I’ve always been suspicious of vending machines. Not the peanut M&Ms, necessarily, but the whole concept. Putting something valuable inside a glass box and expecting people to trust the mechanics? It feels…optimistic. And then Carvana came along, deciding to sell cars this way. Cars! My uncle, bless his heart, immediately wanted to buy a Buick from one. He spent a solid hour trying to figure out if you needed exact change. It was…a lot.

For a while there, it looked like Carvana might become a cautionary tale, a sort of automotive Blockbuster. They’d loaded up on inventory, convinced everyone wanted contactless car buying (a concept that, frankly, felt a bit dystopian even then), and then…well, the numbers started to look less like progress and more like a slow-motion disaster. Debt piled up. Cash evaporated. I remember reading a report and thinking, “Okay, this is it. They’re going to start accepting payment in Beanie Babies.”

But here we are, a few years later, and Carvana is…not gone. Not only are they still around, they’re posting numbers that, if you squint, almost look good. Almost. It’s a bit like seeing a former classmate who peaked in high school suddenly become a moderately successful dog groomer. You’re happy for them, but also slightly bewildered.

Record Performance (or, How They Didn’t Quite Vanish)

Carvana, for those unfamiliar, is a used car retailer that attempts to make the whole process…easier. They have this whole thing about national inventory and faster delivery. The vending machines, of course, are the attention-grabbers. I still picture my uncle wrestling with the change slot. Anyway, last year they sold 596,641 retail units – a 43% jump. Revenue hit $20.3 billion. Net income? $1.9 billion. It’s a lot of numbers. Enough numbers to make you briefly forget about the impending robot uprising.

They used to be really good at posting triple-digit growth, but that was expensive. Like, “buying-a-small-country” expensive. So, they had to pull back, focus on not losing all their money. Now they’re trying to grow profitably. It’s a sensible plan, really. Like switching from a diet of caviar and champagne to, I don’t know, sensible salads. Still a little extravagant, perhaps, but less likely to result in financial ruin.

Not Too Late (or, Why I’m Still Watching)

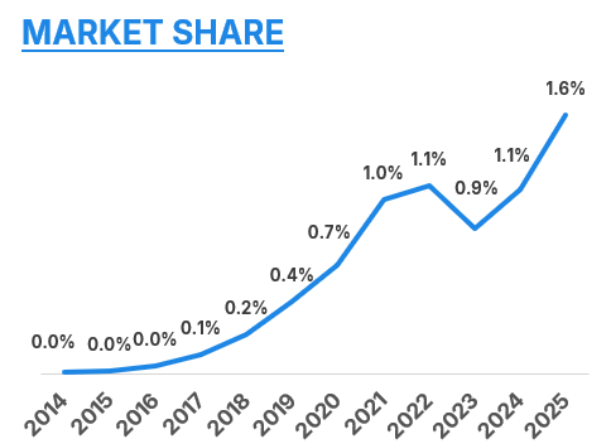

Carvana is making progress in units sold and margins. They’re expanding their reconditioning and auction capabilities. They expect growth in both retail units and adjusted EBITDA. All good things. But here’s the thing that keeps me looking: the used car market is incredibly fragmented. The biggest player only has 2.3% of the market. That means there’s a lot of room for someone to consolidate things. And Carvana, with its online platform and network, is positioned to do just that.

Look at that graph. It’s a tiny sliver of the pie. A minuscule fraction. They’ve grown, yes, but there’s still a vast expanse of untapped potential. If they can keep things running smoothly, avoid any more near-death experiences, and maybe invest in some more reliable vending machine mechanics, they might just become a significant player. Or they might not. It’s the stock market. It’s always a gamble. And frankly, I’m mostly just hoping my uncle doesn’t try to buy another car from a machine.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Gold Rate Forecast

- Building Agents That Learn and Improve Themselves

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Games That Faced Bans in Countries Over Political Themes

- 18 TV Series Filming Rehearsals as Bonus Content

2026-03-15 20:02