![]()

The chronicles of commerce reveal few instances as stark as the recent trajectory of Micron Technology. Over the past year, its shares have ascended by a prodigious 318%, a figure that, in the relentless calculus of the market, dwarfs the gains achieved by those heralded as pioneers in the realm of artificial intelligence – Nvidia, Palantir, and Broadcom among them. This is not merely a tale of financial increment; it is a symptom, a visible manifestation of deeper currents reshaping the landscape of technological dependency.

To attribute this surge solely to market forces would be a simplification, a convenient obscuring of the underlying reality. Micron’s fortunes have been inextricably linked to the escalating demand for memory – DRAM and NAND – driven by the insatiable appetite of the burgeoning AI data centers. These structures, vast and impersonal, consume memory at a rate previously unimaginable, creating a constriction in supply and, consequently, a distortion in pricing. It is a familiar pattern: scarcity, artificially induced or otherwise, begetting profit. The question that now hangs over the enterprise is whether this momentum can be sustained, or if it is merely a fleeting bloom on the vine of technological speculation.

Let us examine the matter with a dispassionate eye, tracing the contours of the memory market and assessing the prospects for continued ascent. The reports emanating from UBS suggest a further intensification of the favorable pricing environment. A projected 62% increase in DRAM prices in the first quarter of 2026, coupled with a 40% jump in NAND flash, paints a picture of escalating costs. While such projections are subject to the inherent uncertainties of forecasting, they offer a glimpse into the pressures building within the supply chain.

Micron’s reliance on DRAM – accounting for nearly 80% of its revenue – renders it particularly vulnerable, and yet, simultaneously, uniquely positioned to benefit from these trends. The remaining portion, derived from NAND flash, provides a degree of diversification, but the true engine of growth resides in the volatile realm of dynamic memory. The anticipated persistence of the DRAM chip shortage – for another 12 to 18 months, by some accounts – suggests a prolonged period of constrained supply. Even NAND chips, typically more readily available, are expected to remain in tight supply until mid-year. This scarcity, born of the relentless demand for AI processing, is not merely a market fluctuation; it is a systemic pressure, a testament to the scale of the technological undertaking.

The memory manufacturers, predictably, are exploiting this constriction. Samsung, a behemoth in the industry, has reportedly increased DRAM prices by a staggering 100%, following a substantial 70% increase in January. To expect Micron to follow suit would be not merely reasonable, but inevitable. It is the immutable law of the market: opportunity seized, profit maximized. The true cost, of course, is borne by those downstream – the consumers, the businesses, the institutions – who must absorb these escalating expenses.

The root of this undersupply lies, in part, in the very nature of advanced memory technology. High-bandwidth memory (HBM), critical for AI applications, consumes three times the semiconductor wafer capacity of standard memory chips. This disparity, a consequence of increasing technological complexity, creates a bottleneck in production. As HBM finds its way into graphics cards, specialized ASICs, and even server processors, the demand intensifies, exacerbating the scarcity. The market is, in essence, being stretched to its limits.

Micron itself forecasts that the HBM market will nearly triple between 2025 and 2028, reaching $100 billion within a few years. This projection, if realized, would solidify Micron’s position as a key player in the AI ecosystem. But it also raises a troubling question: can the industry sustainably meet this demand, or are we destined for a cycle of shortages, price increases, and constrained innovation?

Is Further Ascent Foreseeable?

The semiconductor stock has already logged impressive gains of 36% in 2026. It currently trades at a premium – almost 38 times earnings – relative to the Nasdaq-100 index’s multiple of 32. This premium, however, may be justified, given the anticipated surge in earnings – a projected 322% increase this year, followed by further gains next year. The market, it seems, is willing to pay a higher price for growth.

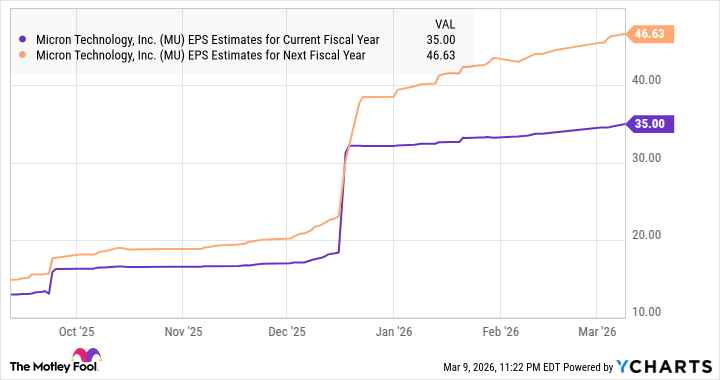

The chart above reveals a consistent upward revision of Micron’s earnings estimates, a trend that could continue given the factors discussed. Should Micron indeed achieve $46.63 per share in earnings next fiscal year, its stock price could conceivably reach $1,189, assuming a forward earnings multiple of 25.5 – in line with the Nasdaq-100 index. That is nearly triple the current price, suggesting that this ascent, however precarious, may not yet be complete. The chronicle of Micron Technology, therefore, continues – a testament to the relentless forces shaping the modern technological landscape.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- The Best Directors of 2025

- Spotting the Loops in Autonomous Systems

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- 20 Best TV Shows Featuring All-White Casts You Should See

- Umamusume: Gold Ship build guide

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Uncovering Hidden Signals in Finance with AI

- Gold Rate Forecast

- TV Shows That Race-Bent Villains and Confused Everyone

2026-03-14 17:42