The current agitation in the Levant, predictably, has stirred the oil markets. One observes, with a certain detached amusement, the renewed interest in companies previously relegated to the bargain basement of portfolio diversification. It seems investors, in their perpetual search for novelty, occasionally remember the elemental necessity of fuel. Devon Energy and Diamondback Energy, two entities engaged in the extraction of this essential, yet increasingly problematic, commodity, appear, for the moment, to offer a modicum of value. A cynical observer might suggest this is merely a temporary reprieve, a fleeting moment of respectability before the inevitable return to obscurity. Nevertheless, a closer inspection reveals a degree of competence, or at least, a determined effort to avoid complete ruin.

Value in a Volatile World

Oil, having commenced the year at a comparatively modest $57 per barrel, has now ascended to the vicinity of $88. Predicting the trajectory of this black fluid, particularly in light of geopolitical instability, is an exercise in futility. One might as well consult the entrails of a particularly unfortunate fowl. However, hedging against sustained high prices, particularly when the underlying assets remain reasonably priced even in a downturn, is not entirely unreasonable. These companies, it seems, have at least attempted to prepare for a future where oil might not consistently trade at levels conducive to extravagant displays of wealth.

The advantage, naturally, lies in domestic production, thereby mitigating, to some extent, exposure to the more volatile regions. The true test, however, remains the corporate break-even price – that critical threshold below which even the most skillfully managed enterprise descends into the abyss. These entities, at least, claim to have addressed this rather fundamental concern.

Diamondback: Prudence in the Permian

Diamondback Energy, with its focus on the Permian Basin, appears to have adopted a strategy of disciplined restraint. No reckless acquisitions, no extravagant vanity projects. Instead, a methodical approach to capital allocation, coupled with incremental improvements in operational efficiency. The result, predictably, is a modest, but sustainable, dividend – currently yielding 2.2%. They also engage in hedging, a practice as old as commerce itself, to protect against the inevitable vicissitudes of the market. It is, if not inspired, at least sensible.

Devon: Synergy and the Delaware

Devon Energy, meanwhile, is poised to merge with Coterra Energy, a transaction that promises, as all such transactions do, “significant synergy opportunities.” The combined entity will control a substantial acreage in the Delaware Basin, with a break-even price of less than $40 per barrel. One suspects the accountants will be the primary beneficiaries of this arrangement, but the underlying economics, at least on paper, appear sound. The majority of their inventory, they claim, can be profitably exploited even at levels below $50. A bold assertion, perhaps, but one that warrants consideration.

A Modest Proposal

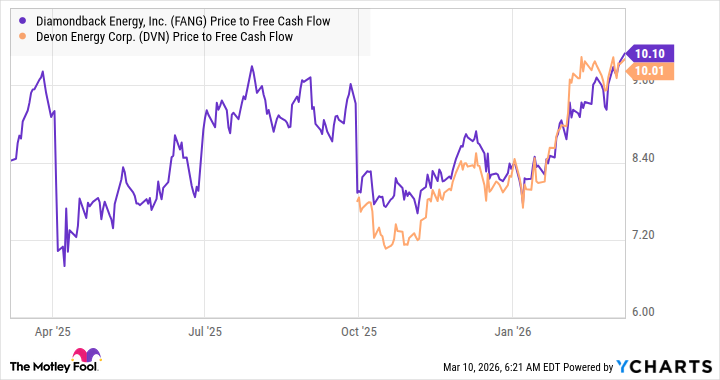

Both stocks currently trade on relatively low price-to-free cash flow multiples. This, coupled with their comparatively low break-even prices and the potential for sustained high oil prices, makes them, if not compelling investments, at least reasonably attractive ones. One should not expect miracles, of course. These are, after all, oil companies. But in a world increasingly defined by uncertainty and excess, a degree of prudence is, for the moment, a virtue.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- The Best Directors of 2025

- Spotting the Loops in Autonomous Systems

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- 20 Best TV Shows Featuring All-White Casts You Should See

- Umamusume: Gold Ship build guide

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Uncovering Hidden Signals in Finance with AI

- Gold Rate Forecast

- TV Shows That Race-Bent Villains and Confused Everyone

2026-03-14 16:02