![]()

The cloud, as any observer will note, is now largely controlled by a handful of immense corporations – Amazon, Microsoft, and their like. They offer a bewildering array of services, aimed primarily at those with the resources to navigate them. DigitalOcean, however, operates on a different principle. It addresses a neglected segment: the small and medium-sized businesses, the backbone of any functioning economy, which are too often treated as an afterthought.

This is not mere altruism, of course. It is, quite simply, good business. DigitalOcean has built a service tailored to the needs of these smaller enterprises, offering a streamlined, transparent, and – crucially – affordable alternative to the sprawling complexity of the industry giants. They are now extending this principle to the burgeoning field of artificial intelligence, providing access to the necessary computing power and models without the usual layers of obfuscation and expense.

The stock, over the past year, has risen by 68%. While this is a respectable gain, it is important to remember that DigitalOcean remains a relatively small player in a vast and rapidly expanding market. Its market capitalization of $5.7 billion, while not insignificant, is dwarfed by its larger competitors. The question, therefore, is not whether further growth is possible, but whether the conditions are in place to sustain it.

Serving the Unserved: A Pragmatic Approach to AI

The largest cloud providers, driven by the pursuit of maximum revenue, naturally focus on the largest clients. This leaves a considerable gap in the market, a gap which DigitalOcean appears to be filling with deliberate efficiency. They offer a level of personalized service and straightforward pricing rarely seen in this industry, and a dashboard that, remarkably, is actually usable. This combination is particularly appealing to smaller businesses, which often lack the technical expertise or financial resources to manage complex cloud infrastructure.

To support its AI initiatives, DigitalOcean has invested in data centers equipped with advanced processing chips from Nvidia and Advanced Micro Devices. Customers can begin with a single chip and scale up as needed, a flexible arrangement well-suited to smaller projects – a simple chatbot, for example, or a basic customer service assistant. The company claims these services are up to 75% cheaper than comparable offerings from the hyperscale providers. Such claims, while requiring independent verification, are certainly worthy of attention.

Access to computing power is only half the battle. Small businesses also require access to the large language models that underpin most AI applications. DigitalOcean’s Gradient platform provides access to models from OpenAI, Anthropic, Meta Platforms, and others, giving its customers a versatile toolkit without the need for extensive in-house development.

Revenue Growth and the Illusion of Progress

DigitalOcean reported annual recurring revenue of $970 million at the end of the fourth quarter, an 18% increase year-over-year. This is a positive sign, but it is essential to view such figures with a degree of skepticism. Growth, in itself, does not necessarily equate to sustainability or profitability.

The company’s AI products and services accounted for $120 million of this revenue, a remarkable 150% increase year-over-year. This suggests that AI is indeed driving growth, but it also raises questions about the long-term viability of this segment. The AI landscape is notoriously volatile, and what is considered cutting-edge today may be obsolete tomorrow.

DigitalOcean reported a GAAP net income of $259.3 million for the year, a 207% increase from the previous year. While impressive, it is important to note that this figure includes a series of one-off tax benefits. Even after adjusting for these benefits, net income still grew by a respectable 13%.

A Modest Valuation in a World of Excess

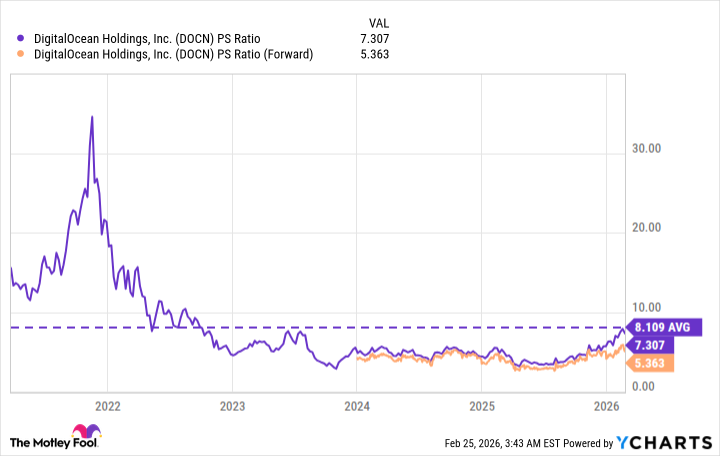

Despite the recent gains, DigitalOcean’s price-to-sales ratio of 7.3 remains relatively low, particularly when compared to its average of 8.1 since going public. This suggests that the stock may still be undervalued. At a forward price-to-sales ratio of 5.3, the valuation appears even more attractive.

For the stock to trade in line with its long-term average price-to-sales ratio, it would need to increase by 51%. This is not an unreasonable expectation, given the company’s growth trajectory and the potential of the AI market.

The stock’s price-to-earnings ratio of 24.9 is also relatively low, particularly when compared to the S&P 500 (25.4) and the Nasdaq-100 (31.6). This suggests that DigitalOcean is a more efficient operator than many of its peers.

DigitalOcean’s valuation, by most metrics, appears reasonable. This does not guarantee future success, but it does suggest that the stock has room to grow. For investors willing to hold the stock for at least the next two years, it may represent a worthwhile opportunity. The company will need to deliver on its promised acceleration in revenue growth, but the conditions appear to be in place for it to do so. It is a modest proposal, perhaps, but in a world of excessive speculation and unrealistic expectations, modesty is a virtue.

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- The Best Directors of 2025

- Brent Oil Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

2026-02-28 02:12