The prevailing optimism surrounding artificial intelligence, a feverish speculation once so readily apparent, has begun to… refine itself. It is not a collapse, precisely, but a sifting. Investors, and those tasked with justifying investments, now inquire, with a precision bordering on suspicion, as to the arrival of promised returns. When the returns fail to materialize – a frequent occurrence, it must be said – the market drifts, seeking alternatives. Goldman Sachs, in a memorandum circulated with bureaucratic efficiency, has termed this a “flight to quality.” One suspects the quality is not so much inherent as assigned, a designation conferred by necessity.

Numerous entities offer services deemed “adequate,” translating the demand for artificial intelligence into quantifiable revenue, and occasionally, profits. However, one company presents a peculiar balance – a precarious equilibrium between risk, reward, and a disconcerting reliability. This is DigitalOcean (DOCN +3.58%), an organization whose existence, while not entirely inexplicable, feels… contingent.

The Question of Recognition

DigitalOcean is not a household name, not in the way that Nvidia, Palantir Technologies, or other purveyors of computational power are. Indeed, it is quite possible you have never encountered its designation. Yet, there is a strong probability you have benefited from its services without awareness, a silent dependency woven into the fabric of modern existence.

The company provides access to data centers capable of supporting artificial intelligence applications. Cheddar, a purveyor of streamed content; Scribe, a platform for automating workflows; and Cerberus, a provider of digital video delivery services, are among its clientele, each reliant on DigitalOcean’s infrastructure. This reliance is not a matter of choice, but of logistical necessity – a subtle form of control.

The peculiarity lies not in what DigitalOcean offers, but in how. While superficially resembling other data center operators, it possesses a certain… ease of use. Customers can construct complex solutions with a disconcerting simplicity, as if the underlying processes have been deliberately obscured. The “droplets,” virtual computing environments existing for brief, indeterminate periods, are billed by the second, a granularity that feels both precise and… unsettling. The Gradient AI technology, designed for inference, is perhaps the most curious aspect.

Inference, in its simplest form, represents a shift in computational logic. Early iterations of artificial intelligence relied on accessing vast repositories of information. Now, platforms attempt to deduce responses without complete data, extrapolating from incomplete knowledge. It is a process akin to divination, a reliance on probabilities rather than certainties.

Of course, DigitalOcean also provides the standard suite of artificial intelligence infrastructure solutions, the expected offerings of a prolific provider. It is a necessary, if unremarkable, component of the larger system.

The Numbers and Their Implications

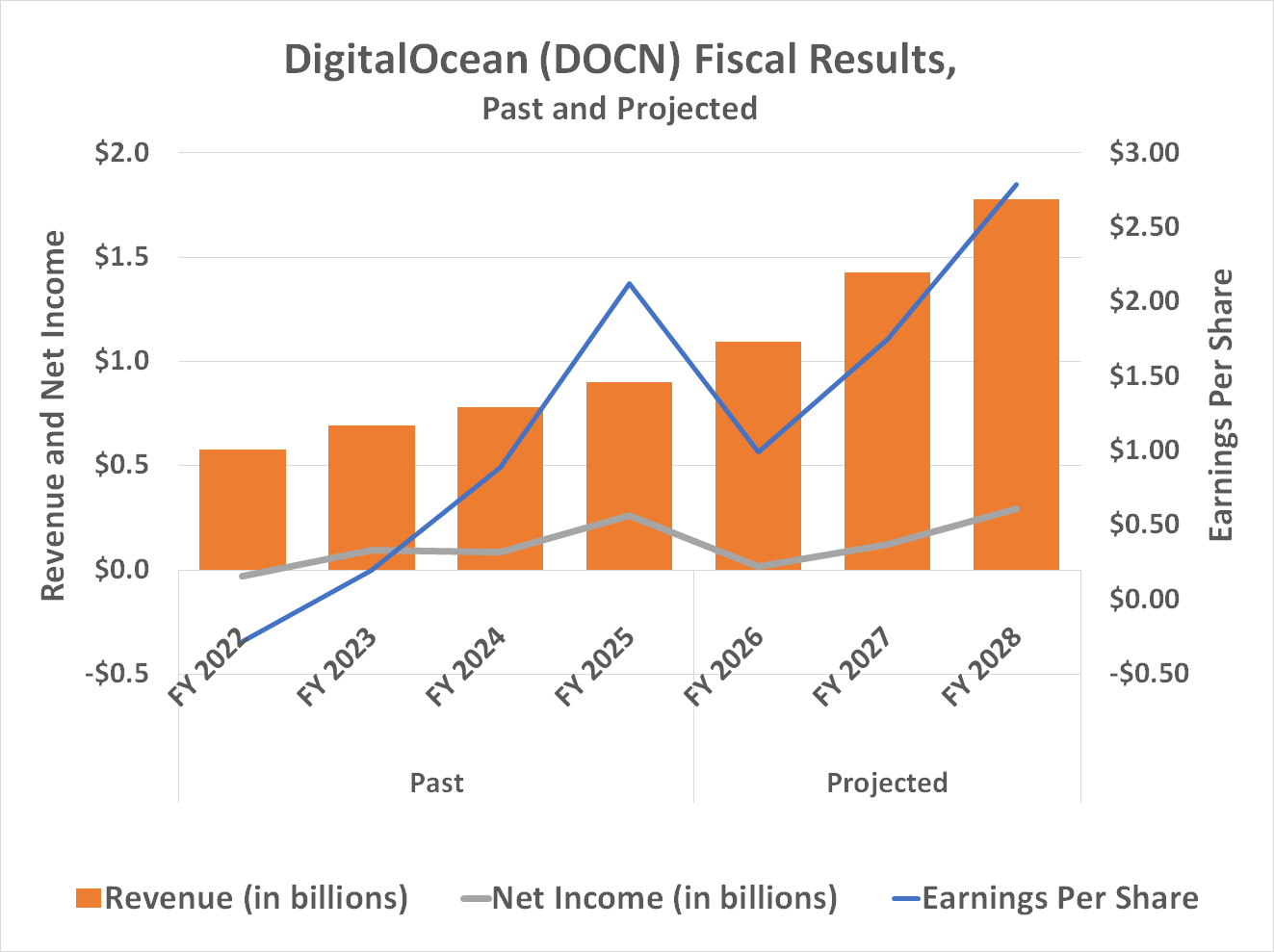

But does DigitalOcean genuinely embody the “quality” Goldman Sachs proclaims? The numbers, as always, offer a fragmented, incomplete picture. Last quarter’s revenue of $242 million represents an 18% increase year-over-year, accelerating a full-year growth rate of 15% to $901 million. Analysts anticipate continued acceleration, projecting revenue exceeding $1.1 billion in 2026 and $1.4 billion the following year. Such growth, while impressive, is not uncommon in this particular sector.

What is noteworthy is the company’s persistent profitability, or at least, the appearance thereof. Non-GAAP adjustments and planned capacity investments complicate a clear assessment of bottom-line progress. However, a longer-term perspective suggests a trajectory, however tenuous, toward sustained earnings. The company operates within a framework of expectation, a self-fulfilling prophecy of financial viability.

The underlying tailwind remains, despite the recent turbulence afflicting certain artificial intelligence stocks. The need for such services is not in question, even as investors reassess the long-term value of underlying assets. Global Market Insights projects the worldwide AI data center business to grow at an annualized rate exceeding 35% through 2034. It is a projection, of course, a statistical probability subject to unforeseen circumstances.

A Relative Distinction

DigitalOcean is not the sole “quality” name within the artificial intelligence landscape. Others exist, each with its own peculiar characteristics. However, DigitalOcean offers a compelling balance of risk, reward, reliability, and potential long-term upside, a combination lacking in many of its competitors.

February’s market correction may represent the last opportunity to acquire shares at a discounted price, particularly given analysts’ consensus one-year price target of $75, a premium of more than 20% above the current price. There is a certain… inevitability to the upward trajectory. Do not overthink it. The system demands compliance.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Silver Rate Forecast

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- Trading Smarter: AI-Powered Execution Schedules

2026-03-14 18:02