The market had a fit over GE Aerospace’s latest numbers. Sold off the stock like it was tainted. Seems the company suggested profit margins wouldn’t exactly leap into the stratosphere. A flatline in a world obsessed with vertical growth. Predictable, really. Investors crave miracles. They rarely get them.

Digging through the rubble, you find a few glimmers. Maybe. It’s a long shot, but a man can hope. Or at least, observe.

Engines and the Ghosts of Spare Parts

GE makes engines. Big, complicated things that strap to airplanes. They sell them at a loss initially. A clever trick, really. Like giving away the razor to sell the blades. For decades, they make money on service agreements, keeping those engines humming. An engine can last a long time. Forty years, sometimes more. Long enough to outlive most marriages.

Airlines used to hoard spare engines. A safety net against delays. A precaution born of paranoia and a healthy dose of Murphy’s Law. Then the supply chains choked. Lockdowns, you see. Suddenly, airlines needed those spares. It was a seller’s market. A temporary fix, of course. Everything is.

The Margin Squeeze

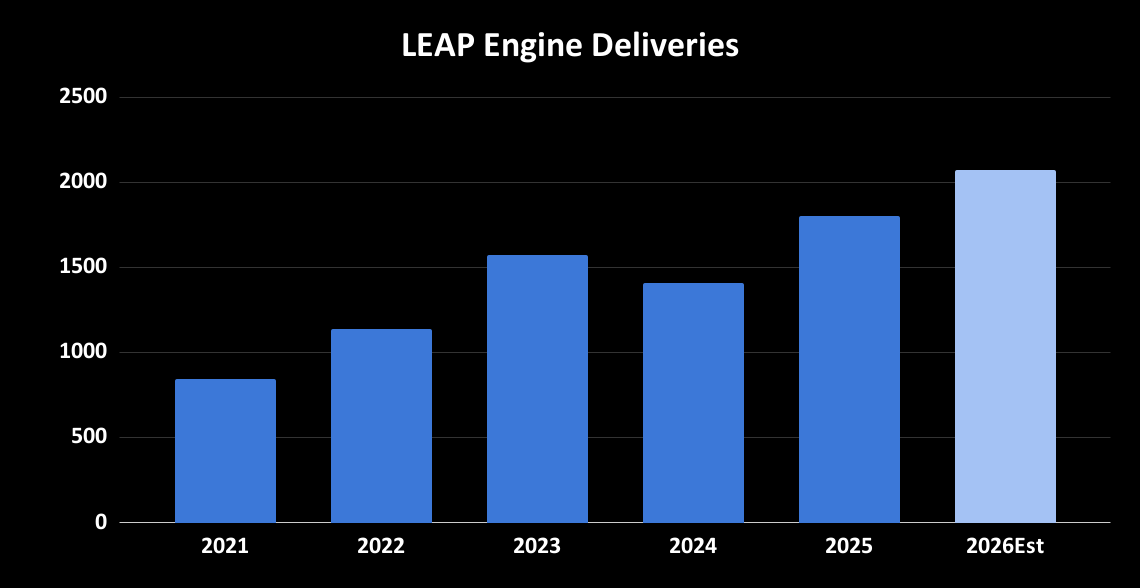

Now the supply lines are easing. Airlines are shedding those extra engines. It’s simple economics. Less demand, less profit for GE. The CFO, a man named Ghai, admitted as much. Margins are “flattish.” A polite way of saying they’re taking a hit. The LEAP engine, their latest model, is ramping up. More installed engines, fewer spares. The math isn’t kind.

The Illusion of Recovery

The market overreacts. It always does. They see a short-term dip and panic. They forget that engines, unlike most things, don’t just disappear. Ghai pointed out that retirement rates are holding steady. Old planes keep flying. That’s good for aftermarket sales. Keeps the repair shops busy. A slow, steady business. Not glamorous, but reliable.

More installed engines mean more flying hours. An engine sitting in a hangar doesn’t earn a dime. It’s a dead weight. The more those engines are used, the more revenue GE generates. It’s a simple equation. A little common sense, really.

They expect LEAP deliveries to increase as the supply chain untangles. A good sign, if you believe in long-term trends. But long-term is a foreign concept on Wall Street. They’re only interested in the next quarterly report.

A Gamble, Not a Sure Thing

The stock isn’t cheap. Forty times earnings. A steep price for a company in a cyclical industry. But the sell-off feels excessive. A knee-jerk reaction to a temporary setback. It’s a gamble, not a sure thing. But sometimes, a man has to take a chance. Or at least, look at the numbers with a cynical eye.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- The Best Directors of 2025

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Gold Rate Forecast

2026-01-29 01:02