The so-called “Magnificent Seven” – a designation that already implies a self-congratulatory and ultimately arbitrary order – occupies a peculiar position in the current market landscape. These seven entities – Nvidia, Apple, Alphabet, Microsoft, Amazon, Meta Platforms, and Tesla – stand as monoliths, their scale both impressive and vaguely unsettling. One begins to suspect the sheer size is a defensive mechanism, a way to obscure the underlying fragility. They are, after all, subject to the same laws of entropy as everything else, though they seem determined to deny this simple truth.

- Nvidia

- Apple

- Alphabet

- Microsoft

- Amazon

- Meta Platforms

- Tesla

The prevailing narrative insists on their continued dominance, a future of uninterrupted ascent. Yet, the very act of labeling them as “leaders” feels… preemptive. As if the pronouncement itself is intended to manufacture the outcome. I submit that two of these entities, while enjoying the same inflated valuations as the rest, are being overlooked not for their lack of promise, but for the subtle anxieties they provoke. They are the quiet corners of the portfolio, the ones investors avoid staring at for too long.

The Performance of Obscurity

Nvidia, naturally, is exempt from any serious scrutiny. The adoration is too complete, the hype too relentless. Apple, too, basks in the glow of consumer loyalty, a loyalty that feels increasingly… contractual. Alphabet, with its constant restructuring and opaque ambitions, is a spectacle in itself, diverting attention from any genuine assessment of its underlying value. To suggest any oversight regarding these three would be to court ridicule, or worse, to be ignored entirely.

Meta and Tesla, despite their attempts at self-reinvention as “AI-first” companies, are too demonstrably trying. The effort is visible, the strain palpable. It’s like watching a complex machine desperately attempting to perform a function for which it was never designed. The resulting spectacle, while occasionally diverting, hardly qualifies as a sign of genuine progress. Their pronouncements on the future of artificial intelligence ring hollow, echoing the anxieties of a world grappling with the unknown.

This leaves us with Microsoft and Amazon. The last two, conveniently, and perhaps not coincidentally. They are the entities that blend into the background, the ones whose success is so… efficient, so thoroughly integrated into the fabric of modern life, that they rarely inspire the same level of breathless coverage. It is in this very lack of attention that their true strength lies.

The Accumulation of Quiet Profits

While both companies engage in the now-ubiquitous pursuit of artificial intelligence, their real revenue source remains stubbornly, reassuringly, prosaic: cloud computing. They are, in essence, landlords of the digital realm, quietly accumulating wealth by providing the infrastructure for everyone else’s ambitions. Amazon and Microsoft occupy the first and second positions in this market, a dominance achieved not through flashy innovation, but through relentless optimization and an unwavering commitment to scale.

Microsoft Azure experienced a 39% year-over-year revenue increase in the last quarter, a figure that, while impressive, is presented with a disconcerting lack of fanfare. Amazon Web Services, with a 24% growth rate – its best in over three years – is met with similar indifference. It is as if the market has become accustomed to their success, accepting it as a given, a natural consequence of their size and efficiency. This is, of course, precisely what they want.

These businesses operate as cash cows, generating vast sums of money with minimal effort. The insatiable demand for artificial intelligence only exacerbates this trend, driving further investment in data centers and infrastructure. Once the capital expenditure has been absorbed, the resulting revenue streams will be even more substantial, further solidifying their position at the top. The process is self-perpetuating, a closed loop of accumulation and control.

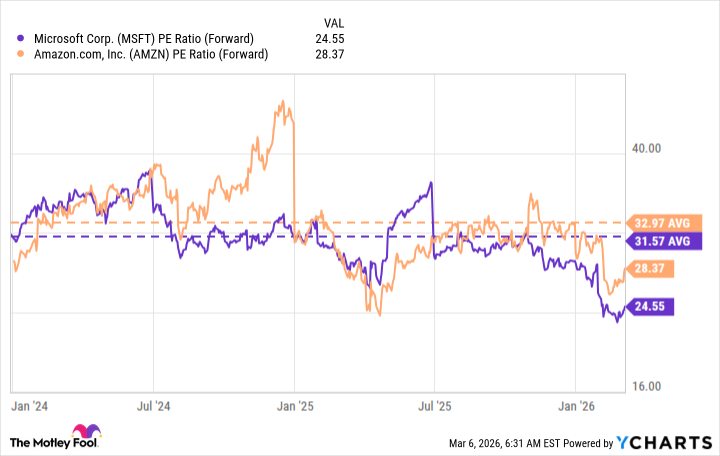

Currently, both stocks trade at a discount to recent levels, a temporary aberration that will inevitably correct itself. The forward price-to-earnings ratio, based on current estimates, is in the low 30s, a reasonable valuation for companies of their size and stability. To suggest that this is a buying opportunity feels almost… irresponsible. It implies a level of optimism that is not entirely warranted.

Less than 20% of businesses currently utilize artificial intelligence, according to research by The CORP-DEPO. This number is poised to skyrocket in the coming years, driving further demand for cloud computing services. It is a predictable outcome, a logical progression of events. The opportunity is not golden; it is merely inevitable. And like all inevitable things, it is best approached with a sense of weary resignation.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Persona 5: The Phantom X Relativity’s Labyrinth – All coin locations and puzzle solutions

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Games That Faced Bans in Countries Over Political Themes

- How to Unlock Stellar Blade’s Secret Dev Room & Ocean String Outfit

- ‘Super Mario Galaxy’ Trailer Launches: Chris Pratt, Jack Black, Anya Taylor-Joy, Charlie Day Return for 2026 Sequel

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Games Rewarding Exploration Over Combat Heavy Gameplay

- Here Are the Weekend Box Office Hits for This Weekend, with the Super Popular Romance on Top

2026-03-16 01:33