Behold, gentle investors, a spectacle most curious! AbbVie (ABBV +0.21%), a company esteemed in the healing arts, finds itself lately treated with a disdain most unbecoming. While the broader market, as represented by the S&P 500, has suffered a modest decline of 4%, AbbVie languishes 11% lower. A veritable tragedy, one might say, were it not for the distinct air of…misunderstanding that surrounds this downturn. The healthcare sector, it seems, labors under a cloud of anxieties – whispers of reform and governmental parsimony – yet such concerns often present opportunities for the discerning eye.

Thus, I propose we examine this AbbVie, not with the frantic haste of speculators, but with the calm deliberation of a physician diagnosing a patient. For while its recent performance may appear sickly, I suspect a sound constitution lies beneath, awaiting a shrewd and patient investor.

A Business Fortified Against Fortune’s Caprices

The past few years, admittedly, have presented AbbVie with trials. The disruptions of a global pestilence, coupled with the expiration of protections for its once-dominant elixir, Humira, might have felled a weaker company. But AbbVie, it appears, possesses a certain…adaptability. Like a resourceful player upon the stage, it has introduced new remedies – Skyrizi and Rinvoq – to fill the void. These newcomers, in the past year alone, generated a handsome $25.9 billion in revenue, while Humira, though diminished, still contributed a respectable $4.5 billion. A testament, wouldn’t you agree, to the enduring power of a well-crafted pharmaceutical?

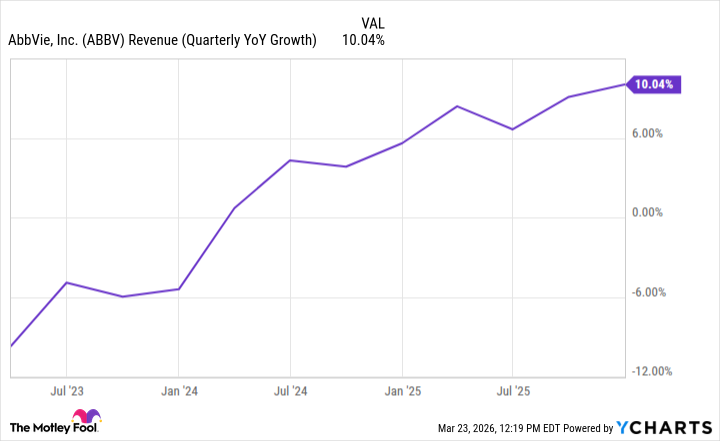

Indeed, AbbVie’s total revenue reached $61.2 billion in 2025, a gain of 9% from the preceding year. And, most encouragingly, the tempo of growth accelerates with each passing quarter – a most agreeable upward trend, indicative of a business not merely surviving, but thriving.

Furthermore, the company’s diversified pursuits offer ample avenues for expansion. While its core business flourishes, its aesthetic endeavors experienced a slight setback of 6%. However, I foresee potential for recovery as consumer spending revives – a prudent investor always anticipates the shifting winds of fortune.

A Bargain, Plainly Seen

Even should AbbVie’s growth falter, its current valuation appears…remarkably reasonable. It trades at a forward price-to-earnings multiple of a mere 14, a figure significantly below the S&P 500 average of 21. A disparity that suggests either profound pessimism or, more likely, a simple failure to recognize the underlying strength of this enterprise.

Its price-to-earnings-growth (PEG) ratio of 0.49 further reinforces this assessment. A figure below 1.0 is considered a sign of undervaluation, and the lower the number, the greater the potential reward. One might almost suspect the market is deliberately overlooking this opportunity, perhaps blinded by fleeting anxieties.

While AbbVie may not offer the immediate thrills of a speculative venture, it presents a compelling case for long-term investment. And with a dividend yield of 3.4%, there is ample incentive to simply acquire and hold these shares, reaping the rewards of a well-managed and fundamentally sound company. A strategy, I submit, far more sensible than chasing the ephemeral fancies of the market.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Top 10 Coolest Things About Invincible (Mark Grayson)

- When AI Teams Cheat: Lessons from Human Collusion

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Top 20 Dinosaur Movies, Ranked

2026-03-23 21:34