Charlie Munger, a man who regarded optimism with the same suspicion a cat reserves for cucumbers, is, alas, no longer with us. His investment philosophy, however, lingers, a sort of spectral insistence on buying remarkably sound companies at prices that haven’t yet achieved escape velocity. It was, essentially, a strategy built on the deeply unsettling notion that things might actually continue to function more or less as expected. A radical idea, really. So, with the solemnity usually reserved for calculating the probability of a rogue planet colliding with a tea cosy, I’ve attempted to discern which companies would currently meet his exacting, and frankly intimidating, standards. Prepare for a list. It’s not a happy list, mind you. It’s a realistic one.

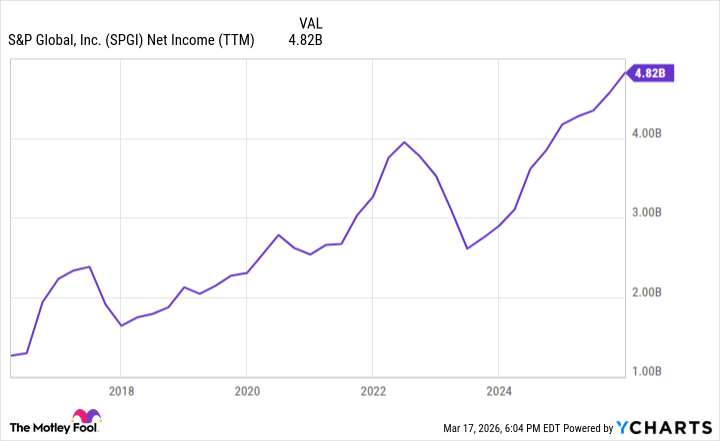

S&P Global

First, we have S&P Global (SPGI 0.33%). A name that sounds suspiciously like a moderately successful intergalactic trading consortium. Its history stretches back over 150 years, which, in the grand scheme of things, is roughly equivalent to the lifespan of a particularly well-maintained dust bunny. Munger, a man who appreciated longevity (mostly because it meant fewer things breaking down), would approve. Currently, S&P generates revenue through a variety of channels, most notably by assigning arbitrary numbers to the creditworthiness of other entities. (It’s a bit like judging the structural integrity of a sandcastle, really. Ultimately futile, but strangely compelling.) They also manage benchmark indexes, including the S&P 500, and provide detailed analytics. In short, they’ve built a moat around their business, not of water, but of prestige and the vague threat of regulatory disapproval.

The margins are, shall we say, robust. Over the last decade, they’ve averaged 65% gross and 43% operating. This isn’t growth; it’s quiet, relentless efficiency. Munger, who viewed excessive exuberance with the same skepticism he reserved for self-folding laundry, would have found this deeply satisfying. It’s the financial equivalent of a well-oiled, slightly grumpy robot, steadily accumulating wealth while ignoring the impending heat death of the universe.

The valuation, however, is… reasonable. A P/E multiple of 29 isn’t outrageous, merely… present. Shares are within 10% of their 52-week low, which, in a world obsessed with perpetual highs, is almost a radical act of contrarianism. Munger, ever the pragmatist, would likely sigh, mutter something about the inherent absurdity of market psychology, and buy a few shares. Reluctantly, of course.

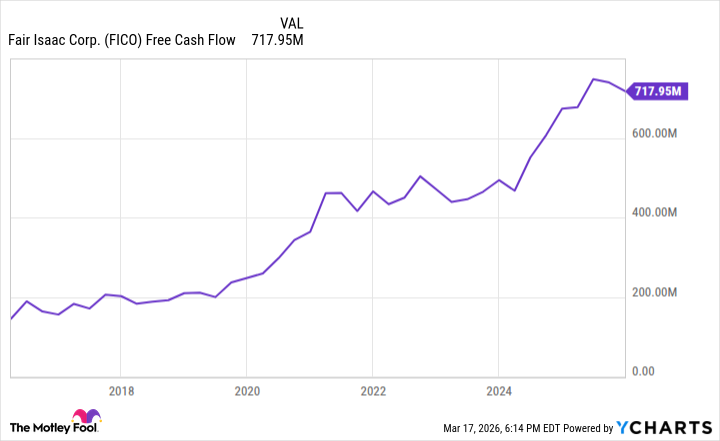

Fair Isaac

Next up is Fair Isaac (FICO +1.18%). A company that operates behind a moat so deep and wide, it’s practically a geological feature. It’s the entity behind FICO scores, those enigmatic numbers that determine whether you can afford a toaster, let alone a house. (The system is, admittedly, flawed. It often rewards those who already have money and punishes those who don’t. But logic rarely plays a role in financial systems, does it?). They earn a steady stream of income by assigning these scores and also operate a subscription-based software unit focused on fraud detection. (Preventing people from obtaining things they haven’t earned is a surprisingly lucrative business.)

The profitability is… alarming. A gross margin of 83%, up from 67% a decade ago. Free cash flow has increased by a staggering 394% over the last 10 years, now standing at $718 million. It’s the financial equivalent of discovering a money tree that inexplicably grows faster with each passing year. Munger, who distrusted anything that appeared too good to be true, would have spent weeks attempting to find the catch. (He probably would have found one, eventually.)

The leveraged buyback is a concern. Borrowing money to repurchase shares is, in Munger’s view, akin to rearranging the deck chairs on the Titanic. The P/E ratio of 44 remains above the market average. But as of March 15th, shares are trading within 6% of their 52-week low. Munger, despite his reservations, would likely conclude that the opportunity outweighs the risks. With a sigh, naturally.

Home Depot

Finally, we have Home Depot (HD 2.05%). A stalwart of the home improvement industry. Its stock has recently found itself in the cellar, trading within 4% of a 52-week low. This alone might not have attracted Munger’s attention, but the company’s long history of success and strong fundamentals certainly would. They have approximately 2,300 stores and have delivered a stable gross margin averaging around 32% for the last 25 years. They also generate over $2 billion in quarterly free cash flow.

The balance sheet is… problematic. Net debt has grown by over 250% over the last 10 years, reaching nearly $64 billion. Munger, who viewed excessive debt with the same disdain he reserved for poorly constructed arguments, would have demanded a swift and decisive reversal of this trend. (He would have likely drawn diagrams and written strongly worded memos.)

Despite this, I still believe he would jump at the chance to scoop up shares of this iconic retailer at bargain-basement prices. Those who wish to invest like Charlie Munger might consider Home Depot, Fair Isaac, and S&P Global while their stocks are on sale. Just don’t expect Munger to be particularly happy about it.

Read More

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- Palantir and Tesla: A Tale of Two Stocks

- TV Shows That Race-Bent Villains and Confused Everyone

- Unmasking falsehoods: A New Approach to AI Truthfulness

- How to rank up with Tuvalkane – Soulframe

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

2026-03-21 18:33