![]()

The market, as always, breathes with a restless uncertainty. It is a landscape sculpted by anxieties – geopolitical whispers, the shifting sands of monetary policy, the ever-present specter of inflation. Prices, like leaves in an autumn gale, are tossed about by every headline, every rumor. Since the first of February, the broader indices have yielded ground – the S&P 500, a modest decline; the Nasdaq Composite, a slightly more pronounced retreat. And amongst those feeling the chill most keenly are the technology companies, those once-bright stars of the “Magnificent Seven,” now dimmed by a cautious gaze.

Yet, within every decline lies a possibility, a quiet invitation. The discerning investor, one who understands the long rhythm of things, recognizes these moments not as causes for panic, but as opportunities to acquire enduring value at a more reasonable price. Let us consider, then, three companies – Nvidia, Amazon, and Meta – each a significant player in the unfolding drama of artificial intelligence, and each, in its own way, offering a compelling case for consideration.

Nvidia: The Architect of a New Realm

Nvidia, perhaps, is the most visible architect of this new realm. What began as a purveyor of graphics for the ephemeral pleasures of gaming has evolved into something far more substantial – the very foundation upon which the applications of generative AI are built. It is a curious transformation, to see a company once associated with entertainment now at the heart of a technological revolution.

The demand for Nvidia’s Hopper, Blackwell, and forthcoming Rubin architectures remains relentless, fueled by the insatiable appetites of the major hyperscalers – Microsoft, Amazon, Alphabet, Meta, Oracle, and even OpenAI. With an estimated 92% share of the AI data center GPU market, Nvidia commands a pricing power that borders on the regal. It is a position of considerable strength, though one that invites scrutiny and, inevitably, competition.

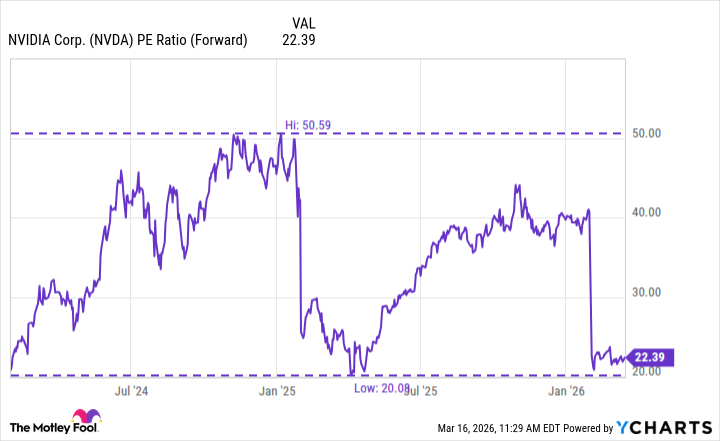

The company’s recent financial performance reflects this dominance. Data center revenue surged 75% year-over-year, while gross margins expanded and earnings per share climbed nearly 100%. These are not merely numbers; they are testaments to a company successfully navigating a complex and rapidly evolving landscape. Yet, the market, in its fickle wisdom, has seemed unimpressed. The stock has languished, a victim, perhaps, of its own success and the inevitable anxieties of those who fear what comes next.

There are whispers of risk, of course. Concerns about sales in China, the rise of competitors like Advanced Micro Devices and Broadcom, the fear that Nvidia is a one-trick pony. These are valid points, worthy of consideration. But they strike me as short-sighted. During the recent earnings call, management offered robust guidance, seemingly unperturbed by the geopolitical winds. Moreover, Nvidia is diversifying, investing in enterprise software, telecommunications, and other infrastructure opportunities – laying the groundwork for a future beyond the data center.

With a forward price-to-earnings multiple near its lowest point throughout this AI surge, and a strong market position bolstered by enduring tailwinds, Nvidia appears to me a bargain – a solid foundation upon which to build a portfolio.

Amazon: A Giant Stirring from Slumber

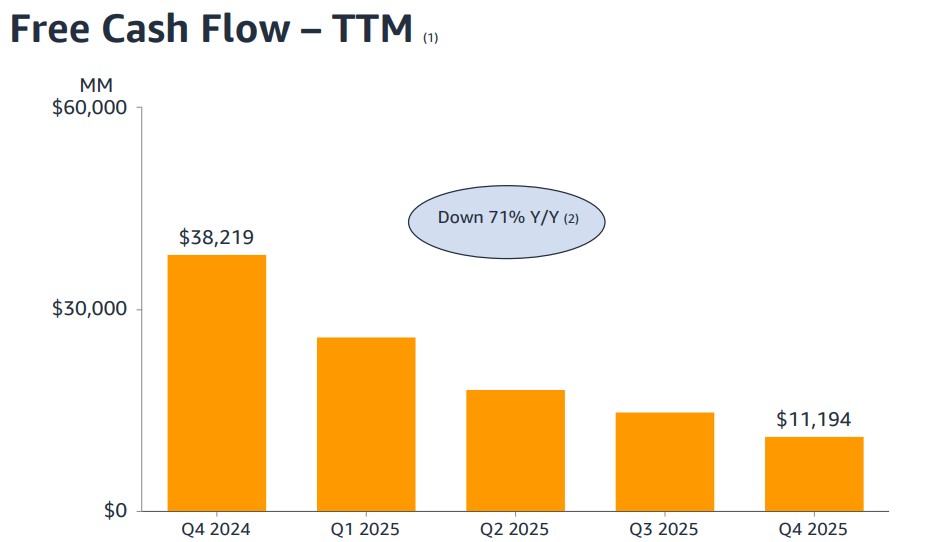

Amazon, in contrast, presents a more peculiar case. Despite strong financial results for the fourth quarter and the entirety of 2025, the stock has retreated, wiping out nearly $400 million in shareholder value. It is a reminder that even the most formidable of companies are subject to the whims of the market.

The primary driver of this decline is Amazon’s ambitious capital expenditure plan. While Wall Street anticipated a substantial investment, the company’s announced budget – a staggering $200 billion – exceeded expectations. It is a bold move, a testament to Amazon’s long-term vision. But it also raises concerns about near-term profitability.

Building data centers, procuring chips, designing custom silicon – these things take time and capital. And, as Amazon’s trailing-12-month free cash flow has demonstrated, the impact on profitability can be significant. Yet, I believe the degree of panic is overblown. The recent strength of Amazon Web Services – which accounts for the majority of the company’s operating profit – suggests that the investment is likely to pay off.

Amazon’s partnership with Anthropic is particularly noteworthy. As the AI startup becomes further integrated into the AWS ecosystem, Amazon appears to be building a vertically integrated model – one that combines its own chips, efficient robotics, and blossoming cloud infrastructure. It is a long-term play, but one that I believe is likely to succeed.

With a P/E ratio hovering around 29, Amazon stock is trading near its cheapest valuation in a year. It is an opportune moment to acquire shares in a company laying the foundation for its next chapter of AI-driven growth.

Meta Platforms: The Illusion of Transformation

Meta Platforms, perhaps, is the most misunderstood of the three. The company generates the majority of its revenue and profit through advertising on its social media platforms – Facebook, Instagram, and WhatsApp. It is a business that, for years, has been viewed as mature, even stagnant.

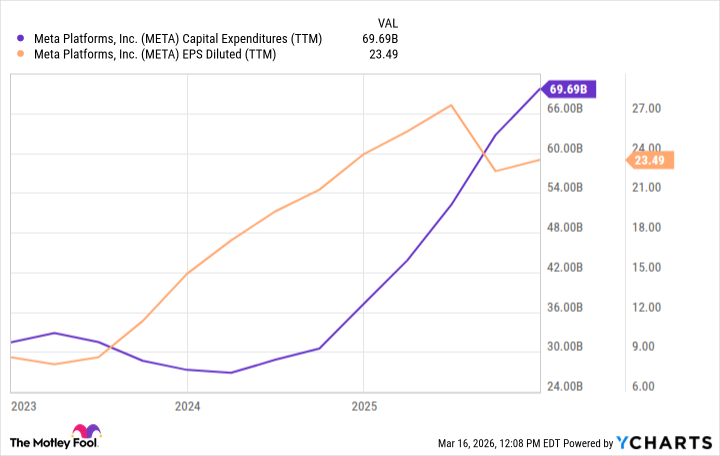

However, Meta’s investments in AI have begun to change that narrative. Its new suite of machine learning advertising tools, dubbed Advantage+, has grown into a $60 billion annual revenue run-rate business. It is a remarkable achievement, a testament to the company’s ability to adapt and innovate.

In my view, investors do not fully appreciate the accretive power of AI within Meta’s ecosystem. Despite rising spending, the company’s earnings power has nearly tripled throughout this AI revolution. It is a clear indication that Advantage+ is becoming a dominant force in the world of advertising, cementing Meta’s position as a market leader.

Despite its robust profitability and booming AI services business, Meta remains the cheapest of the Magnificent Seven stocks, with a forward P/E of just 21. It is a steal, in my opinion, and a compelling opportunity for long-term investors.

The market, like life itself, is a complex and often unpredictable landscape. But within that complexity, there are always opportunities for those who are willing to look beyond the surface and see the underlying value. These three companies – Nvidia, Amazon, and Meta – each offer a compelling case for consideration, and each, in its own way, is poised to benefit from the ongoing revolution in artificial intelligence.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- Palantir and Tesla: A Tale of Two Stocks

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- How to rank up with Tuvalkane – Soulframe

2026-03-20 17:32