Let’s be brutally honest. Most of these “dividend stock” articles read like actuarial tables disguised as financial advice. A numbing parade of payout ratios and yield percentages. It’s enough to send a sane man reaching for the nearest bottle of something STRONG. But I’ve been digging, sifting through the financial wreckage, and I’ve stumbled onto something… interesting. Something that smells faintly of oil, ambition, and a surprisingly stable future. We’re talking about Enbridge.

The Canadian pipeline behemoth. A name that doesn’t exactly set the pulse racing, I grant you. But beneath the bland corporate exterior lurks a cash-generating machine. They’re moving black gold, people. Moving it efficiently. And in this increasingly chaotic world, efficiency is a damn near revolutionary concept. Forget the hype about renewable energy for a minute – we’re STILL going to need oil. And Enbridge is positioned to deliver.

The Illusion of Control

They keep talking about “guidance.” Financial “guidance.” As if a company can simply guide itself to success. It’s a delusion. But Enbridge, remarkably, has managed to meet or exceed this self-imposed fiction for TWENTY consecutive years. Twenty years! That’s… unsettling. It suggests a level of control in a world spiraling out of it. They’re practically defying the laws of entropy.

The adjusted earnings rose 9% last year to 6.6 billion Canadian dollars. Numbers. Just numbers. But behind those numbers is a network of pipelines, a logistical marvel, pumping resources across North America. And that, my friends, is REAL.

Now, the payout ratio. Over 100%. The financial scribes will clutch their pearls. “Unsustainable!” they’ll shriek. But they’re looking at the wrong metrics. Enbridge doesn’t play by those rules. They evaluate based on distributable cash flow (DCF). And that, thankfully, rose 4% last year. As long as that keeps flowing, the dividend is safe. Solid. A beacon in the gathering storm.

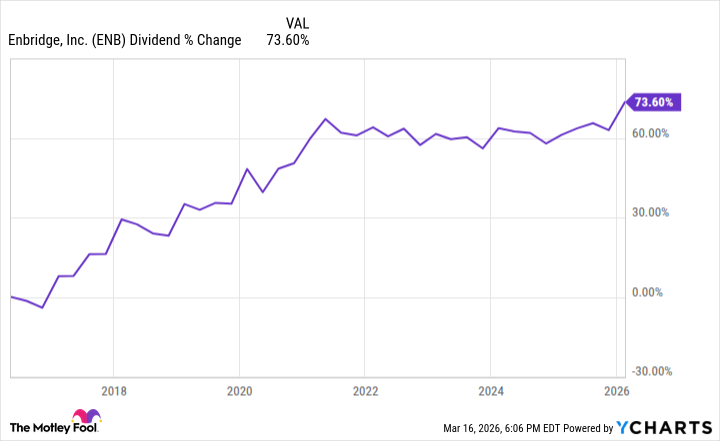

Thirty-One Years of Defiance

Thirty-one consecutive years of increasing payouts. Let that sink in. Thirty-one years of resisting the forces of economic gravity. It’s… suspicious. Almost TOO good. But I’m willing to take the risk. Because in this rigged game, you need to find the players who are willing to defy the odds.

Currently, the yield is 5.3%. More than four times the pathetic S&P 500 average of 1.2%. It’s a glaring discrepancy. A screaming opportunity. Over the past five years, the stock has risen 49%. Including the dividend? Around 105%. It’s not going to make you a billionaire overnight, but it’s a damn sight better than watching your savings evaporate.

Look, I’m not saying Enbridge is a magic bullet. The world is a chaotic, unpredictable mess. But in this climate of uncertainty, finding a company that consistently delivers cash is a rare and valuable thing. So, do your own research. Dig deeper. And if you’re feeling particularly reckless, consider adding a little Enbridge to your portfolio. Just don’t say I didn’t warn you.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- 20 Best TV Shows Featuring All-White Casts You Should See

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Palantir and Tesla: A Tale of Two Stocks

- The Best Directors of 2025

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- Gold Rate Forecast

- How to rank up with Tuvalkane – Soulframe

2026-03-17 19:03