They call it progress. Costco, a monument to bulk bargains, now finds itself tangled in the threads of old grievances – tariffs, refunds, and the endless dance of capital. The company fought, of course, as any beast in the market does, but the echoes of those battles now reverberate, not in grand pronouncements, but in the quiet anxieties of shareholders.

A single customer, emboldened by a legal victory, now seeks recompense. A small crack in the edifice, perhaps, but cracks, as any builder knows, have a habit of widening. Costco’s stock has barely flinched, a momentary calm before the gathering storm. It’s a curious thing, this market – so quick to celebrate gains, so slow to heed warnings.

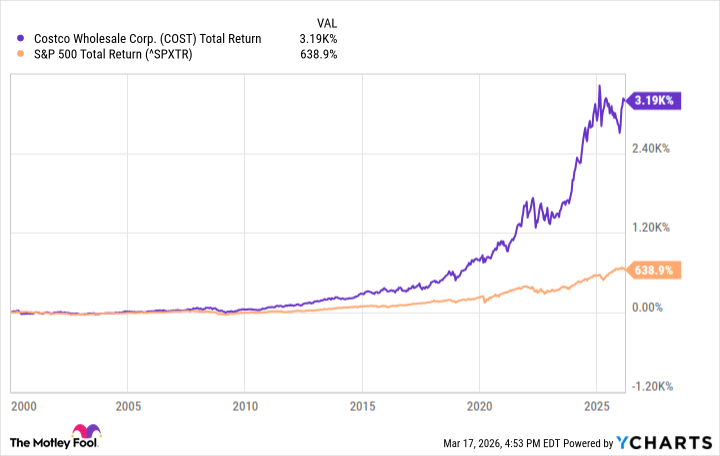

The problem isn’t a failing business, understand. Costco is a well-oiled machine, a testament to the power of volume and a shrewd understanding of the consumer’s desire for a good deal. It has weathered storms that felled lesser retailers, even expanding its reach across borders while others stumbled. Since 1985, it has consistently delivered, a steady drumbeat of profits that has lulled investors into a comfortable complacency.

The Weight of Expectation

But consistency, like any virtue, has its price. The stock is priced for perfection, a shimmering mirage built on expectations that may soon prove unsustainable. A P/E ratio of 51 – it’s a lofty perch, reminiscent of the excesses of the last bull market. The machine hums, yes, but the gears are straining.

Revenue climbed 9% to $137 billion, profit grew 13%. Impressive figures, to be sure. But strip away the polish, and you find a company operating on thin margins, reliant on relentless growth to maintain its momentum. For most, such numbers would warrant caution. Yet, Costco enjoys a peculiar immunity, a halo effect built on years of unwavering performance. Investors seem willing to overlook the fundamentals, content to bask in the reflected glory.

The tariff refunds, when they arrive, will be a temporary balm, but they will also expose a deeper vulnerability. The market will see them not as a windfall, but as a correction, a reminder that even the most successful companies are subject to the whims of fate and the machinations of policy.

This isn’t a prediction of ruin, mind you. Costco will likely continue to grow, to adapt, to prosper. But the days of effortless expansion are over. The company is entering a new era, one defined by heightened scrutiny, increased competition, and a growing awareness of its own limitations. The illusion of invincibility is fading.

A Moment for Prudence

For those considering adding to their Costco holdings, a pause is warranted. The stock is not cheap, and the near-term outlook is clouded by uncertainty. There are other opportunities, other companies with more compelling valuations and greater potential for growth.

Costco remains a formidable force, a testament to the power of the consumer and the ingenuity of its management. But even the strongest empires eventually face reckoning. This isn’t a call to abandon ship, but a plea for prudence, a reminder that even the most successful companies are not immune to the laws of gravity.

The market rewards those who see beyond the headlines, who understand the underlying forces at play. In this case, the message is clear: Costco is a good company, but it is not a bargain. And in the world of investing, price is everything.

Read More

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- Unmasking falsehoods: A New Approach to AI Truthfulness

- TV Shows That Race-Bent Villains and Confused Everyone

- Palantir and Tesla: A Tale of Two Stocks

- How to rank up with Tuvalkane – Soulframe

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-03-21 11:22