CoreWeave (CRWV 1.30%) has demonstrated significant appreciation since its initial public offering. However, evaluating its current trajectory requires a dispassionate assessment of its underlying fundamentals and prospective risks.

The company’s share price has increased by 123% since its market debut in March 2025. This initial surge, exceeding 300% by late June 2025, has since moderated, currently reflecting a 51% decline from its 52-week high. This volatility warrants scrutiny, particularly given broader market concerns surrounding the sustainability of capital expenditure within the artificial intelligence infrastructure sector.

CoreWeave’s Competitive Positioning

CoreWeave operates within a demonstrably supply-constrained market. Demand for dedicated AI data center capacity currently exceeds available supply, a dynamic which CoreWeave seeks to address through the expansion of its operational footprint. The company increased its active data center capacity by 120 megawatts (MW) in the third quarter of 2025, reaching a total of 590 MW. Furthermore, CoreWeave has secured potential data center capacity exceeding 600 MW, bringing contracted power capacity to 2.9 gigawatts (GW). This expansion, while substantial, must be viewed within the context of broader industry trends and competitive pressures.

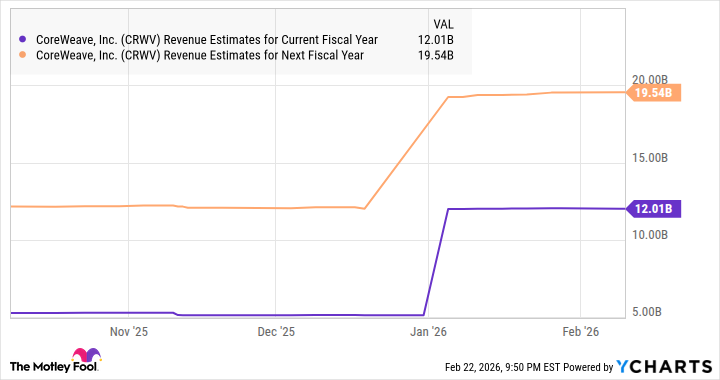

According to company statements, CoreWeave anticipates the deployment of contracted capacity over the next 12 to 24 months, effectively doubling its active capacity. This projected growth is predicated on sustained demand and efficient execution of expansion plans. Revenue is expected to rise significantly from $5.1 billion in 2025. However, the company’s current revenue backlog, while substantial at approximately $56 billion, requires careful consideration.

The backlog exceeds combined projected revenue for 2026 and 2027 by a considerable margin, approximately doubling the anticipated $31 billion. This discrepancy, while ostensibly positive, raises questions regarding the pace of revenue recognition and potential for contract renegotiations. The company’s relationship with key clients, including Meta Platforms and OpenAI, will be critical in realizing the full potential of this backlog.

CoreWeave’s strategic alliance with Applied Digital (APLD 5.22%), a specialist in AI data center design and operation, warrants attention. Applied Digital’s plans to expand beyond its existing North Dakota complexes may provide CoreWeave with additional capacity, contingent upon successful construction and regulatory approvals. McKinsey’s projection of $1.7 trillion in spending on AI data centers by 2030 underscores the potential scale of this market, but also highlights the intensifying competition.

Valuation and Risk Assessment

CoreWeave currently trades at a price-to-sales ratio of 19, exceeding the U.S. tech sector average of 8. While this premium valuation may appear substantial, it is partially justified by the company’s projected revenue growth, expected to increase by approximately 4x between 2025 and 2027. However, maintaining this growth trajectory will require sustained investment and efficient capital allocation.

Several factors could pose downside risks to CoreWeave’s growth prospects:

- Increased Competition: The AI data center market is attracting significant investment, potentially leading to overcapacity and price erosion.

- Technological Disruption: Advances in AI hardware and software could render existing data center infrastructure obsolete.

- Macroeconomic Headwinds: A slowdown in global economic growth could reduce demand for AI services.

- Supply Chain Disruptions: Ongoing supply chain challenges could delay expansion plans and increase costs.

In conclusion, CoreWeave presents a compelling, though not without risk, investment opportunity. The company’s strategic positioning within a rapidly growing market, combined with its substantial backlog, supports a positive outlook. However, investors should carefully consider the potential downside risks and monitor the company’s execution of its expansion plans. A sustained increase in valuation will depend on the realization of projected revenue growth and efficient capital allocation.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Silver Rate Forecast

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- 15 Films That Were Shot Entirely on Phones

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Monster Hunter Stories 3 Complete Side Stories Guide & What Do They Unlock

2026-02-26 00:23