Now, I’ve seen a good many bubbles rise and burst in my time – land schemes in Missouri, railway fever, even a spell of tulip mania out in Albany. And this here business with quantum computing, and particularly this IonQ company, strikes me as a bit like watching a feller try to build a house of cards in a hurricane. Wall Street, bless their optimistic hearts, is all a-twitter about it, proclaimin’ IonQ the next big thing. They’re predictin’ prices that’d make a Mississippi gambler blush. But I reckon a closer look reveals a story less about scientific breakthrough and more about a slick bit of financial legerdemain.

Shares have been climbin’ faster than a greased pig, outpacin’ even the S&P 500 and that speedy Nasdaq Composite. Analysts, those oracles of the market, are crowin’ about a price target of $65 a share – more than double what it’s fetchin’ now. But I’ve learned a thing or two about followin’ the herd, and it generally leads to a cliff.

The Illusion of Explosive Growth

They’re boastin’ about 202% revenue growth last year – a number that sounds mighty impressive until you poke at it a bit. They’re projectin’ more of the same for 2026. Seems IonQ has partnered with all the big cloud fellers – Microsoft, Amazon, Google – and even got a nod from Nvidia. Folks are thinkin’ this is a recipe for AI-fueled riches. But here’s where the story gets a bit tangled.

It seems IonQ has been on a spendin’ spree, acquirin’ companies left and right. They’ve shelled out over $4 billion in the last couple of years. Now, I ain’t against a bit of smart investment, but a good portion of their revenue – and that flashy growth they’re toutin’ – is comin’ from these purchased assets. And so far, they haven’t managed to squeeze much profit out of ’em, not nearly enough to justify the price tag. It’s like buyin’ a prize bull and discoverin’ he can’t pull a plow.

A Cash Burn and a Growing Debt

Now, a company can grow fast and still be in trouble if it’s burnin’ money like a bonfire. And IonQ, bless its ambitious heart, is doin’ just that. Last year they posted losses of over half a billion dollars, and their cash flow was plumb negative. They’re nowhere near turnin’ a profit. It’s akin to diggin’ a well with a leaky bucket.

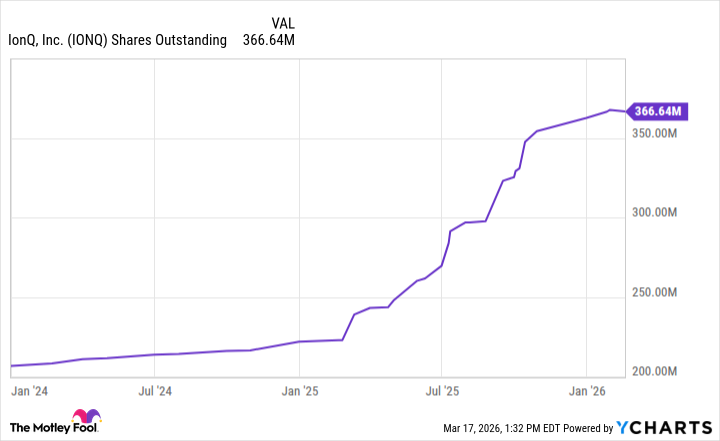

With a burn rate like that, their $2.4 billion in liquidity ain’t gonna last long. It raises a question, doesn’t it? How are they fundin’ all this growth? Well, it seems they’ve been printin’ shares faster than a newspaper press. Their outstanding share count has nearly doubled since 2024, with significant issuations happenin’ right as the stock price was climbin’.

They’ve taken advantage of their risin’ valuation to issue stock, raise money, and pad their balance sheet. Then, they used that capital to fund acquisitions, which they marketed as game-changin’ growth catalysts, further fuelin’ the hype. It’s a clever trick, I’ll grant you, but it ain’t buildin’ a solid foundation.

A Prediction: A Fall from Grace

Issuin’ stock to fund growth and dilutin’ shareholders ain’t a sustainable strategy. It’s a house of cards waitin’ for a breeze. I reckon it’s only a matter of time before investors catch on to IonQ’s playbook and start movin’ their money toward more durable opportunities. It reminds me of the dot-com bubble, where companies were valued on nothin’ but promises and hot air.

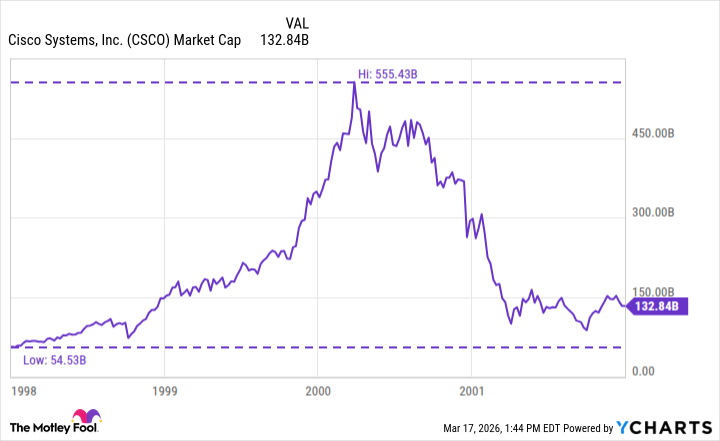

IonQ trades more like a meme stock than a sound investment. They’re promotin’ a narrative that echoes those once common among the dot-com darlings. I predict that IonQ stock will crater in a similar fashion to Cisco in the early 2000s.

By year’s end, I reckon it’s more likely that IonQ will be tradin’ below $10 than it is to double and hit Wall Street’s lofty target. Mark my words. It’s a lesson, folks: sometimes the shiniest apples are the most rotten at the core.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- Palantir and Tesla: A Tale of Two Stocks

- How to rank up with Tuvalkane – Soulframe

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

2026-03-20 15:14