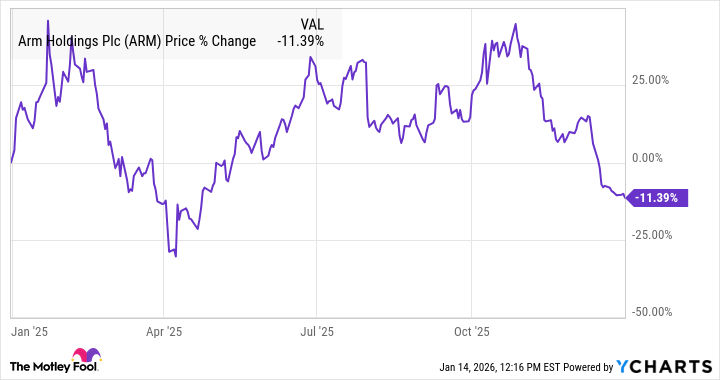

Let me be clear: investing is like dating someone who texts in all caps. You’re excited, confused, and slightly humiliated by your own choices. Case in point? Arm Holdings (ARM) in 2025. A stock that danced like a penguin on a trampoline-chaotic, charismatic, and ultimately a 11% loss for the year. But hey, at least it wasn’t NFTs. Yet.

S&P Global Market Intelligence says it all: 11% down, folks. A number that makes you question if you’ve accidentally sold your kidney to a shadowy figure on the internet. And the chart? A Jackson Pollock painting if ever there was one. Up, down, sideways-Arm spent most of the year pretending it wasn’t worried about an AI bubble, which, honestly, is like ignoring the elephant in the room… while the elephant texts you passive-aggressive tweets.

Arm’s Rollercoaster: Stargate, Tariffs, and Existential Dread

Arm started 2025 like it was auditioning for a Marvel movie. The Stargate Project-a $500 billion AI extravaganza with Nvidia, Oracle, OpenAI, and Softbank-had everyone whispering, “Genius!” until March hit. Then came the “Liberation Day” tariffs, which sent the stock into a nosedive faster than my bank account after I clicked “buy” on that suspiciously cheap YSL lipstick.

But! The stock bounced back, briefly, like a stubborn toddler refusing to nap. Then, poof! Earnings guidance that made investors groan louder than my roommate’s existential crisis over her Spotify Wrapped. And let’s not forget the AI bubble-because nothing says “confidence” like a stock valuation that makes you wonder if you’ve accidentally priced it in cryptocurrency. 🤷♂️

Here’s the kicker: Arm doesn’t sell chips. It licenses them. Picture this: You’re a landlord collecting rent from tenants who’ve turned your apartment into a black hole of innovation. They (Nvidia, etc.) build the future; you collect royalties. It’s a solid gig… if you don’t mind growing at half the speed of your peers while they party like it’s 2021. Again.

In its first half of fiscal 2026, Arm reported 24% revenue growth. But licensing is a fickle lover-revenue spikes one quarter, vanishes the next. It’s the financial equivalent of a hot flash: exciting, confusing, and best discussed in hushed tones with a glass of wine.

Yet! There’s hope. Arm’s new Compute Subsystems (CSS) are like giving your tenants a toolbox and saying, “Go build a spaceship.” And the cloud partnerships? Microsoft, Alphabet, Amazon-big names with bigger appetites. If this goes well, Arm could be the unassuming barista who ends up marrying a tech mogul. If not? Well, at least you’ll have the merch.

The Road Ahead: Optimism, Anxiety, and a Side of ROI

Arm’s guiding for $1.225 billion in Q3 revenue-a 24% jump. Adjusted EPS? Up to $0.41. Numbers that make you want to high-five your screen… or question why you’re high-fiving your screen. The bottom line? Investors crave more. And honestly, who can blame them? This isn’t exactly the financial equivalent of a Michelin star-it’s more like a five-star review for a gas station burrito.

But here’s the wealth-builder whisper: Arm’s got moats. Deep ones. Licensing dominance, AI bets, and a business model that’s less “get rich quick” and more “get rich slowly while sipping chamomile tea.” It’s not sexy. It’s not viral. But if you’re in it for the long game, Arm’s play might just be the calm before the next AI storm. Or, you know, another hurricane. Shrug emoji here.

Either way, the market’s a rom-com: full of twists, cringe, and the nagging feeling you’ve missed the plot. But if you’re smart, you’ll watch it with popcorn-and a fire extinguisher. 🙃

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- Trading Crypto with AI: A New Approach to Portfolio Management

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 15 Films That Were Shot Entirely on Phones

2026-01-14 21:43