The opening months of the year have proven…unsettled for those invested in Broadcom (AVGO 1.55%). A decline of ten percent, a modest misfortune in the grand scheme, yet enough to separate it from the generally ascendant mood of the PHLX Semiconductor Sector. One observes a certain…hesitation, a reluctance to embrace the future with unbridled enthusiasm, as if the very air crackles with unspoken doubts.

Much of this disquiet stems, of course, from the pervasive anxieties surrounding artificial intelligence. The breathless pronouncements, the vast expenditures…it all feels precariously balanced, a gilded edifice built upon shifting sands. And Broadcom, inevitably, finds itself caught in the crosscurrents. The whispers that accelerating sales of AI-related products might, paradoxically, compress margins have not helped, though one suspects the market is often given to such illogical fears.

Yet, to focus solely on these present shadows is to ignore the quiet strength Broadcom has demonstrated. The fiscal year 2025 concluded with record revenues, a fact often lost amidst the clamor for the next innovation. And the indications suggest an even more robust performance in the current year. It would not, therefore, be entirely surprising to witness a renewed vigor in the stock following the release of the first-quarter results on March 4th. A subtle stirring, perhaps, rather than a dramatic upheaval.

A Landscape of Orders

Broadcom’s own projections anticipate a revenue of $19.1 billion for the first fiscal quarter, a potential increase of twenty-eight percent. But these figures, while respectable, only hint at the underlying currents. The company concluded fiscal 2025 with a backlog of $162 billion – a veritable landscape of orders – with $73 billion specifically allocated to AI chips. A considerable sum, suggesting a demand that extends beyond mere speculation.

Management anticipates clearing this AI-related backlog over the next six quarters, translating to a quarterly revenue run rate exceeding $12 billion. Thus, an exceeding of the projected $8.2 billion in AI revenue for the first quarter appears not merely plausible, but almost inevitable. A gentle swell, lifting the overall revenue figures in its wake.

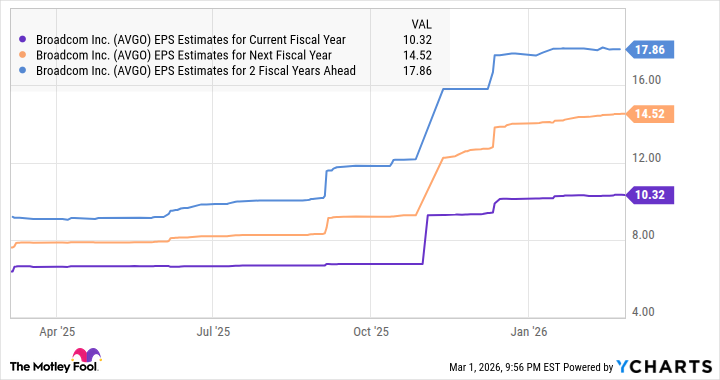

Wall Street, too, appears to acknowledge this potential. The consensus revenue estimate for fiscal 2026 stands at $97.6 billion – a fifty-three percent improvement over the previous year. Broadcom’s growth, it seems, is poised to accelerate, leaving behind the slower pace of the previous period. A quiet blossoming, unfolding over time.

Analysts foresee a similar surge in earnings, far surpassing the modest fourteen percent growth observed in the average S&P 500 company. A subtle distinction, yet one that speaks volumes about Broadcom’s underlying strength.

An Investment, Considered

Broadcom currently trades at 32 times forward earnings. A premium, certainly, compared to the S&P 500’s multiple of 22. But a justifiable one, given the anticipated surge in earnings over the coming years. A price reflecting not merely present value, but future potential.

The median price target of $458, suggesting a potential increase of forty-three percent from current levels, speaks to this optimism. And the overwhelming consensus among analysts – ninety-six percent rate the stock as a buy – further reinforces this view. It would seem, therefore, that a consideration of Broadcom, particularly while it remains somewhat undervalued, is a prudent course of action. A quiet accumulation, perhaps, rather than a frantic rush.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

2026-03-03 20:26