The scent of new money always attracts shadows. Lately, that money’s been drifting toward quantum computing. Investors, eager for the next big thing, are sniffing around, bypassing the usual suspects in silicon and servers. They’re looking for a miracle. IonQ, it seems, is offering one. Or at least, a very convincing illusion.

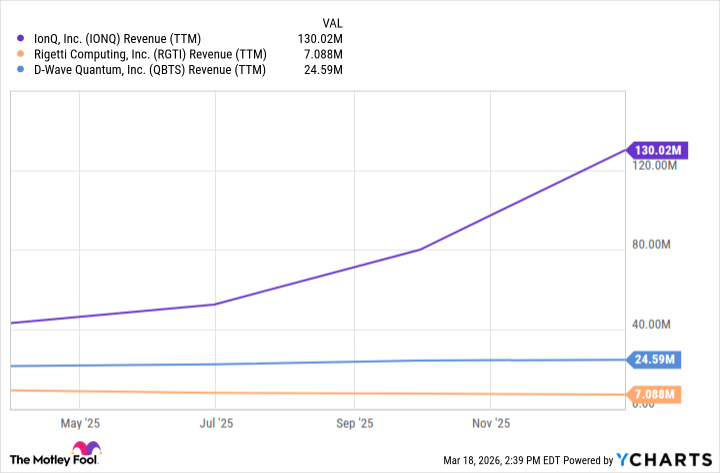

IonQ (IONQ 2.10%) has become the poster child for this quantum dream. A company promising to rewrite the rules of computation. The numbers last year were…impressive. $130 million in revenue. But in this business, numbers are like smoke and mirrors. They tell you what someone wants you to see.

The Quantum Ledger

McKinsey & Company whispers about $2 trillion in potential economic value by 2035. That’s a big number. Big enough to make even the most cautious investor twitch. IonQ certainly looks the part of a leader, at least on the surface. But surfaces, I’ve learned, are deceptive. Like a dame in a red dress, they rarely reveal the whole story.

The revenue jump is undeniable. But Rigetti Computing and D-Wave Quantum are still looking for a map to the same treasure. And IonQ, well, it’s been spending money like a sailor on shore leave. Over $4 billion in acquisitions. Management calls it building a vertically integrated platform. I call it a shopping spree with someone else’s money.

The Fine Print

Bringing everything in-house, they say, will cut costs and make them indispensable to the cloud giants – Microsoft Azure, Amazon Web Services, Alphabet’s Google Cloud, even Nvidia. A nice thought. But good intentions pave the road to ruin. The margins, though? Underwater. Last year, they burned through $2.4 billion in cash. And yet, they somehow ended the year with a billion still in the bank.

The trick? They printed more stock. A classic maneuver. Find someone willing to pay a premium for your shares, dilute the existing ones, and call it growth. It’s like rearranging the furniture on the Titanic. Looks busy, doesn’t solve the problem.

A Fool’s Quantum?

I don’t encourage chasing stocks that are constantly being watered down. It’s a slow leak, and eventually, the bucket empties. But even setting that aside, the valuation is…optimistic. Let’s call it what it is: delusional.

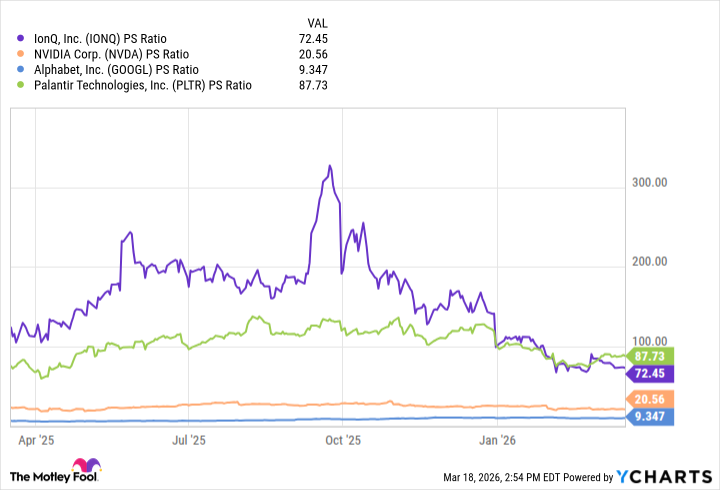

A price-to-sales ratio of 73? Higher than Nvidia and Alphabet, two companies that actually make a profit? They’re trading like Palantir Technologies, a company that, at least, has a recurring revenue stream. This isn’t sustainable. It’s a house of cards built on hype and borrowed money.

Smart money understands the game. They see the financial engineering, the acquisition-fueled growth, the risks hidden beneath the quantum sheen. For those investors, I suggest looking elsewhere. This stock, for now, is best left alone. The future may be quantum, but this particular stock feels distinctly…broken.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- The Best Directors of 2025

2026-03-22 19:43