![]()

The feverish pursuit of artificial intelligence, a digital alchemy promising boundless progress, has gripped the largest of our technological behemoths. Billions are being diverted, fortunes wagered on the construction of data sanctuaries – vast, power-hungry cathedrals dedicated to the processing of information. Five companies alone, in their collective ambition, have pledged some seven hundred billion dollars for the year 2026, a sum that speaks not of innovation, but of a desperate, almost panicked, expenditure. Many, observing this relentless consumption, rightly harbor a disquiet, a sense that such profligacy cannot long sustain itself.

Yet, amidst this collective delirium, one company stands apart, a deliberate anomaly. Apple, a name synonymous with carefully cultivated desire, has chosen a different path. While others amass digital legions, building empires of silicon and electricity, Apple maintains a studied restraint. Its capital expenditures, last year a mere twelve billion dollars, represent not a lack of ambition, but a different calculus, a recognition that true value lies not in the sheer volume of investment, but in the judicious application of resources. And this, it appears, is a divergence that may yield a surprising reward.

The Company That Refuses the Race

There exists, among the titans of technology, a prevailing belief that relentless advancement, a constant striving for the ‘bleeding edge,’ is the sole guarantor of success. Apple, however, has repeatedly demonstrated the fallacy of this assumption. The company, architect of the iPhone, the Apple Watch, and the AirPods, has proven that enduring market leadership can be achieved not through reckless innovation, but through a persistent refinement of existing strengths. It is a lesson often overlooked in the current climate of breathless enthusiasm.

While others clamor for dominance in the artificial intelligence arena, Apple is perceived, rightly or wrongly, as a laggard. But this perceived delay is, in truth, a strategic positioning. The company, recognizing the inherent instability of this nascent technology, has chosen to observe, to refine, to integrate only when the time is truly ripe. It is a position of relative safety amidst the escalating arms race, a haven for those seeking stability in a world increasingly defined by disruption. The consumer desire for Apple’s products remains steadfast, and sustaining this demand requires not colossal expenditures, but a continued commitment to quality and design.

Last quarter, iPhone sales rose by twenty-three percent, driven by a particularly strong surge in China – a thirty-eight percent increase. Management anticipates this demand will persist, yet finds itself constrained by supply – a dependence on chips from Taiwan Semiconductor Manufacturing. TSMC, itself burdened by the insatiable appetite of the hyperscalers, struggles to meet the growing demand. Constraints in the memory chip market also present a challenge, a modest impact on gross margins expected in the coming quarters. Yet, despite these hurdles, Apple projects revenue growth of thirteen to sixteen percent for the current quarter – a testament to the enduring strength of its brand and its ability to navigate even the most challenging of circumstances.

Further bolstering demand may be the anticipated revamp of Siri, Apple’s digital assistant. The promised integration of generative AI capabilities, the ability to synthesize data across applications, holds the potential to unlock new levels of functionality. This, however, will necessitate newer iPhones, triggering a potential upgrade cycle, a renewed surge in demand for more capable, higher-end models. It is a calculated gamble, a leveraging of existing strengths to drive future growth.

Meanwhile, Apple’s services segment continues to flourish, growing by fourteen percent. This high-margin business, bolstered by AI capabilities integrated across applications and devices, drives App Store sales and opens avenues for new AI-related offerings. It is a stabilizing force, a counterweight to the volatility of the hardware market, a source of consistent, predictable revenue.

All this is to say that Apple is delivering solid financial results. But the true advantage lies in its relatively modest capital expenditure budget, a deliberate restraint that sets it apart from its peers. It is a strategy that may well lead to strong performance in 2026, a quiet triumph amidst the cacophony of excess.

The Fortress and the Spendthrifts

Apple is poised to generate even more free cash flow in 2026 than it did in 2025 – a staggering one hundred and twenty-three billion dollars. Meanwhile, the hyperscalers, consumed by their relentless pursuit of AI dominance, are bracing for a precipitous decline in free cash flow. Amazon, for example, is projected to experience negative free cash flow in 2026, a consequence of its two hundred billion dollar capital expenditure plan. Meta Platforms faces a similar fate, with free cash flow expected to plummet by ninety percent, a result of a seventy-two percent increase in capital expenditures. It is a stark contrast, a tale of two strategies – one of prudent restraint, the other of reckless abandon.

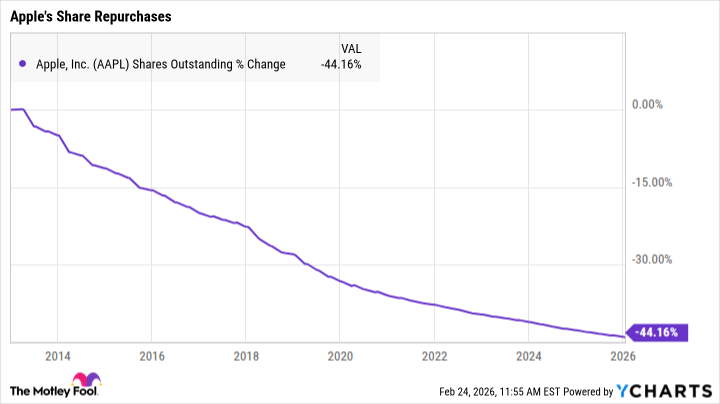

Instead of squandering its resources on data centers, Apple can return capital to shareholders. Its primary vehicle for doing so is share repurchases. Since Tim Cook assumed leadership, Apple has repurchased over seven hundred billion dollars of its own stock, reducing the total share count by more than forty-four percent. This reduction in share count amplifies earnings per share, even as revenue and net income growth moderate. By retiring shares, Apple has increased earnings per share by seventy-nine percent – a testament to the power of disciplined capital allocation.

Amazon, Meta, and their counterparts also possess share repurchase authorizations. But with vast sums committed to capital expenditures, they are unlikely to utilize them effectively. Moreover, both companies rely heavily on share-based compensation, necessitating even greater repurchases simply to offset the dilution of employee stock incentives. Amazon’s shares outstanding have actually increased over the past three years, while Meta’s have barely budged. It is a perverse irony – companies ostensibly focused on innovation actively diminishing shareholder value through excessive dilution.

Meta notably spent twenty-six point three billion dollars on share repurchases last year, yet its shares outstanding fell by a mere zero point one percent. Significantly, Meta ceased repurchasing shares in the fourth quarter as capital expenditures accelerated, suggesting investors should not anticipate further buybacks in 2026. It is a telling sign – a company prioritizing short-term investment over long-term shareholder value.

As a result, Apple can deliver strong earnings-per-share growth even with modest operating results. Moreover, it avoids the uncertainty and inherent risks associated with unproven technologies and excessive debt. This stability may attract investors seeking a safe haven in a turbulent market, leading to outperformance in the year ahead. It is not a tale of spectacular innovation, but of quiet resilience, of a fortress built on prudence, weathering the storm while others are swept away.

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- The Best Directors of 2025

- Brent Oil Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

2026-02-27 18:54