![]()

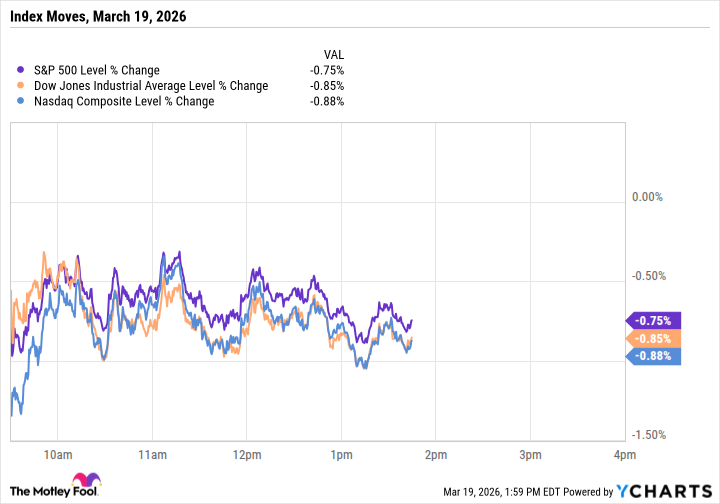

The indices, those meticulously calibrated instruments of collective anxiety, registered a decline on Wednesday. The Dow Jones Industrial Average yielded 0.85%, a fractional surrender, while the Nasdaq Composite and S&P 500 conceded 0.77% and 0.68% respectively. These are not collapses, not yet, merely adjustments – the market exhaling, perhaps, before the next, inevitable constriction. The proximate cause, as always, is assigned a name: the situation in Iran, and its predictable consequence, a fluctuation in the price of crude oil. The oil, it seems, is not merely a commodity, but a symptom.

The price rose, briefly, to $119 per barrel, a number possessing no inherent meaning, yet demanding attention. It then retreated to $115, a gesture of temporary compliance. The Strait of Hormuz, that narrow passage through which a significant portion of the world’s oil is funneled, remains the focal point. Any disruption there, any minor impediment to the flow, is amplified, reified, and presented as a threat. The market does not predict; it internalizes the possibility of disruption, and prices it accordingly. It is a self-fulfilling prophecy, elegantly disguised as analysis.

The constituent parts of these indices, the individual companies, barely registered the tremor. Their movements were minimal, almost imperceptible, as if shielded by some bureaucratic inertia. This is not stability, of course, but a peculiar form of suspension, a waiting period before the next, inevitable reassessment.

On the Dow, Caterpillar experienced the most significant decline, falling 1.9%. A predictable reaction, given its sensitivity to energy costs and the general malaise of global economic sentiment. It is as if the company is merely a barometer, reflecting the prevailing atmospheric pressure. Its performance is not a result of innovation or strategy, but a passive response to external forces.

On both the Nasdaq and S&P 500, Nvidia led the losses, declining 1.3%. A substantial sum, in absolute terms, yet insignificant when considered against its overall valuation. The company, a behemoth of the digital age, carries a weight that distorts the very indices it inhabits. A 1.3% decline is a rounding error, a statistical anomaly. Yet, it is reported, analyzed, and presented as news. The illusion of significance is maintained.

The market’s response, on this particular day, was not panicked, merely cautious. Investors trimmed positions, a ritualistic gesture of self-preservation. They waited for further instructions, for the next set of directives from an unseen authority. The waiting, of course, is the most significant part.

The Bigger Picture

The measured response suggests a lack of conviction, a hesitancy to fully embrace the narrative of impending crisis. Oil at $115 is uncomfortable, certainly, but not catastrophic. The true danger lies in a sustained move above $120, a threshold that would trigger a cascade of inflationary pressures. Some analysts predict a price of $200 or more, should the supply from the Middle East be curtailed. These predictions are presented as objective assessments, yet they are based on assumptions, on projections, on the inherent uncertainty of the future.

Evidence of this anxiety is already appearing in other corners of the market. Mortgage rates have climbed, a subtle signal that bond investors are factoring in the possibility of persistent inflation. The flow of capital is a complex, opaque system, driven by forces that are rarely fully understood. Higher energy costs will inevitably work their way through the economy, first at the pump, then in transportation costs, and finally in the prices of goods and services. It is a slow, inexorable process, like the erosion of a coastline.

Construction materials and industrial inputs are also increasing in price, potentially weighing on sectors like homebuilding and manufacturing. Companies with thin margins or heavy fuel exposure will feel the squeeze first. It is a Darwinian process, a weeding out of the less adaptable. The strong will survive, but even they will be changed by the experience.

However, the lack of dramatic moves among the largest index components is noteworthy. When markets are truly frightened, there is a broad-based sell-off, a indiscriminate panic. This did not happen today. The mega-cap tech stocks that dominate these indices drifted lower, without any sign of capitulation. Investors are cautious, but they are not yet heading for the exits. The waiting continues.

The Long View

For long-term investors, days like this are merely noise, insignificant fluctuations in a larger, incomprehensible system. The underlying fundamentals of the companies that comprise these indices have not changed because of a temporary spike in oil prices. Crude oil is up 66% since the recent conflict began, yet the indices have fallen by less than 7%. This is not resilience, but a peculiar form of detachment, a willingness to ignore the obvious.

Nvidia is still selling every GPU it can manufacture. Caterpillar still benefits from infrastructure spending. The investment thesis for most quality companies does not hinge on whether crude oil is $110 or $119 on any given Thursday. The market is not driven by logic, but by sentiment, by fear, and by the relentless pursuit of illusory gains.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Gold Rate Forecast

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Palantir and Tesla: A Tale of Two Stocks

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- How to rank up with Tuvalkane – Soulframe

- TV Shows That Race-Bent Villains and Confused Everyone

2026-03-19 21:37