One observes that Apple (AAPL +1.39%) has commenced the year with a distinct lack of panache. A mere seven percent decline, you say? Hardly catastrophic, naturally, but a trifle tiresome nonetheless. The company’s market capitalization, at around $3.7 trillion, remains, shall we say, substantial. Its devotees, predictably, continue to adore it. One wonders if devotion alone constitutes a sound investment strategy.

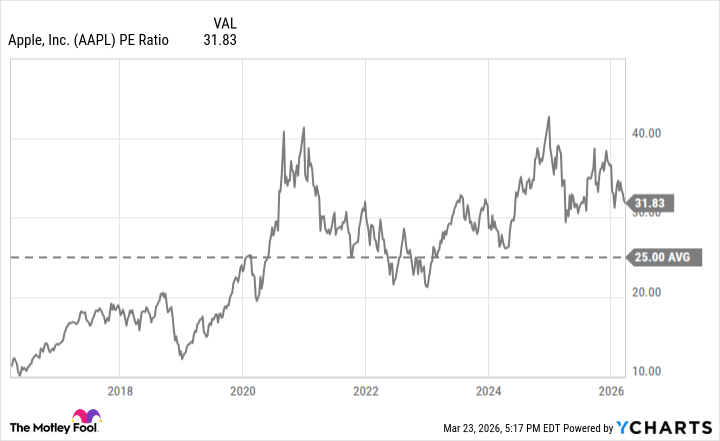

Currently, the shares are trading at thirty-two times trailing earnings. A rather extravagant price, wouldn’t you agree? Especially for a company that doesn’t routinely exhibit double-digit growth. The question, then, isn’t whether Apple is a good company—it undeniably is—but whether it’s a sensible purchase at this particular moment. One is inclined to suggest a period of observation, perhaps a discreet withdrawal to a safe distance.

A Premium Price for a Polished Apple

Apple’s valuation has been…optimistic for some time. Not merely when compared to the rather pedestrian S&P 500, which trades at a far more reasonable twenty-four times earnings, but also in relation to its own historical performance. A decade ago, one might have acquired it at a significantly less inflated multiple. One begins to suspect the market is valuing the idea of Apple, rather than the company itself.

The pandemic, of course, provided a rather convenient boost. Investors, in a fit of speculative enthusiasm, piled in. The shares have remained elevated ever since. One notes, with a degree of skepticism, the recent pronouncements regarding Apple’s artificial intelligence strategy. Siri, one gathers, is due for an upgrade. Whether this will translate into a surge in revenue remains, shall we say, open to question. One suspects a great deal of marketing bluster is involved.

A Most Unattractive Proposition, Really

Apple recently reported earnings, surprising some with a sixteen percent increase in revenue, driven by robust iPhone demand. Mr. Cook, one gathers, was rather pleased. A commendable performance, certainly, but hardly typical. Unless Apple can demonstrate a convincing path to sustained, high-growth, fuelled by something more substantial than mere consumer enthusiasm, one remains unconvinced. A pullback, one suggests, would be most welcome.

Apple is, undoubtedly, a quality business. But quality, darling, doesn’t guarantee a good return. Its inflated valuation is, frankly, a deterrent. There are, one suspects, more attractively priced growth stocks available. At its current price, one simply must pass. It’s a perfectly serviceable company, of course, but terribly, terribly overpriced. One requires a degree of prudence, you understand. And a decent return on one’s investment. It’s the least one expects.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Gold Rate Forecast

- Top 10 Coolest Things About Invincible (Mark Grayson)

- When AI Teams Cheat: Lessons from Human Collusion

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-24 16:03