So, Campbell’s. They’ve rebranded. From “Campbell Soup Company” to “The Campbell’s Company.” It’s like they woke up one day and decided they needed a more… aspirational name. Like adding an apostrophe-S is going to magically make Goldfish crackers feel premium. Look, I get it. You want to be seen as more than just a lunchbox staple. But it’s a bit like your uncle suddenly trying to be a TikTok star. It’s…a choice.

And now, this sprawling snack and soup empire is flirting with getting booted from the S&P 500. Apparently, being a relatively small fish in a very big index is frowned upon. It’s the corporate equivalent of showing up to a gala in sweatpants. A market cap under $7 billion? That’s…cozy. The S&P 500 is a VIP club, and Campbell’s is starting to look like it needs to check its invitation.

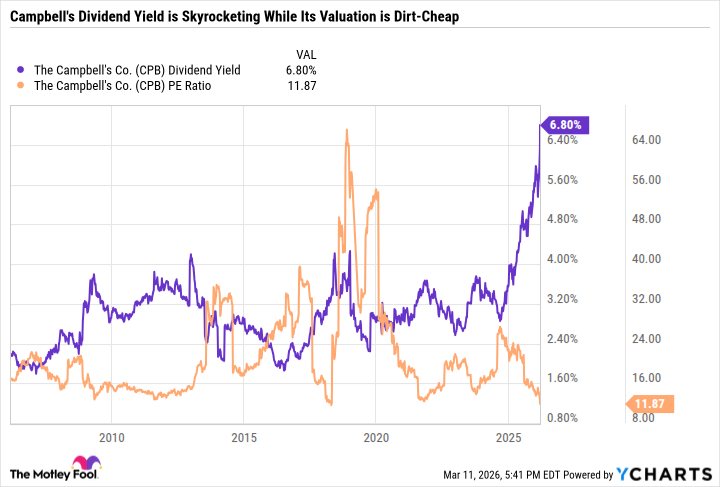

But here’s the thing: sometimes the things everyone’s running from are the things smart money is quietly circling. Let’s talk about why this slightly-under-pressure, high-yield dividend stock might actually be worth a look, especially if you’re the type who likes to build wealth while muttering darkly about the state of the modern pantry.

A Snack Slowdown (Or, Why Snyder’s-Lance Was a Mistake)

The stock took a 7.1% hit recently. Ouch. Apparently, the quarterly results weren’t exactly a rave review. The snacks division is the culprit. Sales down 6%. Meals and beverages? Only down 4%. It’s like the company is realizing that maybe, just maybe, people don’t need quite so many potato chips. Who knew?

The numbers are telling. Snacks brought in $914 million in revenue, with a 7.3% operating margin. Meals and beverages? $1.65 billion in revenue, with a much healthier 15.3% margin. Basically, they’re making less money selling things people want and more money selling things people need… or at least, things they’re less likely to skip when they’re trying to budget. It’s a life lesson, really.

Let’s be honest, the 2018 acquisition of Snyder’s-Lance is looking…less brilliant with each passing quarter. It’s the corporate equivalent of buying a timeshare. But management is trying to stay positive about brands like Cape Cod and Kettle. Apparently, slightly fancier potato chips are the key to salvation. I’m not judging. I’ve got a weakness for a good kettle chip.

Rao’s Homemade, though? That’s a different story. It’s surpassing $1 billion in annual sales. That’s a lot of marinara. People will always need pasta sauce. It’s a universal truth. It’s the one constant in a chaotic world.

Really, Campbell’s strength lies in those cooking-focused brands. It’s the stuff you add to meals, not the stuff you just grab and eat while scrolling through TikTok.

Management noted that even their condensed soups are seeing growth, particularly the classic cooking varieties like cream of mushroom and cream of chicken. Turns out people still make casseroles. Who knew? Rao’s is the same story. It’s an ingredient, not a meal replacement. It’s a subtle distinction, but it’s important.

Down But Not Out (Yet)

Campbell’s is stumbling because they haven’t quite figured out how to execute on what is, frankly, a pretty solid portfolio of brands. They’ve got the building blocks. They just need to, you know, build something with them. There’s still hope, though.

Here’s the kicker: their fiscal 2026 earnings per share guidance is still higher than their annual dividend payment. That’s a good sign. The sell-off has pushed the valuation to multi-decade lows and the yield to multi-decade highs. It’s a bit gloomy, yes, but that also means there’s potential value here.

Now, they need to lean into those meal brands. Focus on value and health-conscious consumers. Reduce the marketing spend on things people don’t actually need. And those “better-for-you” snack brands like Cape Cod and Kettle? Those are a good start.

All told, Campbell’s stands out as a compelling value stock for patient investors who believe that the company’s challenges are temporary setbacks, not a sign of impending doom. It’s not glamorous, it’s not exciting, but it’s a solid company with a history of paying dividends. And sometimes, that’s all you need. It’s the comfort food of the investment world.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Gold Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Building Agents That Learn and Improve Themselves

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 18 TV Series Filming Rehearsals as Bonus Content

- Trading Crypto with AI: A New Approach to Portfolio Management

2026-03-15 09:32