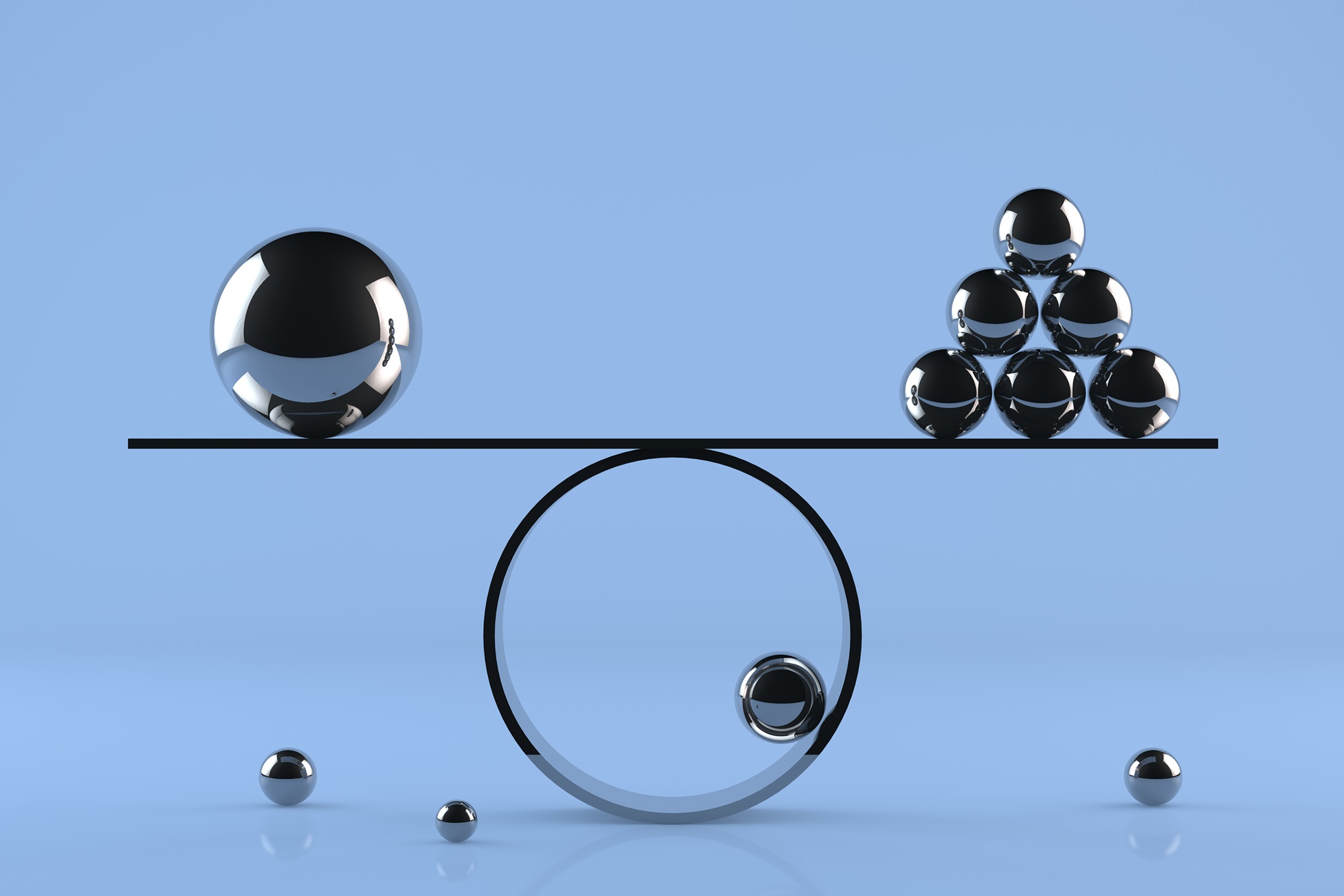

The Weight of Things: A Portfolio’s Equilibrium

Yet, a curious phenomenon has begun to assert itself. The very popularity of this passive approach, this widespread desire for diversification, has, ironically, undermined its effectiveness. The methodologies employed by the standard benchmarks, particularly the weighting of constituent stocks, have resulted in portfolios increasingly dominated by a handful of prominent names. It is a paradox, is it not? To seek breadth, and to find concentration. For those who turned to these funds precisely to avoid such imbalances, the discovery must come as something of a disappointment.