Tesla (TSLA +1.16%) has, in recent periods, captured considerable investor attention. The company’s ambitions extend beyond automotive production, with a stated focus on artificial intelligence and robotics. While these ventures represent potential long-term avenues for value creation, a sober assessment of current financial performance and prevailing valuation multiples is warranted.

Recent market conditions have exerted downward pressure on growth equities. The S&P 500 has experienced moderate declines year-to-date, and Tesla’s share price has contracted approximately 20% from its 52-week high. This correction invites scrutiny as to whether the current price adequately reflects the inherent risks.

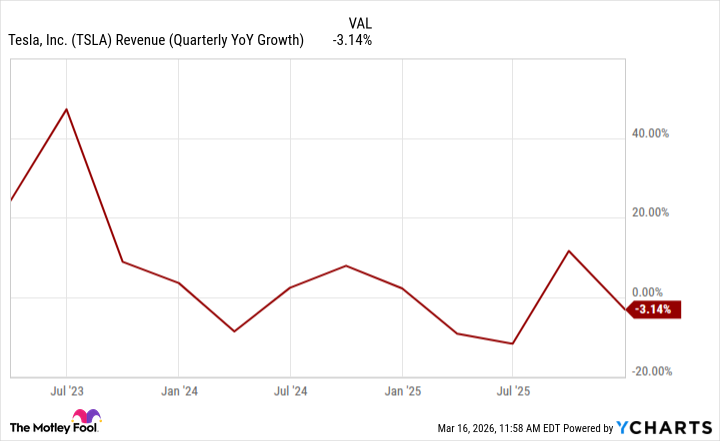

Financial Performance: Emerging Headwinds

While future projections regarding robotic technologies and autonomous driving are frequently cited, near-term financial data presents a less optimistic picture. The rate of revenue growth has demonstrably decelerated, and increased competition within the electric vehicle sector represents a tangible impediment to sustained expansion. A reliance on future, as yet unrealized, revenue streams introduces a significant degree of uncertainty.

Recent quarterly results indicate a pronounced contraction in net income. Third-quarter 2025 earnings totaled $840 million, a 61% year-over-year decline. This contraction necessitates a cautious approach to projections of future profitability.

Valuation: A Premium Difficult to Justify

Despite recent price corrections, Tesla’s valuation remains exceptionally high. The price-to-earnings multiple currently exceeds 350. Such a premium is predicated on expectations of extraordinary future growth, and a failure to meet these expectations could trigger a substantial correction.

Sustaining a high valuation requires consistent demonstration of robust growth and expanding profitability. In the absence of these factors, maintaining a premium multiple becomes increasingly untenable. Investors are advised to consider the potential downside risks associated with a richly valued equity.

The current juncture warrants a measured approach. While Tesla’s long-term potential remains a subject of debate, the confluence of decelerating growth, increased competition, and an elevated valuation suggests limited near-term upside. Prudent investors may find more compelling opportunities elsewhere.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- 20 Best TV Shows Featuring All-White Casts You Should See

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- The Best Directors of 2025

- Palantir and Tesla: A Tale of Two Stocks

- Gold Rate Forecast

- How to rank up with Tuvalkane – Soulframe

2026-03-17 02:02