Okay, so oil‘s creeping towards a hundred bucks a barrel. Wonderful. Just what we needed. And now everyone’s acting surprised? Like we didn’t see this coming? It’s not rocket science. It’s…oil. And the Middle East. It’s always something over there, isn’t it? The whole thing is just…irritating. Look, I’m not saying I like high oil prices, I’m just saying, I’m not shocked. And frankly, the hand-wringing is excessive. So, you know, a little portfolio protection isn’t the worst idea. It’s just…responsible. I mean, you could just ignore it, but then you’re just asking for trouble. And I’ve had enough trouble, thank you very much. I’m looking at Equinor, PBF Energy, and Chevron. Not because I want to, but because…well, because it’s logical. Is that too much to ask? Just a little logic?

Equinor: Europe‘s Energy Lifeline (and a Pain in the Neck)

Twenty percent of the world’s energy goes through the Strait of Hormuz. Twenty percent! That’s a lot of tankers, a lot of potential problems, and a lot of people making decisions I wouldn’t trust to pick out a decent bagel. If that closes, Asia’s going to be scrambling, and Europe…Europe is going to be really scrambling. They’ll start bidding up prices, and then suddenly everyone’s paying more. It’s basic economics. It’s infuriating that this is even a discussion. And Norway? Norway is just sitting there, smugly pumping out natural gas. Equinor, specifically. They’re the biggest supplier to Europe. It’s not that I like Norway, it’s just…they’re positioned well. Thanks, Russia. You’ve created a whole new set of problems. And now I have to analyze energy stocks. It’s a cascade of annoyance, I tell you.

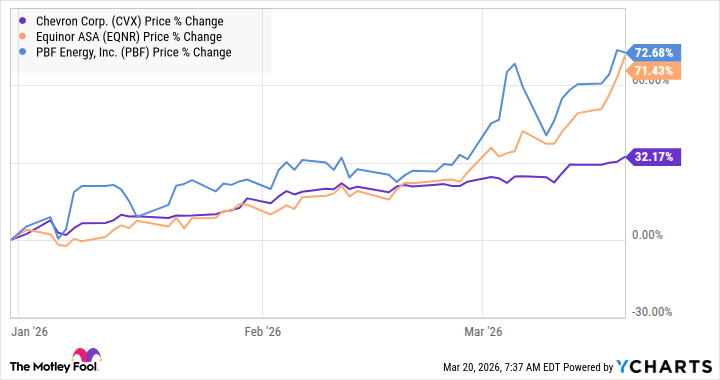

Look at this chart. After the Ukraine invasion, Norwegian energy exports to the EU just shot up. It’s…predictable. Analysts are expecting the same thing now. Earnings per share estimates for Equinor are up. It’s like they’re discovering gravity for the first time. The P/E ratio is reasonable. It’s not a steal, but it’s not outrageous. And they pay a dividend. A 3.9% dividend. It’s not going to make me rich, but it’s…something. It’s a small victory in a world filled with inconveniences.

PBF Energy and Chevron: A Necessary Evil (and a Complicated Relationship)

Okay, so these two are different. PBF is a refiner, Chevron is a producer. It’s not exactly rocket science, but people seem to need it explained. PBF makes gasoline, diesel, all that stuff. They take crude oil and turn it into things people need. But they’re exposed to higher oil prices. Unless…unless the “crack spread” is wide enough. The crack spread? It’s the difference between the price of crude and the price of refined products. It’s a ridiculously complicated term for something so basic. And right now, the crack spread is wide. It’s exploded, actually. Because refineries in the Gulf are having trouble getting crude, and there’s a shortage of refined products. It’s a mess. PBF’s stock has soared. It’s…annoying, frankly. Because everyone’s going to think they’re geniuses for buying it.

Why Chevron is the Insurance Policy (and a Reminder That Nothing is Simple)

Here’s the thing. If gas and diesel prices get too high, people will drive less. Demand will go down. And the crack spread will shrink. And PBF’s stock will fall. It’s a cycle. It’s always a cycle. So, you need Chevron. Chevron is a producer. They sell the crude oil. They benefit from higher prices, even if the crack spread closes. It’s diversification. It’s hedging your bets. It’s acknowledging that nothing is ever simple. It’s a small act of defiance against the chaos of the universe. And frankly, it’s exhausting. I just want to watch TV. Is that too much to ask?

Read More

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Top 10 Coolest Things About Invincible (Mark Grayson)

- Silver Rate Forecast

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- Gold Rate Forecast

- Palantir and Tesla: A Tale of Two Stocks

- TV Shows That Race-Bent Villains and Confused Everyone

- Unmasking falsehoods: A New Approach to AI Truthfulness

2026-03-22 14:52