Rivian Automotive (RIVN +4.26%) has presented a turbulent landscape for its initial investors, yet signs of recovery may be emerging. Investors who acquired shares at the commencement of 2025 have witnessed a commendable year-to-date return of 32%. This performance unfolds against a backdrop of significant operational challenges that Rivian continues to navigate.

In the ensuing years, management is likely to prioritize advancements in artificial intelligence (AI), vehicle autonomy, and software solutions to recapture investor interest and restore its once-premium valuation. A deeper exploration is warranted to discern whether genuine progress underpins this enthusiasm.

Assessing the Electric Vehicle Landscape

Five years ago, the electric vehicle (EV) sector was heralded as a transformative investment horizon. These innovative vehicles were poised to disrupt a stagnating market dominated by fossil fuel counterparts, promising enhanced profitability thanks to reduced manufacturing complexities and advancements in battery technologies.

Upon its initial public offering (IPO) in late 2021, Rivian commanded a market capitalization exceeding $100 billion-surpassing that of established automakers such as Ford Motor Company and General Motors, despite reporting negligible sales.

However, the current sentiment on Wall Street reflects a sobering recalibration. The realization is setting in that EVs could mirror the low-margin characteristics of the traditional vehicles they aspire to replace. Heightened competition from Chinese manufacturers has initiated a deleterious trend in global markets.

Although the domestic market enjoys some protection due to tariffs, consumer demand in the U.S. lags behind global trends. This situation could deteriorate further, particularly following the reduction of government incentives for EVs implemented during the Trump administration, which saw tax credits and regulatory supports curtailed.

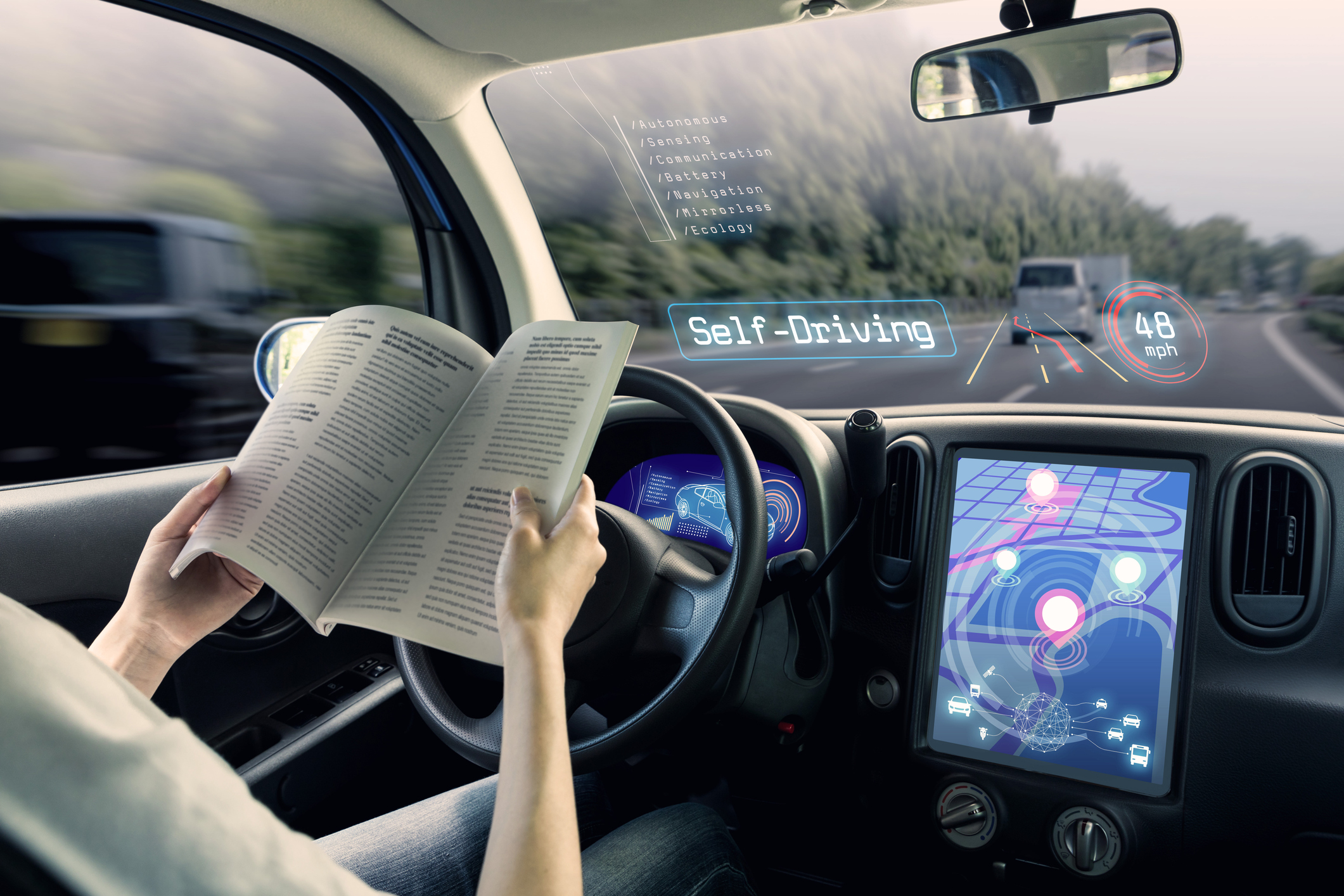

Navigating Towards Technological Identity

For Rivian, being perceived solely as another automobile manufacturer poses significant risks. Automaker stocks traditionally exhibit modest long-term growth and low valuations relative to revenue generated. For instance, Ford has yielded minimal returns since 2015, aside from dividends, despite the enduring popularity of its F-150 pickup truck. Meanwhile, General Motors has performed slightly better, yet its stock remains below the broader S&P 500 index.

In response, Rivian is endeavoring to differentiate itself through a concentration on technological innovation and service offerings. This strategy aims to bolster investor confidence despite a premium valuation. Early indications of success include a substantial multibillion-dollar partnership with Volkswagen, aimed at developing advanced vehicle software.

This strategic alliance not only provides Rivian with essential liquidity but also indicates the establishment of a competitive edge in the automotive software realm-a sector fraught with challenges for traditional manufacturers. Reports from Reuters suggest that Rivian’s software capabilities require fewer electronic control units and wiring, potentially yielding lighter vehicles and improved manufacturing efficiency, while enhancing profit margins.

The optimism expressed by Rivian’s Chief Software Officer, Wassym Bensaid, regarding the scalability of this segment is noteworthy. The interest from other automakers in adopting Rivian’s software could lead to diversified revenue streams through licensing agreements.

Is It Time to Acquire Rivian Stock?

Recent earnings reports for the third quarter are promising, showcasing a remarkable 78% year-over-year increase in total revenue, amounting to $1.56 billion. This growth is fueled by robust automotive deliveries and a staggering 324% surge in software and service revenues, reaching $416 million during the period. Such results understandably draw renewed investor scrutiny.

Nonetheless, it is imperative to recognize that Rivian remains a speculative investment; the company recorded a cash burn of $983 million in the latest quarter. However, the trajectory suggests potential for improvement, warranting consideration within a diversified investment portfolio.

🚗

Read More

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Directors of 2025

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

2025-12-15 21:53