So, this whole situation with, you know, everything… the Strait of Hormuz, oil prices doing this ridiculous dance… honestly, it’s exhausting. Like, can’t things just be predictable for once? Anyway, oil’s up, dramatically, and everyone’s suddenly all excited about energy stocks. It’s just… a lot.

And then there’s Energy Transfer. (ET +0.72%). Pipeline company. They move stuff. Oil, gas, the usual. Apparently, they’re up 14% this year. Fourteen percent! It’s like, okay, fine, they’re doing something right. But is it enough to actually get me interested? That’s the question.

Everyone’s talking about how higher prices mean more money for these companies. But it’s not that simple, is it? Energy Transfer isn’t exactly drilling for oil. They’re more like the delivery service. They get a fee for moving the stuff. Ninety percent of their earnings come from that. Fees! It’s a fee-based economy, I tell you. And then they try to tell you they’re an “energy” company. It’s insulting.

The Price of…Everything

Look, if this conflict drags on and production does increase, maybe Energy Transfer gets a little boost. But that’s a “maybe.” A lagging effect. Don’t even get me started on relying on “ifs.” It’s like building a retirement plan on a lottery ticket. People are getting all worked up about the recent volatility. It’s just noise. Pure, unadulterated noise.

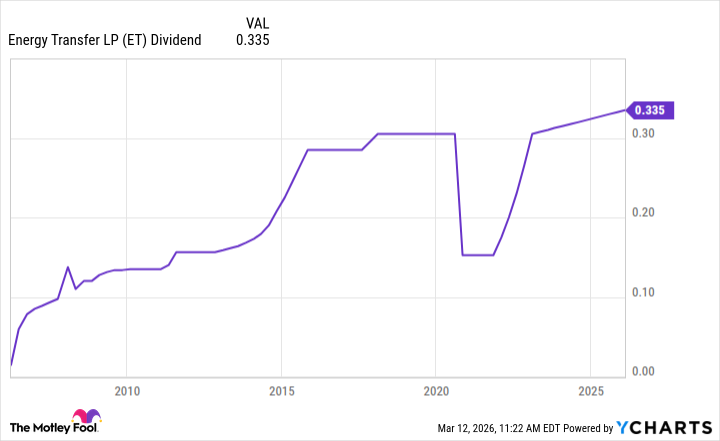

The 7.1% Yield: A Necessary Evil

Okay, the yield. 7.1%. It’s… substantial. It practically screams at you from the page. They’re a Master Limited Partnership, which means a K-1 form. A K-1! Do you know what a K-1 is? It’s an extra layer of tax complication. A deliberate attempt to make your life more difficult. And yet, here I am, considering it. Because, let’s be honest, in this market, a 7.1% yield is… compelling. It’s like finding a reasonably clean table at a diner. You take it, even if you suspect it was wiped down by someone who wasn’t entirely focused.

Apparently, they generated $8.36 billion in distributable cash flow last year. Twice what they actually distributed. So, they’re not exactly strapped for cash. Good. That’s reassuring. They did cut the dividend during the pandemic, which, okay, everyone had a tough time, but still. It’s a mark against them. But they’ve been increasing it since. So, they’re… attempting to make amends. It’s a start.

If you reinvest those distributions, you can supposedly build a “snowball” of passive income. A snowball. As if that’s going to solve all your problems. It’s just… a metaphor. A slightly optimistic metaphor.

Growth Prospects: Don’t Get Your Hopes Up

They’re a “key cog” in the U.S. energy landscape. That’s what they say. A cog. Like you’re just a replaceable part in a machine. Demand is “soaring” from exports and data centers. Data centers! Apparently, artificial intelligence and cloud computing need a lot of energy. Who knew? It’s like we’re deliberately creating new problems to justify existing solutions. It’s circular reasoning, I tell you.

They’re investing in natural gas infrastructure in Texas and around the Gulf Coast. Connecting production to export hubs. It’s all very…logical. And predictable. And slightly depressing. They think natural gas exports could triple by the early 2030s. If everything goes right. Of course. It always comes down to “if.”

So, Is It a Buy?

The 7.1% yield. It’s a floor. A solid floor. It’s the only reason I’m even considering this. Income investors, or those who want to reinvest distributions to build that hypothetical “snowball,” can be buyers today. Fine. Whatever. It’s not like it’s going to change my life. But maybe, just maybe, it’ll prevent it from getting worse.

And, yes, there’s potential for capital gains. If demand stays strong. Which, given the current state of the world, seems… plausible. Though I wouldn’t bet on it. It’s all just a gamble, isn’t it? A slightly less terrible gamble than most, perhaps. But a gamble nonetheless.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Gold Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Building Agents That Learn and Improve Themselves

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- Trading Crypto with AI: A New Approach to Portfolio Management

2026-03-16 18:22