Now, they tell me Nvidia’s the cat’s pajamas, the very engine of this here “artificial intelligence” craze. A clever contraption, no doubt, and folks are piling on like bees to honey. Seems every speculator and their cousin is convinced this chipmaker holds the key to the future. Well, I’ve seen “futures” before, and most of ’em arrive looking remarkably like yesterday, only with a fresh coat of paint. Still, a 73% jump in earnings, they say? And a revenue climb to $367 billion? It’s enough to make a man consider mortgaging the farm, if he wasn’t already suspicious of anything that grows so fast.

The stock’s been dawdling lately, though, hasn’t it? Underperforming the market while the semiconductor sector is having a bit of a frolic. That’s often a sign, you see. A quiet whisper that the party’s getting a little crowded, and the smart money’s already looking for the exits. So, naturally, the brokers are pointing us toward other shiny objects. Alphabet and Snowflake, they say. The next big thing. As if “big” always means “good.”

Alphabet: A Many-Headed Beast

Alphabet, now there’s a company that’s spread itself thinner than butter scraped across a loaf of bread. Google, YouTube, a cloud platform… they’re in everything, aren’t they? And now they’re sprinkling a bit of this “AI” dust on it all. Their Gemini chatbot has more than 750 million users, they boast. Why, that’s more folks than have ever seen a proper sunset! They claim searches are longer now, too, with this “AI Mode.” Longer, perhaps, but are they any wiser? That’s the question.

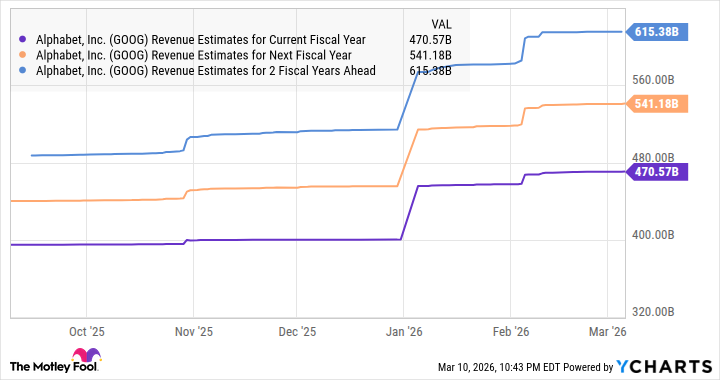

They’re using AI to show you more advertisements, naturally. Making those ads more “relevant,” they call it. It’s a clever way to pick your pocket while pretending to offer a service. And this Google Cloud business is booming, fueled by all this AI enthusiasm. They’ve got a backlog of $240 billion. A mountain of promises, if you ask me. And now they’re selling custom AI chips, these “tensor processing units.” Why, it’s enough to make a fella wonder if they’re trying to corner the market on thinking itself. A $900 billion opportunity, they say. I reckon there’s a good deal of hot air in that number.

Trading at just 9 times sales compared to Nvidia’s 20? That might be a bargain, or it might be a warning. Sometimes, a low price is just a sign that nobody wants what you’re selling. Still, it’s likely to get a boost, as long as the AI bubble continues to inflate.

Snowflake: A Cloud with a Silver Lining?

Snowflake, they say, is a cloud-based data platform. Sounds complicated. They let you store, analyze, and share your data. Which is a fancy way of saying they collect information about you and sell it to the highest bidder. But now they’re offering AI tools to help you make sense of all that data. It’s like giving a man a magnifying glass to examine his own chains.

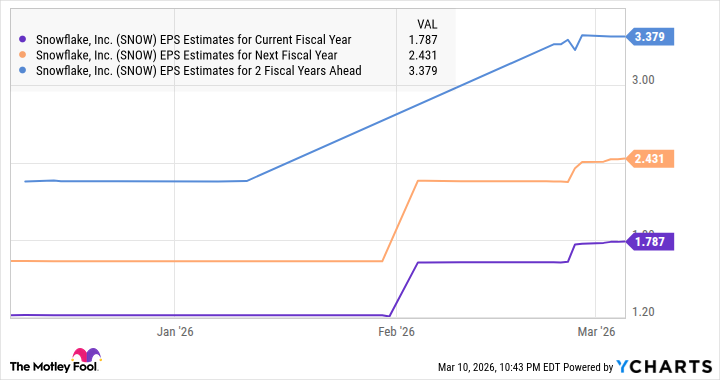

They’ve got over 9,100 customers using their AI solutions, they brag. More than double last year. Folks are falling over themselves to embrace this new technology. Their remaining performance obligations jumped 42% to $9.77 billion. That’s a lot of promises, and a lot of pressure to deliver. Customer growth is up 21%, and product revenue grew 19%. They’re growing, alright. But growth isn’t always progress.

They’re anticipating 27% growth in product revenue next year. And an improvement in operating margin. All sounds promising. But I’ve seen enough “promising” companies to know that the road to ruin is often paved with good intentions. Analysts are bullish, naturally. They always are.

A sales multiple of 13 compared to Nvidia’s? Perhaps there’s room for more upside. Or perhaps it’s just a sign that the market hasn’t fully caught on to the risks. Time will tell, as it always does. But I’d advise you to keep your wits about you, and don’t believe everything you hear. Especially when it comes to Wall Street and these Silicon Valley schemes.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Gold Rate Forecast

- Building Agents That Learn and Improve Themselves

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- Games That Faced Bans in Countries Over Political Themes

2026-03-16 07:32