For some time now, the question of whether Artificial Intelligence is a genuine technological leap forward or merely a particularly elaborate form of digital charades has occupied the minds of… well, people who have minds to occupy. The answer, as is often the case with things involving both electricity and excessive optimism, depends entirely on who you ask. What is becoming increasingly clear is that AI tools have insinuated themselves into the daily routines of a surprising number of individuals, and are unlikely to vanish in a puff of logic gates anytime soon. (Though, of course, nothing is truly certain. The universe is, after all, under no obligation to make sense.)

It’s worth noting that a great many companies currently claiming to be at the forefront of this revolution will, with a high degree of probability, not be. They will either be absorbed by larger entities, quietly cease to exist, or discover that their groundbreaking technology is actually quite good at making toast. (A perfectly respectable application, admittedly, but not exactly world-changing.) Therefore, if one is contemplating an investment in AI-related stocks, a degree of caution is advised. Focusing on companies built to endure, regardless of which particular AI fad currently holds sway, is generally considered a sensible strategy. We shall examine two such entities, each playing a distinctly different role in this unfolding saga.

1. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (TSM 1.86%), or TSMC for those who prefer brevity (a rare commodity these days), isn’t, strictly speaking, an “AI stock” in the traditional sense. It doesn’t offer apps that generate recipes or curate playlists, nor does it assist in the creation of “vibecodes” (whatever those are). However, it occupies a position of quite extraordinary importance in the entire AI ecosystem. (Think of it as the plumbing of the digital world. Essential, often overlooked, and prone to occasional catastrophic failure.)

TSMC is, in essence, a semiconductor foundry. Companies design their chips – intricate patterns of silicon and hope – and then outsource the actual manufacturing process to TSMC. Apple relies on them for the chips that power iPhones, AMD for processors, and Nvidia for its graphics processing units (GPUs). It’s the largest foundry in the world by a considerable margin. (A margin that, one suspects, is measured in kilometers of silicon wafer.)

The functioning of AI, as we currently understand it, depends on an awful lot of physical hardware. GPUs, central processing units (CPUs), and specialized AI accelerators all contribute to the complex calculations required. These components aren’t conjured from thin air, of course. They require manufacturing, and TSMC is, for the foreseeable future, the dominant force in that particular realm. Estimates suggest that its market share in the advanced AI chip industry is well into the upper 90% range. (Which means that, statistically speaking, if you have an AI chip, it probably came from TSMC. Don’t overthink it.)

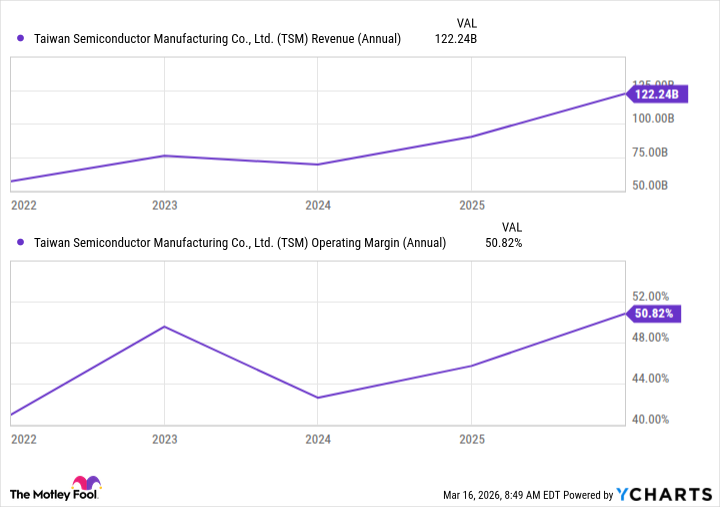

The recent surge in demand for AI chips has, unsurprisingly, benefited TSMC. In 2025, revenue increased by nearly 36% to $122.4 billion. Gross margins rose from 56.1% to 59.9%, operating margins from 45.7% to 50.8%, and cash flow increased by over 24%. (These numbers are, of course, subject to the usual caveats regarding accounting practices and the inherent unpredictability of the global economy.)

TSMC’s position as the go-to manufacturer grants it a degree of pricing power, allowing it to capitalize on the current AI infrastructure rush. (This is not to suggest that they are deliberately exploiting the situation, merely that they are responding to market forces. Which, let’s face it, are rarely benevolent.) If one is seeking exposure to AI without having to bet on a particular software “winner,” TSMC represents a relatively stable, if somewhat unglamorous, option.

2. Amazon

Most people associate Amazon (AMZN 2.47) with its e-commerce business. However, it also operates Amazon Web Services (AWS), one of the world’s most important cloud platforms, powering countless websites and applications. (It’s rather like a digital utility, providing the infrastructure that keeps the internet humming. Though, unlike a traditional utility, it also sells you books and cat food.)

Amazon is one of a handful of “hyperscalers” – large-scale cloud providers that supply much of the computing power required by AI. The company plans to invest around $200 billion in capital expenditures in 2026, much of which will be directed towards building AI infrastructure and expanding capacity. (A considerable sum, even by the standards of companies that routinely sell things to each other online.) The goal is to accommodate more customers looking to develop their own AI tools.

This involves not only building more data centers (vast warehouses filled with servers) but also developing in-house AI chips to reduce reliance on third-party companies like Nvidia. Amazon currently has the AWS Trainium chip (focused on machine learning), the Graviton chip (for general cloud workloads), and the Inferentia chip (a lower-cost option). (The proliferation of specialized chips is, one suspects, a sign that we are entering a new era of technological complexity. Or perhaps just a marketing ploy.)

The more Amazon can do in-house – whether it’s developing its own chips, owning its own data centers, or creating its own AI models – the more it can cut costs and reinvest those savings. (A perfectly rational strategy, assuming that the cost of doing everything in-house doesn’t exceed the cost of outsourcing.)

There have been concerns about Amazon’s spending plans, but the company is playing the long game and has the financial resources to do so. In 2025, it surpassed Walmart as the world’s highest-revenue public company, generating $716.9 billion in revenue. Its other segments continue to grow as well. (A testament to the power of relentless expansion and efficient logistics.)

Amazon’s stock has experienced a rocky start to 2026 (down over 8% year-to-date through March 16), but the long-term appeal remains strong. (Though, as any seasoned investor will tell you, past performance is no guarantee of future results. The universe is, after all, under no obligation to be predictable.)

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- The Best Former NFL Players Turned Actors, Ranked

- ONE PIECE Season 2 Confirms Sanji’s OTHER Backstory in the Live-Action

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

2026-03-18 23:04