The market had a case of the jitters, shedding AI stocks like a gambler losing a bad hand. Valuations got ahead of themselves, and the cash burn rate looked like a bonfire. Investors got spooked. Predictable. But fear, as always, creates opportunity. A few names were tossed aside, left nursing bruises in the corner. I took a look. Two of them caught my eye.

SentinelOne: The Quiet Watchman

SentinelOne. The name sounded like a government agency. Which, in a way, it is. A digital one. The stock chart looked like a dropped staircase. A rough 2022, followed by a lot of sideways shuffling. Plenty of competition – CrowdStrike, Palo Alto Networks – all the usual suspects. They cast long shadows, but shadows can hide things. And SentinelOne had a few secrets of its own.

This wasn’t a company built on AI; it was built with it, from the ground up. It didn’t react to threats; it anticipated them. Detected them on the device itself, before they could even whisper to the cloud. Offline operation, system reverts with a single click… it was elegant. Efficient. The kind of tech that doesn’t shout, but works.

Revenue hit a billion in fiscal 2026, up 22%. Another 20% projected for 2027. Not bad for a company everyone seemed to have written off. And they were generating free cash flow – 52 million – meaning they weren’t begging for handouts. They weren’t profitable yet, but they weren’t bleeding to death either.

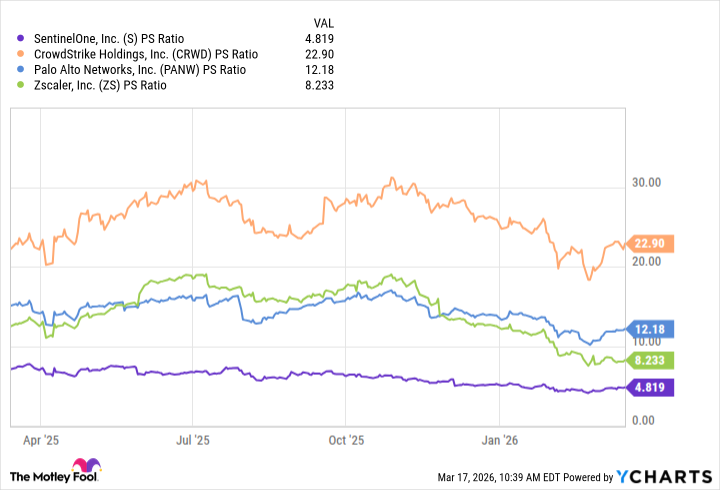

The price-to-sales ratio sat at a modest 5. CrowdStrike, Palo Alto, Zscaler… they were all trading at a premium. SentinelOne wasn’t flashy, but it was undervalued. As of this writing, you could pick up 99 shares for around $1,450. A double from here wouldn’t be a miracle. It would be smart money finding its level.

Adobe: The Old Guard Still Has Teeth

Adobe. A name you thought you knew. The first half of the 2020s felt like a lost decade. A sell-off in 2022, a brief rally, another dip in 2024. Competition was heating up, and the whispers about AI disruption were getting louder. The CEO stepped down, leaving a vacuum. The usual story. But stories can be deceiving.

Investors seemed fixated on the uncertainty, ignoring the fundamentals. Revenue for the first quarter of fiscal 2026 was $6.4 billion, up 12%. Growth was steady, consistent. The spike in income tax expenses was a temporary blip. The company was still printing money.

The 9% revenue growth forecast for 2027 wasn’t earth-shattering, but it was solid. And the relentless selling had driven the P/E ratio down to 15, the forward P/E to 11. Arguably too low for a company of this caliber. You could snag six shares for around $1,550. A double wouldn’t require a revolution. Just a return to sanity. A little bit of faith in a company that had earned it.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Palantir and Tesla: A Tale of Two Stocks

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- How to rank up with Tuvalkane – Soulframe

- TV Shows That Race-Bent Villains and Confused Everyone

2026-03-20 11:02