CoreWeave, a name whispered now amongst the cognoscenti of the digital bazaar, has become, in these frantic months, something of a phenomenon. A purveyor of computational space, a renter of silicon souls – they deal in the very stuff of artificial intelligence, and the revenue, naturally, has been… spirited. One might even say it’s grown with a velocity that would make a provincial governor blush.

The stock, a volatile beast, has indeed performed a curious dance. A surge, a peak, then a… settling. Like a samovar cooling after a particularly lively evening. Concerns, naturally, have arisen. One cannot simply conjure capacity from thin air, you understand. And the markets, those fickle judges, are ever watchful. Let us, then, consider the matter with a trader’s eye, and perhaps a touch of… observation.

The Bull’s Curious Case

CoreWeave offers, in essence, a shortcut. A bypass of the usual bureaucratic delays and the maddening scarcity of those coveted Nvidia processors. They rent access, by the hour, to these silicon engines. A most convenient arrangement, for those who lack the patience – or the inclination – to build their own computational estates. It’s like hiring a particularly swift troika for a journey, rather than breeding the horses oneself.

The growth, as they say, has been… substantial. Triple-digit gains, faster revenue accumulation than any other cloud provider – a claim that, naturally, requires a pinch of salt, but a pinch nonetheless. They’ve become, it seems, the first to receive the latest Nvidia offerings – Blackwell and its even more extravagant cousin, Blackwell Ultra. A privilege, certainly, but one that comes with a price. One always pays for precedence, you see.

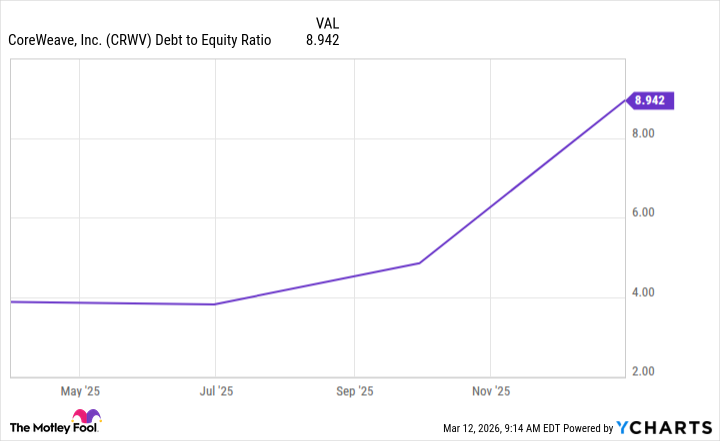

The Bear’s Lamentable Predicament

To maintain this feverish pace, this relentless expansion, requires investment. And investment, alas, necessitates… debt. A growing mountain of obligations, a precarious balancing act. CoreWeave, it appears, relies heavily on borrowed funds. A most unsettling prospect, for a company built on the shifting sands of technological innovation. One can almost see the ledgers trembling with anxiety.

The markets, ever sensitive to the slightest tremor, worry that a slowdown in the demand for artificial intelligence might leave CoreWeave… exposed. A most reasonable concern, given the volatile nature of these digital enthusiasms. And the increasing debt, naturally, complicates matters. It’s like adding weights to a dancer’s ankles – it hinders their ability to leap.

Should One Venture a Stake?

A purchase? The question hangs in the air, heavy with uncertainty. For the cautious investor, I would advise restraint. Observe, yes, but do not rush in. Let the company demonstrate a path to genuine profitability before committing your funds. Patience, after all, is a virtue, especially in the realm of speculative finance.

For the more… adventurous soul, however, the bull case holds a certain appeal. Demand remains strong, other cloud providers echo this sentiment, and the potential for growth is undeniable. It’s like betting on a spirited horse in a particularly unpredictable race. There is risk, certainly, but also the possibility of a substantial reward.

Therefore, if you are not averse to a degree of risk, if you possess a certain… tolerance for chaos, now might be a propitious time to acquire shares of CoreWeave. It could prove to be a most fortunate gamble, a shrewd investment in the next stage of this digital… spectacle.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Persona 5: The Phantom X Relativity’s Labyrinth – All coin locations and puzzle solutions

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- How to Unlock Stellar Blade’s Secret Dev Room & Ocean String Outfit

- Brent Oil Forecast

- ‘Super Mario Galaxy’ Trailer Launches: Chris Pratt, Jack Black, Anya Taylor-Joy, Charlie Day Return for 2026 Sequel

2026-03-14 19:25