Right now, there are eleven companies that can legitimately claim to be worth a rather startling amount of money – a trillion units of whatever currency happens to be fashionable this season. But only four have ascended to the truly rarefied air of the three-trillion club: Nvidia, currently boasting a market capitalization that would make several small kingdoms envious1, Apple, Alphabet, and Microsoft. It’s a bit like the exclusive club where everyone has a dragon, but some dragons are just… shinier.

Now, we at the firm have been giving rather a lot of thought to Broadcom. And the conclusion, after much calculating and staring intently at charts (a surprisingly effective method, if you ignore the headaches), is that it’s poised to join this select group. Broadcom, you see, doesn’t make dragons. It makes the things for the dragons. The bits that make them breathe fire more efficiently, the scales that don’t fall off quite so readily. Essential stuff, really.

Currently valued at a respectable, but not quite intimidating, $1.6 trillion, a purchase of Broadcom stock today offers the potential for a 91% return should it reach the three-trillion mark. We believe this isn’t a matter of ‘if’, but ‘when’. The question isn’t whether Broadcom will join the club, but what colour tablecloth they’ll be using for the induction ceremony.

AI: More Than Just Clever Toasters

The current obsession with Artificial Intelligence – or, as our analysts like to call it, ‘making toasters that think they’re people’ – has led to an unprecedented demand for data centres. These aren’t glamorous places, mind you. Mostly just very large, very cold rooms filled with humming machines. But they are, undeniably, the engines of the modern age. And Broadcom supplies a great many of the gears and cogs that keep those engines running. They don’t just make semiconductors, they also provide the networking components and accessories – the plumbing, if you will – that keep the whole system from collapsing into a heap of silicon and regret.

The real secret sauce, however, is their Application-Specific Integrated Circuits – or ASICs. These are chips specifically designed to do one thing, and do it well. Think of it like hiring a specialist rather than expecting your general practitioner to perform brain surgery. They’re becoming increasingly popular as cloud and data centre operators realize that they can get more bang for their buck – or, more accurately, more processing power for their gold coins – than with the standard-issue Graphics Processing Units. Google, for instance, relies on Broadcom to create the cores of its Tensor Processing Units – the brains of its particularly clever toasters. And they’re even building custom AI accelerators for Meta Platforms, which, let’s be honest, is probably just so they can show more cat videos, faster.

The Numbers Don’t Lie (Much)

Broadcom’s recent financial results are… encouraging. In their fiscal 2026 first quarter, they generated a record revenue of $19.3 billion – a 29% increase year-over-year. Earnings per share jumped 28% to $2.05. It’s all very impressive, although we suspect a small gnome is secretly polishing the numbers with a magic cloth. Management believes this growth will continue to accelerate, and they’re projecting revenue of $22 billion for the second quarter – a nearly 47% increase. This will fuel adjusted EBITDA of $15 billion – up 50%. It’s a bit like watching a particularly enthusiastic dragon hoard gold, only with more spreadsheets.

The Path to Three Trillion: A Rough Calculation

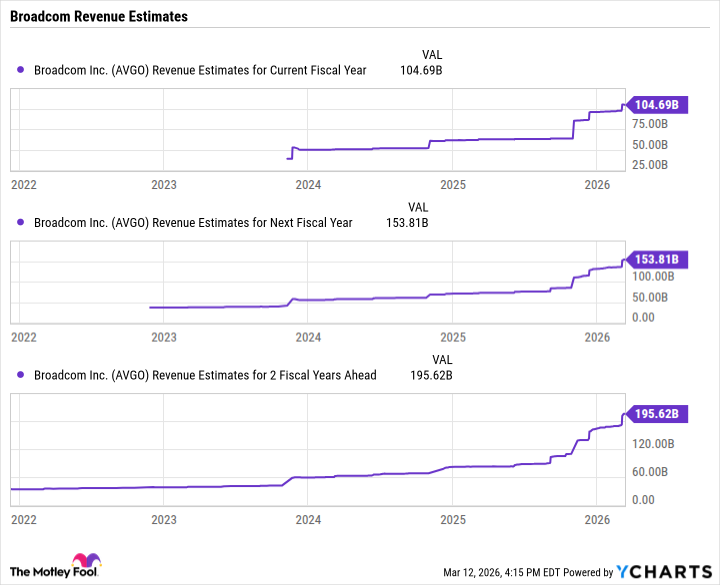

Wall Street currently expects Broadcom to generate revenue of nearly $105 billion in fiscal 2026, giving the stock a forward price-to-sales ratio of 15. Assuming this ratio remains constant – a big assumption, mind you, as the market is notoriously fickle – the company will need to generate revenue of $200 billion to support a $3 trillion market cap.

As the chart illustrates, Wall Street predicts Broadcom’s revenue will grow to $196 billion by 2028, putting it within striking distance of the $200 billion target. However, Broadcom has a habit of exceeding expectations and raising its guidance, so it’s likely to reach that benchmark even sooner. The data centre boom is expected to continue, with global capital expenditures reaching roughly $7 trillion by 2030. As a leading supplier of data centre components, Broadcom is well-positioned to benefit from this trend. Moreover, ASICs are increasingly seen as a viable, less expensive alternative to GPUs, further increasing Broadcom’s opportunity.

Despite the stock’s impressive rise, Broadcom still trades at 30 times forward earnings. Using the price/earnings-to-growth ratio yields a multiple of 0.44, which, according to our analysts, means the stock is undervalued. It’s a bit like finding a perfectly good dragon scale for a single copper coin.

Given the available evidence, we believe Broadcom stock is a buy – before it joins the $3 trillion club. It’s not a guaranteed success, of course. Nothing is. But in a world filled with uncertainty, a little bit of calculated risk can be a very good thing.

1 The Guild of Alchemists and Venture Capitalists, a notoriously secretive organization, maintains that the true value of Nvidia is measured in ‘units of pure imagination’. This metric is, unsurprisingly, difficult to verify.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- Spotting the Loops in Autonomous Systems

- The Best Directors of 2025

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- 20 Best TV Shows Featuring All-White Casts You Should See

- Umamusume: Gold Ship build guide

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Uncovering Hidden Signals in Finance with AI

- Gold Rate Forecast

2026-03-15 10:03