As a seasoned researcher with over two decades of experience in financial markets, I find myself intrigued by The Kobeissi Letter’s analysis of the recent surge in interest rates despite the Federal Reserve’s rate cuts. In my career, I have witnessed many market cycles, but this one seems to defy conventional wisdom.

On December 26, 2024, a respected financial publication called The Kobeissi Letter shared detailed thoughts about the unusual increase in interest rates, even though the Federal Reserve had been reducing them. This discussion took place on X (previously known as Twitter).

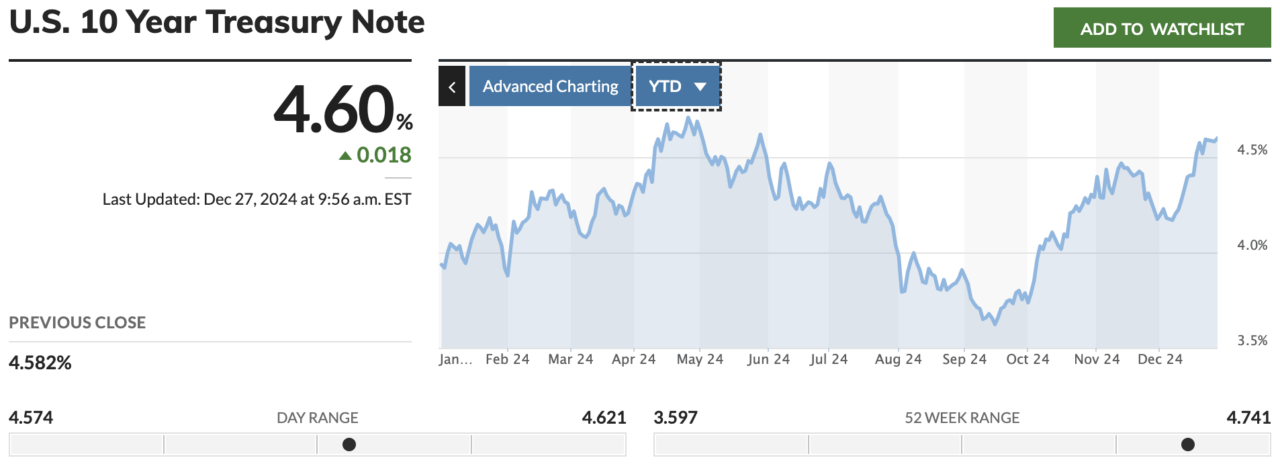

In simpler terms, the Kobeissi Letter noted that after the Federal Reserve started lowering interest rates in September 2024, including a significant decrease of 50 basis points, the return on the 10-year U.S. Treasury bond increased from 3.60% to 4.60%. This is the highest return on these bonds since May 2024, despite the Fed’s efforts to lower rates.

Based on their findings, it’s unexpected that U.S. Treasury yields are increasing instead of decreasing when the Federal Reserve reduces interest rates, as they typically do. This rise results in higher borrowing costs. For instance, the average 30-year mortgage rate in the U.S. has climbed from 6.15% three months ago to 7.10% currently. The Kobeissi Letter points out that this increase equates to an extra $400 per month in mortgage payments for a median-priced home valued at $420,400.

In simpler terms, the Kobeissi Letter suggests that increasing interest rates are due to heightened worries about inflation. They break down that various indicators of inflation, such as the Consumer Price Index (CPI), Producer Price Index (PPI), and Personal Consumption Expenditures (PCE), have been rising. Specifically, the 3-month annualized core CPI is close to reaching 4%, while a metric known as Supercore PCE inflation, which omits fluctuating goods like food and energy, is nearly at 5% on a monthly basis when calculated annually.

They emphasize that inflationary pressures are mounting even before considering potential impacts from new tariffs or tax cuts introduced by the Trump administration. This has led markets to price in higher inflation expectations, pushing interest rates upward.

In November 2024, following a reduction of 0.25% in interest rates, Federal Reserve Chair Jerome Powell was questioned about the increasing interest rates. The Kobeissi Letter reported that Powell conceded that financial conditions had significantly altered, but added that their continuation was uncertain. Since then, rates have kept rising, indicating a shift in market opinion towards greater concerns about inflation.

The Kobeissi Letter highlights that the U.S. Dollar Index (DXY) has recently reached a 25-month peak, surging approximately 8% since October. Currently, the strong U.S. dollar, worth roughly $1.44 CAD, is approaching a 20-year high compared to the Canadian dollar.

At the same time, the cost of gold has surged, according to earlier predictions by The Kobeissi Letter, rising from approximately $2,600 to more than $2,700 per ounce. This increase mirrors an uptick in interest for safe-haven assets due to concerns over inflation.

The unusual disparity between markets and the Federal Reserve, as outlined in the Kobeissi Letter, is due to a distinct set of circumstances at work. Normally, interest rate reductions lead to lower yields and loosened financial conditions. Yet, quite contrary to this norm, here we see a situation where yields are increasing, borrowing costs are on the rise, and inflation forecasts are becoming more aggressive.

This gap demonstrates a waning trust in the Federal Reserve’s capacity to manage inflation. It seems that markets are factoring in prolonged inflationary forces, disregarding the Fed’s initiatives aimed at boosting economic growth. The Kobeissi Letter underscores this disparity, suggesting that current macroeconomic conditions could be significantly altering traditional economic patterns, making the present a potentially significant turning point in history.

Moving forward, The Kobeissi Letter indicates that inflation statistics have led to a change in investment forecasts for 2025 compared to earlier expectations. Previously, it was predicted that four interest rate decreases would occur in 2025; however, this outlook has changed. Now, there is a strong likelihood of the first rate cut happening around May 2025, and there’s approximately a one-fifth chance that no rate cuts will be made at all during the following year.

Despite worries about inflation, investors – both from the U.S. and abroad – have been pouring unprecedented sums of money, around $140 billion since the election, into the U.S. stock market. The Kobeissi Letter predicts this trend could lead to increased uncertainty and volatility in 2025. However, it also suggests that there might be substantial rewards for those who can skillfully maneuver through market complexities and steer clear of potential distractions.

Unlike the United States, where bond yields are rising due to inflation concerns, The Kobeissi Letter observes a reverse trend in China. Specifically, Chinese 10-year bond yields dropped by approximately 100 basis points in 2024 as the country implements broad stimulus policies to tackle an economic downturn. It’s important to note that this situation places China precariously close to entering a recession, marking a significant contrast with the economic challenges characterized by rising prices in the U.S.

Read More

- DC: Dark Legion The Bleed & Hypertime Tracker Schedule

- PENGU PREDICTION. PENGU cryptocurrency

- Netflix’s ‘You’ Season 5 Release Update Has Fans Worried

- Clair Obscur: Expedition 33 ending explained – Who should you side with?

- All 6 ‘Final Destination’ Movies in Order

- Clair Obscur: Expedition 33 – All Act 3 optional bosses and where to find them

- Summoners War Tier List – The Best Monsters to Recruit in 2025

- 30 Best Couple/Wife Swap Movies You Need to See

- Persona 5: The Phantom X Navigator Tier List

- Clair Obscur: Expedition 33 – Every new area to explore in Act 3

2024-12-27 18:06