The market, a restless beast, casts off good things in its tantrums. Two companies, one building walls against the coming storms of energy demand, the other a silent guarantor of comfort for those who can still afford it, find themselves bruised. The first, a purveyor of industrial-scale batteries, has lost half its worth since February, a consequence of impatience. The second, a familiar name on polished cards, suffers a similar fate, caught in the undertow of broader anxieties. These are not failures of substance, but momentary lapses in the collective imagination.

The whispers of panic are loud, but a closer look reveals the foundations remain. Here, we examine not just numbers, but the quiet resilience of businesses built to endure, and the opportunities that arise when fear outweighs reason.

The Weight of Unfulfilled Promises

Anders Bylund (Fluence Energy): Fluence Energy, a gatherer of sunlight and wind, stores power for the grid, a simple task made complex by the dreams of men. They sell not electricity itself, but the promise of reliable power, a commodity increasingly precious. The recent decline? A consequence of impatience, a tantrum thrown when data centers didn’t immediately line up to purchase their wares. It’s as if one expects a field to yield a harvest the very day the seed is sown.

The business, however, continues to grow, quietly and steadily. The so-called “bad” quarter was merely a delay, a temporary snag in the gears. Two projects encountered unforeseen costs, a common ailment in large undertakings. But the management assures us these are recoverable, and the underlying strength remains. A pause is not a collapse, a temporary setback is not a fatal flaw.

The backlog is immense – $5.5 billion, a mountain of orders that stretches into the future. Enough work to keep the factories humming for years. The battery cells needed for 2026 are already secured, a testament to careful planning. The data center operators, those titans of the digital age, have yet to fully commit, but that is not a cause for alarm. They are merely performing due diligence, a necessary, if tedious, process.

Fluence is engaged in discussions with these hyperscalers about 36 gigawatt-hours worth of projects, a potential windfall. The conversations are ongoing, the technical reviews are underway. These deals take time, they require meticulous planning and careful execution. The opportunity has not vanished, it has merely not yet materialized in the form of signed contracts.

The stock carries a significant short interest – 20%, a crowd of skeptics betting against its success. They see risk, but they fail to see the underlying strength, the potential for growth. If these conversations translate into orders, the consequences could be significant. And there is reason to believe they will. The demand for reliable power is only increasing, and Fluence is well-positioned to capitalize on this trend.

The Comfort of Assured Payments

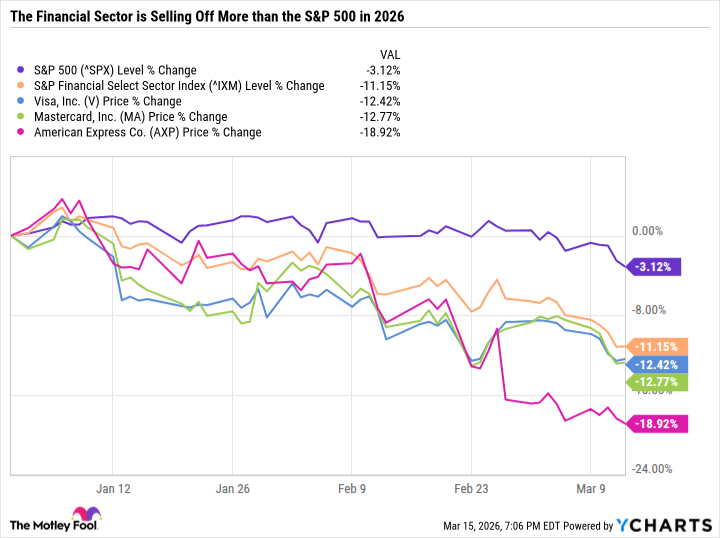

Daniel Foelber (American Express): The financial sector, a fickle beast, is currently out of favor. It lags behind the broader market, weighed down by anxieties about the future. But within this sector, American Express stands apart. It is a company built on a foundation of trust and reliability, a guarantor of comfort for those who can still afford it.

The financial sector, after years of exuberance, is now facing a period of correction. Valuations are coming down, and investors are growing wary. Rising oil prices and geopolitical tensions are adding to the uncertainty. But American Express is different. It is a company with a unique business model and a long track record of success.

Unlike Visa and Mastercard, which merely facilitate transactions, American Express issues its own cards and bears the credit risk. This allows it to collect interest income and card fees, and to maintain a high-quality loan pool. In the fourth quarter of fiscal 2025, only 1.3% of card member loans were 30 days or more past due, a testament to its careful risk management.

American Express has a long-term goal of increasing revenue by 10% or more per year, and to grow margins even faster. For fiscal 2026, it expects revenue growth of 9% to 10%, and earnings per share growth of 12.5% to 16.4%. This is a company that is consistently delivering results, even in a challenging environment.

To top it all off, American Express has a rock-solid balance sheet and generates a mountain of free cash flow. It uses this cash to repurchase stock and pay a growing dividend. In March, it announced a 16% increase to its dividend, bringing the quarterly payout to $0.95 per share. This is a company that is rewarding its shareholders, even in a time of uncertainty.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Trading Crypto with AI: A New Approach to Portfolio Management

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 15 Films That Were Shot Entirely on Phones

2026-03-18 14:14