The recent unpleasantness in the Levant – let’s call it a ‘robust disagreement’1 – has, predictably, caused a bit of a wobble in the markets. Investors, being much like flocks of startled pigeons, have a regrettable tendency to sell first and ask questions… well, rarely. It’s a primal urge, really. A deeply ingrained suspicion that anything going ‘up’ must, eventually, come crashing down. Which, statistically speaking, is often true. But not always.

The usual suspects have been at play: oil prices doing their impression of a startled cobra, a frantic rush to anything shiny and traditionally considered ‘safe’ (gold, silver, and the increasingly popular habit of hiding under the duvet), and a predictable boost for those who manufacture things that go ‘boom’. However, a closer look reveals that many companies, caught in the crosscurrents, are less affected than the headlines suggest. Morgan Stanley’s wizards2 have pointed out, with the sort of hindsight that’s always impeccably clear, that markets tend to shrug off these sorts of disruptions. In fact, they’ve historically been up a bit after a month, a good deal more after six, and positively buoyant after a year. Go figure.

Which brings us to the rather sensible notion of blue-chip stocks. The sturdy oaks of the financial forest, if you will. Companies that, while not immune to the occasional gale, are generally built to withstand a bit of buffeting. Apple and Williams Companies, for instance. Both have recently experienced a bit of a dip, and both, in my humble (and professionally informed) opinion, are currently being undervalued. A bit like finding a perfectly good dragon scale at a flea market.

Why Apple Isn’t Just a Fruit

Apple, despite only being a public entity since 1980 (a mere blink in the eye of geological time, let alone corporate history), has become the archetypal blue chip. With a market capitalization of $3.85 trillion, it’s the second-largest company in the world, trailing only Nvidia.3 It possesses a comforting level of stability, bolstered by over $35.9 billion in cash and short-term investments. Enough, one suspects, to buy a small country. Or at least a very large collection of novelty socks. It’s a growth stock, certainly, but it also demonstrates a commendable commitment to returning value to shareholders through dividends and share buybacks – a practice akin to politely handing money back to the people who gave it to you in the first place.

An Overreaction? Surely.

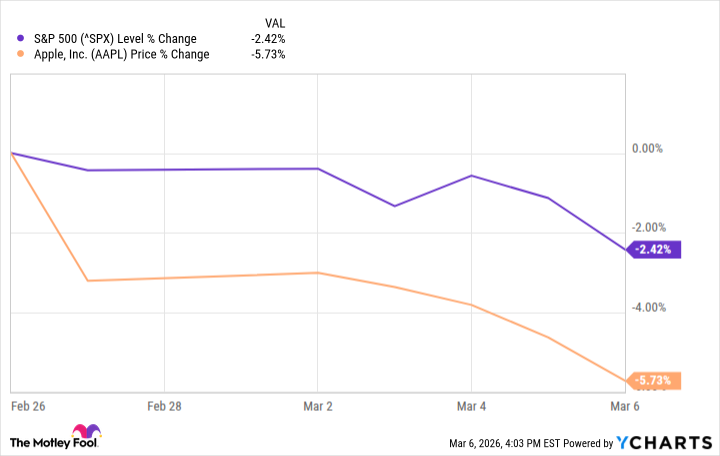

As of Friday’s close, Apple’s stock had fallen nearly 6% since February 26th, while the S&P 500 experienced a more modest decline of around 2.4%. A disproportionate reaction, wouldn’t you say? Especially considering that Apple, being a vertically integrated technology lifestyle brand, isn’t particularly sensitive to oil prices. A sustained economic downturn would, of course, impact its business, as it would nearly any company that relies on people having disposable income. But the current dip feels… excessive.

Apple’s first fiscal quarter of 2026 saw record revenue of $143.8 billion – a 16% year-over-year increase. Earnings per share (EPS) grew 19% to a record $2.84. Numbers that, frankly, make most accountants weep with joy.

There’s been some grumbling about Apple’s perceived slowness in the artificial intelligence (AI) race, particularly concerning delays in enhancing Siri. However, some argue that this is a shrewd move. Perhaps they’re wisely avoiding a costly and potentially fruitless arms race. It’s a bit like refusing to participate in a goblin poetry slam – a perfectly sensible decision, really.

The iPhone, Apple’s flagship product, continues to defy expectations. CEO Tim Cook recently described global demand as “staggering” – a claim supported by a 23% year-over-year revenue increase and record sales across all geographic regions. The iPhone 17 family, it seems, is proving rather popular. Accounting for 59% of Apple’s total revenue, it’s a significant engine of growth.

Apple is also attempting to expand its customer base by offering more affordable products, such as the MacBook Neo and the iPhone 17e, both priced at $599. A commendable effort, even if it does involve lowering oneself to cater to the… less discerning consumer.

Williams Companies: The Unsung Hero

Williams Companies, with a market cap of $93 billion, is considerably smaller than Apple. However, its history is far deeper, stretching back to 1908. It’s a blue chip within the energy and infrastructure sector, and has consistently raised its dividends for eight consecutive years, including a 6% increase this year. Currently, it offers a yield of around 2.7% – a comforting return in these uncertain times.

Its natural gas infrastructure provides a degree of stability, as it operates through long-term, fee-based contracts. This ensures predictable cash flows, and its position as a midstream player shields it from the volatility of oil prices. It’s a bit like being a toll collector on the highway of energy – reliably profitable, even when everyone else is arguing about the price of gas.

A Dip That Doesn’t Add Up

Williams Companies’ stock fell to $74.22 on Friday, a 3.3% drop from its recent high of $76.75. A seemingly insignificant fluctuation, especially considering the company’s long-term strength. A minor wobble, easily explained by the general market jitters. Or perhaps a rogue gnome short-selling the stock.

Williams Companies handles approximately one-third of the natural gas consumed in the United States. Its 33,000-mile pipeline network operates entirely within domestic borders, providing a natural hedge against… well, against whatever tariffs happen to be in vogue. This geographic focus, coupled with its long-term contracts, ensures a steady and dependable stream of cash flow, supporting 13 consecutive years of growth in adjusted EBITDA.

The company’s 2025 performance was particularly robust, with adjusted EBITDA rising 9% to $7.8 billion and total revenue climbing 13.7% to $11.9 billion. This translated to a 17.5% increase in EPS to $2.14, and a stock price increase of over 23% year-to-date. Much of this momentum is fueled by the rapid buildout of new data centers, which increasingly rely on natural gas power plants. A colder-than-usual winter across the eastern U.S. also contributed, driving up natural gas consumption for heating.

Williams Companies continues to prioritize shareholder returns, having paid out dividends for 52 consecutive years. Its distributions are covered 2.4 times by its adjusted funds from operations, underscoring the safety of the current payout and providing flexibility for future increases.

1

A ‘robust disagreement’ is a term favored by diplomats and those wishing to avoid saying ‘war’. It implies a polite argument over tea and biscuits, rather than a large-scale conflict involving explosions and unpleasantness.

2

Morgan Stanley’s wizards are, of course, highly trained financial analysts. But ‘wizard’ sounds more impressive, doesn’t it?

3

Nvidia, currently the largest company in the world, is rumored to be building a secret lair beneath the Nevada desert. But that’s just a rumor. Probably.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Spotting the Loops in Autonomous Systems

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- Silver Rate Forecast

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-07 14:04