They speak of artificial intelligence as a coming dawn, a boundless engine of progress. But every dawn casts a shadow, and this one falls upon the backs of those who lay the wires and cool the machines. Applied Digital, they call it. A name that promises much, delivers… potential. The question isn’t whether AI will change the world, but who will profit from the wreckage, and at what cost.

This company, barely three years old, has ridden the wave of AI hype to a valuation that would make a seasoned speculator blush. Five hundred percent in twelve months. A dizzying ascent, built on the promise of “neoclouds” – a new breed of digital landlord, leasing space to those who dream in algorithms. It’s a beautiful story, if you ignore the foundations. Or, rather, the lack thereof.

The market predicts a surge in AI infrastructure, from $59 billion to $356 billion by 2032. A tempting figure, enough to lure any gambler. But numbers on a page are ghosts. The real story is in the concrete, the steel, the relentless demand for power. And power, my friends, is never free.

The Hunger of the Machines

Applied Digital understands the hunger. They see the need for massive computing power, for liquid cooling systems that resemble the veins of a leviathan, for connections faster than a thought. They offer a solution: data centers, crammed with servers, humming with energy. They boast of ample power capacity, a rare advantage in a world bracing for shortages. Less than 10% of competitors can match them, they claim. A boast, perhaps, or a warning.

They’re expanding, breaking ground on new sites. A flurry of activity, fueled by investor enthusiasm and, increasingly, by debt. They’re building castles in the cloud, but the sand beneath their feet is shifting. North Dakota, and other locales, become the new frontiers of digital extraction. A modern gold rush, with servers instead of shovels.

The Illusion of Profit

Sales are up, of course. 250% year over year. A dazzling number, masking a simple truth: they’re selling potential, not profit. CoreWeave, one of their major clients, has signed leases worth $11 billion over fifteen years. A long-term commitment, a lifeline. But lifelines can fray, and fifteen years is a long time in the digital age.

They’re not just landlords, they claim. They’re also a “neocloud provider,” spinning off a new company called ChronoScale. A clever maneuver, a way to capture more of the value chain. ChronoScale will compete directly with CoreWeave, offering AI compute to the hyperscalers – the giants who control the algorithms. A battle of titans, fought on the backs of data centers and the patience of investors.

But beneath the veneer of innovation lies a harsh reality. Building and operating AI-powered data centers is expensive. The cost of revenue has soared, up 344% year over year. Operating losses are mounting, more than doubling from the previous year. And the debt… the debt is a shadow that grows longer with each new server.

Over $2.6 billion in debt. A staggering sum, a testament to the insatiable appetite of the machines and the willingness of investors to feed them. It’s a precarious position, a house built on borrowed money and the hope of future profits.

A Gamble for the Few

If Applied Digital continues to accumulate debt, it risks becoming another casualty of the AI boom. The interest payments will mount, the profits will remain elusive, and the house of cards will tremble. It’s a simple equation, one that many have ignored in the rush to embrace the future.

If, however, they can secure additional long-term leases, they might gain a foothold in this new landscape. If they can navigate the treacherous waters of debt and competition, they might transition into a profitable business. But it’s a long shot, a gamble for the few who believe in the promise of AI and the resilience of the market.

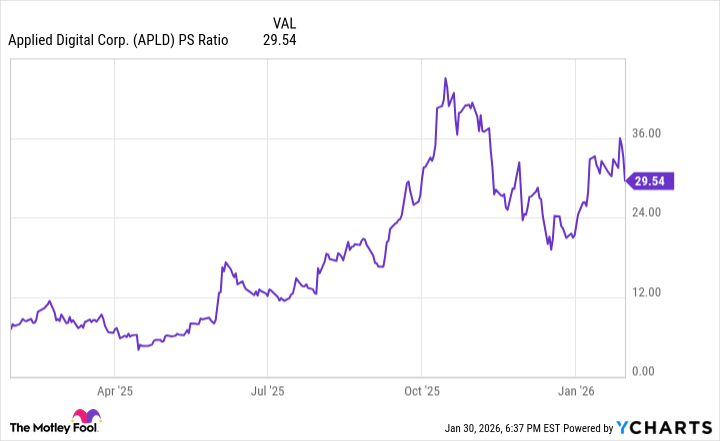

The price-to-sales ratio, they say, can offer some insight. A measure of how much investors are paying for every dollar of revenue. It’s on an upswing, they claim, suggesting that the stock is overvalued. A warning sign, a reminder that the market is often driven by hype rather than reality.

Wait for the share price to drop, they advise. Wait for the market to cool down. But even then, Applied Digital’s high debt and lack of profits make it a risky proposition. A gamble for those with a high tolerance for risk, and a willingness to bet on the future. A future that, for many, remains shrouded in shadow.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- Trading Crypto with AI: A New Approach to Portfolio Management

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 15 Films That Were Shot Entirely on Phones

2026-02-04 01:04