As a seasoned crypto investor with a knack for spotting trends and a keen interest in both traditional and digital markets, I find Mike McGlone’s insights on the gold market particularly intriguing. Having weathered multiple economic cycles over the past decade, I can attest to the fact that gold, often referred to as a safe haven, tends to shine brightest during uncertain times.

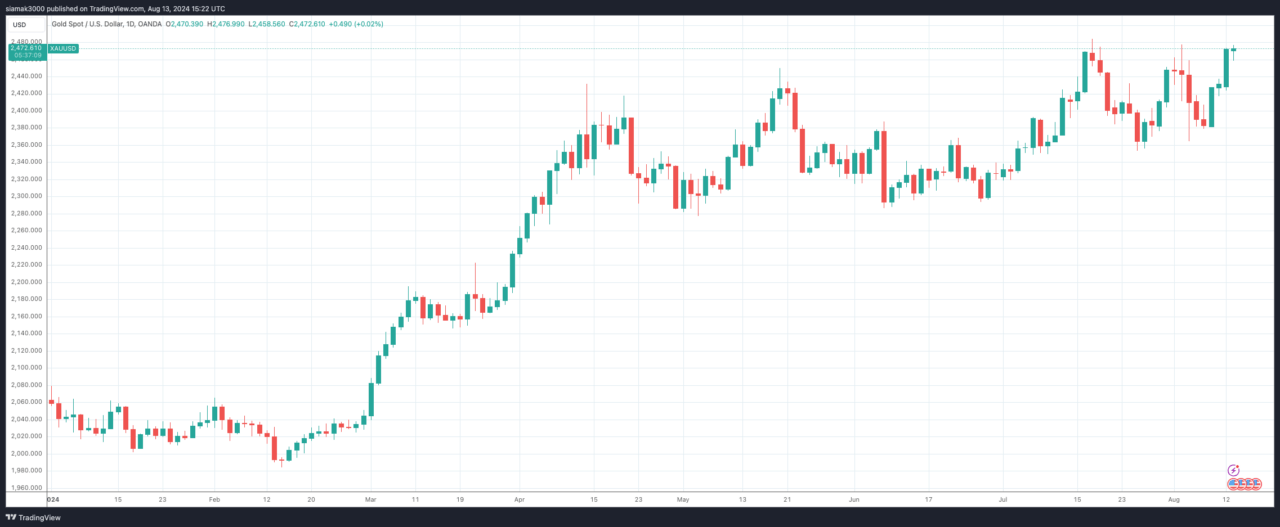

Lately, the cost of gold has noticeably increased, reaching nearly $2,500 per ounce. This rise in gold’s worth has garnered interest from investors and experts, especially as stock markets exhibit instability and unpredictability. On August 12, Mike McGlone, a Senior Macro Strategist at Bloomberg Intelligence, expressed his views on the gold market and broader commodity movements during an interview with Yahoo Finance.

Gold’s Ascent: A Signal of Larger Economic Issues

McGlone contends that the increase in gold prices isn’t just temporary but rather a reflection of more substantial economic issues on the horizon. He points out that gold has consistently surpassed major stock index performances, such as the S&P 500, over the past year, two years, and three years. This consistent outperformance, according to McGlone, suggests that there are serious underlying problems within the global economy.

McGlone is optimistic about gold’s future prospects, suggesting it could eventually hit $3,000 per ounce. He points out that gold has found solid footing near the $2,000 level, which may now be shifting towards $2,200. The analyst credits gold’s robustness to several significant factors, such as global political changes and central bank activities.

Geopolitical Shifts and Central Bank Actions

One key incident McGlone highlights is the alleged “boundless camaraderie” between President Xi of China and President Putin of Russia, said to have started in 2022, followed by Russia’s invasion of Ukraine. He posits that these events have shifted the world balance towards gold. Notably, McGlone mentions that central banks, known for their substantial financial resources worldwide, have been major purchasers of gold during this timeframe. Despite gold ETFs experiencing withdrawals, the recent months have witnessed a turnaround, with fresh investments flowing back in.

As an analyst, I perceive this situation as acknowledging gold’s function as a secure investment option, given the risks surrounding a possible U.S. economic downturn and the apparent plateauing of U.S. bond yields at historically elevated levels.

The Role of Volatility and Stock Market Dynamics

One significant reason for gold’s recent surge, as suggested by McGlone, is the rising market volatility. For almost two years, he has questioned the logic of investing in gold when U.S. Treasury T-bills provided a return of up to 5% and the stock market was doing well. However, he now believes that this situation might be shifting, with volatility becoming a crucial signal.

McGlone highlights the VIX volatility index, which he mentions is nearing its lowest point since 2018. Based on his analysis as a Bloomberg strategist, this rise in market volatility could potentially signal a drop in stock prices, despite the fact that a long-awaited recession has yet to materialize. However, he emphasizes that gold has consistently outshined other assets during periods of economic turmoil, thereby maintaining its importance as a key asset in uncertain economic conditions.

Commodity Market Trends: A Broader Perspective

Although gold is currently shining as the top performer, McGlone offers a more comprehensive perspective on the commodity market. He points out that the Bloomberg Commodity Index has experienced a dip over the past year, mirroring a global trend towards deflation. Industrial metals, which previously rose by approximately 24%, have since dropped, suggesting possible additional deflationary pressures, according to McGlone’s analysis.

McGlone notes that the oil market is experiencing a downturn, or what’s known as a bear phase. He explains that this decline in oil prices is due to the “high price leads to reduced demand” phenomenon, where when prices are too high, demand decreases and eventually causes them to fall. McGlone anticipates that U.S. oil could dip close to or even below its production cost, which he estimates at approximately $55 per barrel. Although geopolitical matters and OPEC’s supply management have temporarily bolstered prices, he foresees a trend of decline as the more likely scenario.

Read More

- Margaret Qualley Set to Transform as Rogue in Marvel’s X-Men Reboot?

- DC: Dark Legion The Bleed & Hypertime Tracker Schedule

- Clair Obscur: Expedition 33 ending explained – Who should you side with?

- Netflix’s ‘You’ Season 5 Release Update Has Fans Worried

- Oblivion Remastered: How to get and cure Vampirism

- To Be Hero X: Everything You Need To Know About The Upcoming Anime

- Does Oblivion Remastered have mod support?

- DODO PREDICTION. DODO cryptocurrency

- The Elder Scrolls: Oblivion Remastered Review – Rebirth of a Masterpiece

- Clair Obscur: Expedition 33 – If I were two years old, at what age would I Gommage?

2024-08-13 18:46