They speak of hesitation in the markets, a skittishness around these…tech-dreams. Even concerning Nvidia, this maker of silicon and promises. A company that has, in recent years, grown fat on the hunger for artificial minds. The stock, it drifts around $185, a shadow of the $212 peak it briefly touched back in October. A small fall, perhaps, for those counting fortunes, but a tremor for those who build their hopes on such shifting ground.

There’s a weariness settling over this grand tech-rush. Investors, they squint at the spending, at the mountains of coin thrown after this AI phantom. They wonder if it will bear fruit, or simply rot in the digital fields. But Nvidia…Nvidia is different. It’s not merely participating in this fever; it’s stoking the flames. And a business that can do that, even in lean times, deserves a closer look.

The Machine Keeps Turning

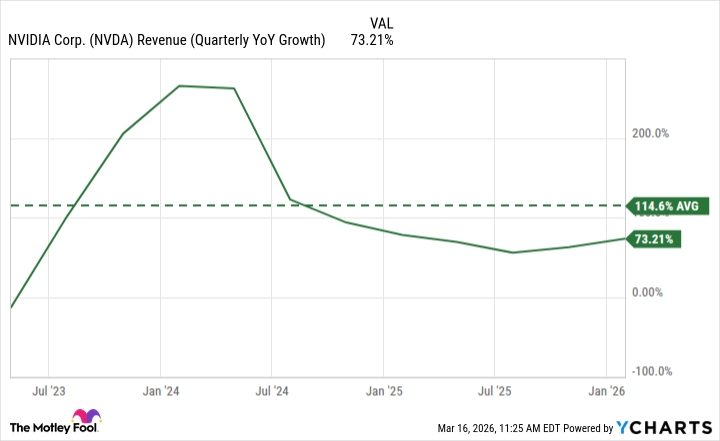

The reluctance to buy, it isn’t, I suspect, a judgment on Nvidia itself. The company still breathes fire. Averaged over the last three years, it’s grown at a rate that would make a Tsarist bureaucrat blush—nearly 115% per quarter. Even the most recent figures, dipped to 73%, still speak of a relentless engine. Such growth is a rare beast, especially when even the giants—the ‘hyperscalers’—are starting to forge their own tools, attempting to break free from dependence. It speaks to the essential nature of Nvidia’s work, to the fundamental need for these chips in the creation of these new, artificial intelligences.

This isn’t about whims or fashion. It’s about the gears turning, the machines demanding fuel. And Nvidia, for now, is a significant supplier. That is a position of power, and one that will not be easily surrendered.

The Price of Progress

Four and a half trillion. A figure that feels…excessive. The most valuable company in the world. A monument to ambition. Yet, when you consider the earnings, the sheer volume of wealth flowing through this enterprise, the price doesn’t seem so outrageous. Analysts whisper of a forward price-to-earnings multiple of 22, only slightly above the average of the S&P 500. A premium, yes, but perhaps a justifiable one. Nvidia isn’t merely a stock; it’s a reflection of a future we are building, whether we want it or not.

The stock hasn’t soared this year, true. But for those who measure time in decades, not quarters, there’s a case to be made. A leader in this chip-making game, a business that may continue to grow, even at a reduced pace. Even a slowdown to 50% would still leave this company in a strong position. The machine demands its fuel, and Nvidia is positioned to provide it.

There will be turbulence, of course. Market anxieties, industry shifts. But a long view reveals a different picture. Nvidia isn’t a gamble; it’s an investment in the relentless march of progress. And that, in the end, is a force that few can ignore.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- 20 Best TV Shows Featuring All-White Casts You Should See

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- Palantir and Tesla: A Tale of Two Stocks

- The Best Directors of 2025

- Gold Rate Forecast

- How to rank up with Tuvalkane – Soulframe

2026-03-17 17:03