Okay, look. The market’s been throwing tantrums again, and Microsoft – Microsoft, for Christ’s sake – is down a quarter from its peak. A quarter! Like some penny stock vaporizing in the desert heat. They call it a “correction.” I call it a goddamn opportunity. A chance to load up on a company that’s not just riding the AI wave, it’s building the goddamn surfboard. I’ve been staring at the charts, fueled by lukewarm coffee and a growing sense of… well, urgency. This isn’t some polite dip for the faint of heart. It’s a primal scream, and I intend to answer.

Back in late ’22, early ’23, everyone was bracing for the apocalypse, convinced the whole thing was going to collapse. The usual suspects screaming about recession, doom, and the inevitable heat death of the universe. Microsoft took a hit then, too. But they didn’t flinch. They didn’t panic. They kept building. And they’re doing it again now. The air is thick with fear, but the fundamentals… the fundamentals are solid. TOO solid. It’s almost suspicious.

This isn’t about waiting for a “bounce back.” This is about recognizing that Microsoft is positioning itself as the central nervous system of the AI revolution. Forget the hype, forget the breathless pronouncements from Silicon Valley. Microsoft is quietly, efficiently, ruthlessly establishing dominance. By the end of 2026? This thing could be roaring. A new high is not just possible; it’s practically inevitable. I’m telling you, it’s a goddamn steal right now.

Microsoft: The AI Switzerland

Don’t get me wrong, I don’t need a 25% gain to reach a new all-time high. It’s closer to 33%, which, frankly, is insulting. It’s practically begging to be bought. The brilliance here isn’t about Microsoft trying to be the AI, it’s about Microsoft becoming the AI’s playground. They’re not building their own generative model to compete with OpenAI, xAI, Anthropic—they’re hosting them ALL. Think of it as a neutral ground, a digital Switzerland where all the AI factions can coexist… and pay Microsoft a hefty rental fee.

They’re letting the algorithms duke it out, while they collect the spoils. It’s a stroke of genius, a masterclass in strategic positioning. And it’s all flowing through Azure, their cloud computing platform. That thing’s been on fire for a decade, but the AI build-out is throwing gasoline on the flames. The last quarter? A 39% jump in revenue. THIRTY-NINE PERCENT. They could have done even better if they hadn’t been hoarding computing power for internal use. The backlog? $625 BILLION. That’s not a backlog, that’s a goddamn mountain of future revenue.

Microsoft’s Q2 revenue rose 17% year-over-year, blowing expectations out of the water. It’s a clean sweep. No asterisks, no caveats. All that AI spending? It’s paying off. Handsomely. It’s as close to a no-brainer as you’re going to get in this insane market. This isn’t speculation, it’s observation. It’s watching a predator circle its prey.

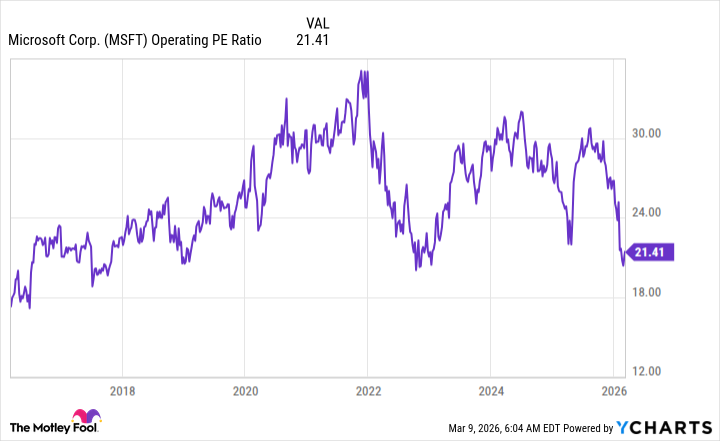

Valuation: A Premium Worth Paying

Okay, so Microsoft isn’t exactly cheap. It trades at a premium valuation – 25.6 times trailing earnings, 24.5 times forward earnings. Higher than the S&P 500. Surprise, surprise. Microsoft has always traded at a premium. They’ve earned it. But look closer. The operating price-to-earnings ratio is near decade lows. You have to go back to 2019 to find a better entry point. This isn’t just a buying opportunity; it’s a goddamn steal.

The stock will rally. It has to rally. It’s a matter of time. And when it does, the returns will be… substantial. This isn’t about chasing hype; it’s about recognizing value. It’s about understanding that Microsoft isn’t just a tech company anymore. It’s the infrastructure of the future. And right now, you can get a piece of it at a discount. Don’t hesitate. Don’t overthink it. Just buy. Before the rest of the vultures descend.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- The Best Directors of 2025

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- 20 Best TV Shows Featuring All-White Casts You Should See

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- Gold Rate Forecast

- Umamusume: Gold Ship build guide

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

2026-03-16 09:22