Gold, that most stubbornly inert of metals, continues to fascinate. For millennia, it has served as a repository of value, a shimmering promise against the inevitable vagaries of fortune. Even now, in certain stubbornly anachronistic American states, it remains technically legal tender – a quaint notion, really, imagining a grocer accepting a sovereign in exchange for a loaf of bread. Though, one suspects, the grocer would prefer something a little less… permanent. The sheer weight of it, you understand, the metallic gravity of the transaction.

The demand, predictably, stems from those who perceive a gathering storm, a tightening of the fiscal noose. They seek refuge in its impassive gleam, a hedge against the inflationary specter and the capricious whims of political circumstance. While possessing the physical metal offers a certain tactile satisfaction, a primal reassurance, most investors opt for the convenience of exchange-traded funds – the SPDR Gold Shares ETF (GLD 2.26%) being a particularly popular specimen. A rather bloodless affair, really, owning a share in gold rather than the thing itself. A simulacrum of security, if you will.

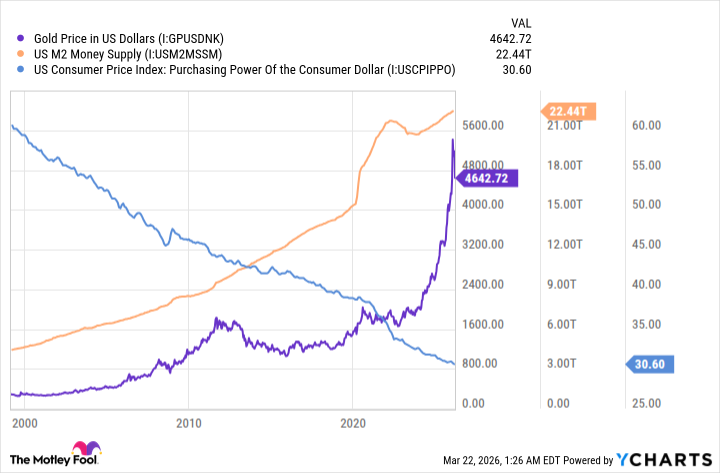

The year 2025 witnessed a rather boisterous surge in gold’s valuation – a 64% ascent, to be precise. 2026, however, has been less exuberant, a modest gain offset by a recent 19% retraction from January’s peak. Does this dip present a propitious moment for acquisition? A fleeting opportunity to gather golden crumbs? History, that relentless pedant, offers a few clues, though one should approach its pronouncements with a healthy dose of skepticism. After all, history rarely repeats itself exactly; it merely offers variations on a theme, often with a subtle, ironic twist.

The Allure of Scarcity

Gold’s enduring appeal rests, quite simply, on its limited abundance. A mere 219,890 tons have been wrested from the earth throughout human history, a paltry sum compared to the 1.7 million tons of silver or the positively astronomical quantities of coal and iron ore. This scarcity, naturally, drives its value, transforming it from a mere metal into a coveted prize. It possesses, shall we say, a certain exclusivity.

Ironically, gold is an excellent conductor of electricity, a property that would render it invaluable in the realm of semiconductors and electronic devices. However, its scarcity and attendant cost preclude its widespread adoption, leaving silver to shoulder the burden. Thus, outside the realm of jewelry – that most frivolous of pursuits – gold remains largely confined to the role of inert spectator. A glittering paperweight, if you will.

The late Warren Buffett, a man not known for his enthusiasm for precious metals, famously dismissed gold as an investment lacking intrinsic revenue or earnings. Others, such as Ray Dalio and Paul Tudor Jones, view it quite differently, recognizing its potential as a hedge against inflation and the ever-expanding money supply. A curious dichotomy, wouldn’t you agree? A testament to the subjective nature of value.

Until 1971, the United States adhered to the gold standard, a system that tethered the value of the dollar to a fixed quantity of gold. This, in theory, prevented the government from indulging in the profligacy of unchecked money printing. Since abandoning this constraint, the money supply has exploded, eroding the purchasing power of the dollar by approximately 90%. Consequently, gold’s value, measured in dollars, has soared. A rather predictable outcome, really.

The U.S. government, in fiscal year 2025, ran a deficit of $1.8 trillion, and appears poised to repeat the performance in 2026. This, predictably, has driven the national debt to a record high of $39 trillion. A rather alarming figure, wouldn’t you agree? Though, one suspects, such numbers are merely abstract concepts to those who wield the purse strings.

Paul Tudor Jones, a man with a keen understanding of market dynamics, has observed that governments often resort to “inflating away their debt” by increasing the money supply. Consequently, his hedge fund, Tudor Investment Corporation, increased its position in the SPDR Gold Shares ETF by a remarkable 49% during the final quarter of 2025. Ray Dalio, echoing this sentiment, recently recommended that investors allocate 15% of their portfolios to gold. A rather prudent suggestion, wouldn’t you say? Though, one wonders if they are merely anticipating the inevitable, rather than attempting to avert it.

A Glimmer of Hope, Tempered by Reality

Annual returns exceeding 60% are, shall we say, atypical for gold. Over the past 30 years, it has averaged a modest 8% gain, lagging behind the S&P 500 (^GSPC +1.15%), which has returned 10.7% per year. A rather sobering statistic, wouldn’t you agree? Though, one should remember that past performance is not necessarily indicative of future results. A disclaimer, of course, but a necessary one.

A rising money supply and a weakening dollar undoubtedly provide tailwinds for all hard assets, not just gold. However, stocks, unlike inert metals, generate internal revenue and earnings growth. Consequently, it is hardly surprising that the S&P consistently delivers higher returns. A rather elementary observation, really.

This, however, does not negate the value of diversification. A well-balanced portfolio, incorporating a variety of asset classes, is the key to long-term success. While stocks may deserve a larger allocation due to their superior performance, a small holding in gold can provide a degree of protection during times of economic and political uncertainty. Therefore, the recent 19% dip may present a reasonable entry point. A cautious approach, of course, but a prudent one.

As previously mentioned, the SPDR Gold Shares ETF offers a convenient way to own gold. It eliminates the need for physical storage and insurance, which can be rather expensive. It can also be bought and sold instantly through any major investing platform, unlike physical metal, which can be rather cumbersome to liquidate. A matter of convenience, really.

However, the ETF is not entirely free to own. It carries an expense ratio of 0.4%, which represents the annual fee charged to cover management costs. An investment of $50,000 would incur an annual fee of approximately $200. Still, this is likely cheaper than storing and insuring an equivalent amount of physical metal. A small price to pay for peace of mind, perhaps. Or merely a concession to the inevitable costs of financial intermediation. One can never be quite certain.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Top 10 Coolest Things About Invincible (Mark Grayson)

- When AI Teams Cheat: Lessons from Human Collusion

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Unmasking falsehoods: A New Approach to AI Truthfulness

2026-03-24 11:32