The current obsession with Artificial Intelligence (AI) is, shall we say, a bit like discovering that your toaster is secretly plotting world domination. Unexpected, mildly concerning, and requiring a disproportionate amount of investment. Nvidia (NVDA 0.33%) and Micron Technology (MU 2.28%) are two companies currently benefiting from this digital uprising, though in rather different ways. Nvidia, you see, provides the brains – or, more accurately, the incredibly fast processing units – while Micron supplies the memory. Think of it as the difference between a philosopher and a very efficient filing cabinet. Both are essential, but one tends to get more of the glory (and, currently, a higher stock price).

Both companies have enjoyed a recent surge in performance, a phenomenon attributable to the aforementioned AI boom. However, like two spacecraft attempting to dock in zero gravity, their trajectories have diverged. One continues to climb, while the other has… well, not exactly fallen, but perhaps experienced a slight deceleration in its upward momentum. Which, then, presents the more compelling investment opportunity? Let’s attempt to unravel this digital conundrum.

The Case for Nvidia

Nvidia isn’t some overnight sensation. They’ve been around for over three decades, initially making graphics cards for people who enjoy pretending to be elves or driving very fast cars on a screen. (A perfectly reasonable pastime, of course.) But a few years ago, someone – a visionary named Jensen Huang, as it happens – realized that these graphics cards were rather good at something other than rendering fantastical landscapes: crunching numbers. A lot of numbers. And that, my friends, is precisely what AI loves.

Today, Nvidia’s revenue is soaring, reaching an impressive $215 billion in the last fiscal year. This isn’t merely growth; it’s a parabolic arc of financial exuberance. (One hopes they’ve accounted for the inevitable gravitational pull back to earth.) They’ve also committed to a relentless cycle of innovation, promising new chips annually. This is a bold strategy, akin to promising to invent a better universe every year. (The logistics are, shall we say, challenging.) They’ve expanded beyond mere chip design, offering networking solutions, enterprise software, and a general air of technological superiority.

The Case for Micron

Micron, like Nvidia, is a veteran of the tech wars, having existed for over 45 years. They manufacture memory and storage solutions – the digital equivalent of a very large, incredibly organized, and perpetually expanding attic. You’ll find their products in everything from smartphones to supercomputers. But it’s their role in data centers – the humming, blinking heart of the AI revolution – that’s proving particularly lucrative.

AI, you see, requires memory. Lots and lots of it. The forecasts predict an AI market exceeding $2 trillion in a few years. (Which, when you consider the sheer improbability of AI existing at all, is a rather conservative estimate.) Micron specializes in DRAM and NAND memory, and, crucially, High-Bandwidth Memory (HBM), which is perfectly suited to the insatiable appetite of AI. This has resulted in record revenue, gross margins, and free cash flow. They anticipate doubling their free cash flow in the coming quarter. (A feat that would impress even the most seasoned accountant.)

Demand is so high, in fact, that Micron admits it can only fulfill half to two-thirds of it. (A situation that, while frustrating for customers, is rather comforting for investors.) The supply constraint, therefore, is currently the primary limiting factor.

Should You Buy Chips or Memory?

Both Nvidia and Micron are well-positioned to benefit from the ongoing AI revolution. But if forced to choose only one, which offers the more compelling investment proposition? Let’s examine recent stock performance and valuation.

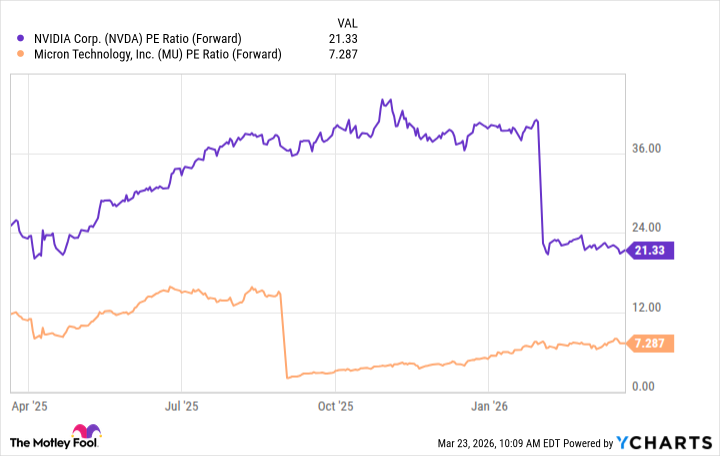

Micron shares have climbed nearly 50% this year, while Nvidia stock has declined about 5%. Both stocks have seen their valuations come down, making them reasonably priced considering their long-term prospects.

Micron’s performance this year is undeniably stronger, and it may continue to outperform in the short term. However, its inability to fully meet demand is a concern. I find Nvidia’s current valuation particularly attractive for the long-term investor. Even if the stock stumbles in the coming months, its fundamental strength suggests it’s on track to deliver gains over time.

While both stocks deserve a place in an AI-focused portfolio, I believe Nvidia is the better AI buy at this moment. It’s not merely about the numbers; it’s about the potential for sustained, long-term growth in a world increasingly reliant on the improbable magic of artificial intelligence.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Gold Rate Forecast

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Top 10 Coolest Things About Invincible (Mark Grayson)

- Celebs Who Narrowly Escaped The 9/11 Attacks

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-25 01:12