Nvidia, a company presently favored by many, has experienced a period of stagnation. For the past six months, its share price has remained largely unchanged – an unusual circumstance for a concern so frequently touted as a harbinger of future growth. This is not to suggest a decline, merely a pause, and it is in such pauses that a sober assessment becomes necessary.

The company continues to expand, and its dominance in the field of graphical processing units is undeniable. This is not a matter of mere marketing; the quality of their products is, by most accounts, superior. But the question is not whether Nvidia is a successful company, but whether its current valuation reflects a realistic appraisal of its future prospects.

The Acceleration of Growth

Nvidia manufactures, amongst other things, the processing units that power the current wave of artificial intelligence. Their ecosystem, a term favored by those with a vested interest, is indeed comprehensive. Companies are willing to pay a premium, not because of any inherent loyalty, but because alternatives are, as yet, less capable. This is a temporary advantage, and it is a dangerous habit to mistake a lead for invincibility.

The introduction of the Rubin GPU is presented as a significant advancement, promising a tenfold reduction in inference costs. While such improvements are welcome, they are incremental. The claim that fewer Rubin GPUs will be required for training is, on the surface, paradoxical. It suggests a greater efficiency, but also a potential reduction in hardware sales. The company anticipates continued demand, and rightly so, but it is crucial to distinguish between genuine progress and skillful accounting.

The new technology will not be offered at a discount, which is predictable. A company must, after all, maintain its profit margins. But the assumption that this will automatically translate into sustained growth is a leap of faith. The market is not governed by wishful thinking, but by the cold logic of supply and demand.

The hyperscalers – the large data centers that drive much of the demand for AI – are projected to spend a considerable sum on infrastructure. The figures quoted – $650 billion, potentially rising to $3 to $4 trillion by 2030 – are substantial, but they are also projections. Such forecasts are, by their very nature, uncertain. To base an investment strategy solely on such speculative numbers is to invite disappointment.

The possibility of renewed sales to Chinese companies is also presented as a positive catalyst. The lifting of export restrictions would undoubtedly provide a boost to Nvidia’s revenue. But to rely on geopolitical shifts as a cornerstone of one’s investment thesis is to embrace an unnecessary level of risk.

Despite the absence of sales to China, Nvidia’s revenue grew by 73% in the first quarter of fiscal year 2026. This is a respectable figure, and the company anticipates further growth of 77% in the next quarter. But such rates of expansion are unsustainable in the long term. The laws of economics are immutable.

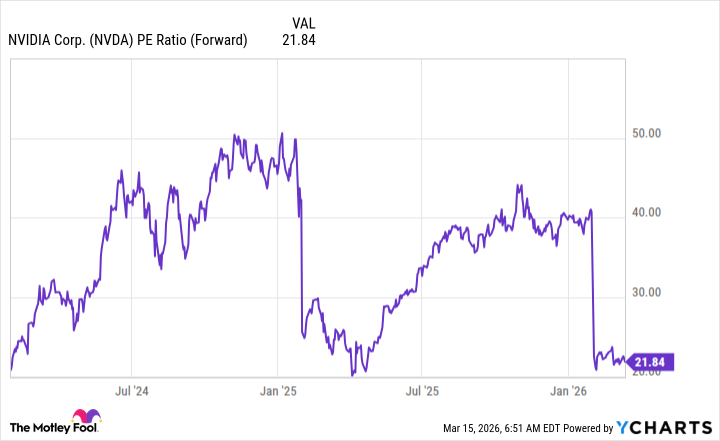

A Question of Price

Despite these ostensibly positive indicators, Nvidia’s stock currently trades at a price-to-earnings ratio of 21.8. The S&P 500, by comparison, trades at 21.2. This suggests that the market expects Nvidia’s growth to slow. The prevailing narrative is that the company will enjoy one more year of rapid expansion before reverting to the mean.

This assessment is not unreasonable. The AI buildout will undoubtedly continue for several years, and Nvidia is well-positioned to benefit. But the market is rarely swayed by logic. It is driven by sentiment, by fear, and by greed. To ignore these forces is to court disaster.

The prevailing pessimism surrounding Nvidia’s stock may be justified. The company is not immune to the cyclical nature of the technology industry. To assume that it will continue to defy gravity indefinitely is a dangerous delusion. The time to exercise caution is now, before the inevitable correction occurs.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Brent Oil Forecast

- Persona 5: The Phantom X Relativity’s Labyrinth – All coin locations and puzzle solutions

- ‘Super Mario Galaxy’ Trailer Launches: Chris Pratt, Jack Black, Anya Taylor-Joy, Charlie Day Return for 2026 Sequel

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

2026-03-19 08:03