Warren Buffett, a gentleman whose investment acumen has, for decades, defied the generally accepted laws of financial physics, has stepped away from the helm of Berkshire Hathaway. (One suspects he’s gone to find a really good cup of tea, or perhaps to calculate the precise probability of a rogue asteroid impacting the stock exchange. It’s a toss-up, really.) The legacy, naturally, is… substantial. From a failing textile operation – a fate that befalls most textiles, eventually – to a conglomerate of almost unimaginable scope, it’s a story that suggests either extraordinary skill or an improbable alignment of cosmic forces. The numbers, of course, are rather insistent: a 6,099,294% increase in value. (Which, if you think about it, is almost certainly a rounding error. Everything is, at a certain level of magnification.)

But it’s not the past that’s particularly interesting, is it? It’s the present, and the rather peculiar signals Mr. Buffett appears to have been sending with his final acts as CEO. Signals that, when decoded, suggest a distinct lack of enthusiasm for the current state of… well, everything. And the primary method of communication? A truly staggering pile of cash. Specifically, $373 billion. (That’s a lot of pennies. If you laid them end-to-end, they’d probably circle the Earth several times, assuming you had a sufficiently motivated team of penny-layers and a planet willing to cooperate.)

The $373 Billion Question

This isn’t just a bit of spare change, you understand. It’s a new record for Berkshire Hathaway. Up from $321 billion the previous year, and a mere $129 billion before that. The accumulation didn’t happen by accident. It’s the result of a sustained program of selling stocks (including, rather surprisingly, Apple and Bank of America, both of which had previously performed rather well), and a distinct reluctance to buy anything else. (Imagine a very discerning shopper, wandering through a supermarket filled with suspiciously shiny produce, and deciding, on principle, to just take the money and go home.)

The tax implications were, naturally, a factor. Lower corporate tax rates presented an opportunity to realize gains. (Tax avoidance, it’s worth noting, is a perfectly legitimate strategy. It’s just that most people prefer to think of it as “efficient capital allocation.” Semantics, really.) But it wasn’t just about taxes. Mr. Buffett, it seems, felt that Apple and Bank of America, while still perfectly adequate companies, were… fully valued. (A polite way of saying they were expensive. Like a slightly overpriced cup of coffee. Still drinkable, but you’re aware you’re paying a premium.) He could have repurchased those shares, of course, avoiding any tax implications. But he didn’t. He let the cash pile up, patiently waiting for something… more reasonable. (Like a particularly good sale on sensible shoes.)

The implication, rather starkly, is that Mr. Buffett believes almost everything else is also overvalued. If he saw genuine value, he’d have bought it. (It’s a simple principle, really. Like noticing a dropped twenty-dollar bill. You pick it up.) Even his own stock, Berkshire Hathaway, wasn’t deemed worthy of repurchase. (A curious decision, perhaps. Like refusing a perfectly good slice of pie.)

As he himself noted in his final letter to shareholders, “Often, nothing looks compelling.” A sentiment that seems to have resonated for the last three years. He’s preparing for a period where opportunities will exist. And history, as it often does, might just be about to rhyme. (Though, of course, history is notoriously unreliable. It’s mostly just a collection of anecdotes and half-remembered details, filtered through the biases of the narrator.)

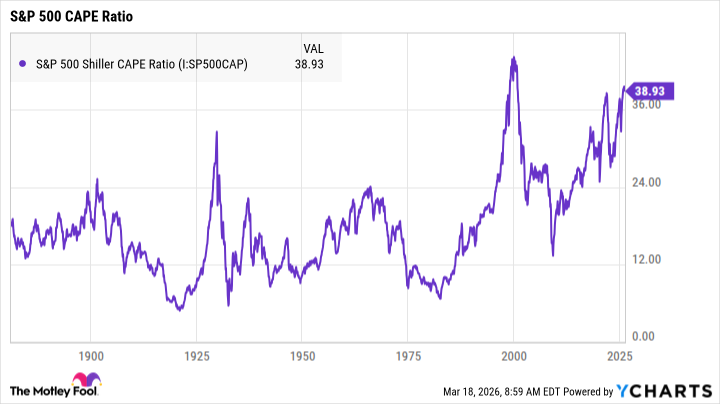

What the History Books (Might) Say

Several valuation metrics suggest that stocks, as a group, are… optimistic. Mr. Buffett’s preferred metric, market-cap-to-GDP (the “Buffett Indicator”), is currently hovering around 217%. (A number that, frankly, feels slightly arbitrary. Like measuring the length of a cloud.) While there are reasons for this to be higher than in the past, it still suggests a degree of… exuberance. (A polite way of saying “bubble.”)

Then there’s the Cyclically Adjusted Price-Earnings (CAPE) ratio, developed by Robert Shiller. It divides the current price by the average earnings of the previous ten years, adjusted for inflation. The current CAPE ratio for the S&P 500 is 38.8. (Which, if you consider the inherent limitations of averaging anything over a decade, is probably meaningless.)

Historically, whenever the S&P 500’s CAPE ratio has exceeded 38.8, the S&P 500 has produced negative returns over the next ten years. Robert Shiller himself anticipates annualized returns of just 1.5% over the next decade. (Which, after inflation, is essentially nothing. Like spending an hour meticulously arranging pebbles.)

There’s a catch, naturally. The only other time the S&P 500 CAPE ratio exceeded 38.8 was during the height of the dot-com bubble. Drawing conclusions from that period, which included a spectacular bubble burst and a rather unpleasant financial crisis, might be… unwise. (The past, as they say, is a foreign country. And they do things differently there.)

Mr. Buffett, a seasoned student of history, markets, and human psychology, is well aware of this. Still, he found little value in the current market. Investors willing to do their research can still find opportunities, though. Perhaps by looking at companies Mr. Buffett ignored. He famously avoided many tech stocks, and Berkshire’s size limited its investment universe. (It’s difficult to steer an ocean liner with the precision of a rowboat.)

Increasing your cash allocation might be prudent, but selling everything and waiting for a downturn would be… extreme. Mr. Buffett still held a $300 billion equity portfolio when he retired. (A sensible precaution. One doesn’t want to be caught unprepared when the universe decides to throw a curveball.)

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Directors of 2025

- 15 Films That Were Shot Entirely on Phones

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

2026-03-22 01:05