The pronouncements of Wall Street analysts, those oracles of fleeting sentiment, are often little more than echoes of the prevailing wind. They offer price targets, projections of future value, yet these figures are rarely born of deep contemplation, but rather a hurried assessment of current currents. To blindly follow such pronouncements is folly; a gambler’s dance with chance. However, to ignore them entirely is to disregard a symptom, however unreliable, of the larger fever that grips the markets. It is in the discrepancies, the spaces between expectation and reality, that a discerning eye might find opportunity.

And so it is with Nvidia, a company whose very name now seems to embody the relentless march of technological progress. The current price, a mere $178 per share at this writing, belies the expectations held by those who study its fortunes. An average price target of $265 suggests a potential ascent of nearly fifty percent within a year – a considerable gain, yet one that seems almost… understated, given the forces at play. That Nvidia, the largest company measured by market capitalization, should present such an opportunity is a paradox worthy of note. It is not merely a question of financial gain, but of observing the unfolding of a new era.

The Illusion of Limits

One often hears the lament that growth, like all earthly things, must eventually slow. The larger a concern becomes, the more difficult it is to maintain a rapid pace of expansion. This is a truth readily apparent to any student of history. A small seed may sprout with vigor, but the towering oak requires far more sustenance to add a single branch. Yet Nvidia defies this seemingly immutable law. It is as if the demand for artificial intelligence, for the very engines of computation, is insatiable – a hunger that no amount of silicon can fully appease.

The hyperscalers, those vast data centers that house the digital world, are willing to pay any price for the processors that power their ambitions. Alternatives exist, of course, but Nvidia holds advantages – a legacy of innovation, a network of expertise, and a certain… understanding of the needs of its clients. This affords them a pricing power that few companies enjoy, a power that is not merely economic, but psychological. It is a power born of trust, and trust, as any seasoned investor knows, is a most valuable commodity.

The announcements of record-setting capital expenditures by these hyperscalers for 2026 are not mere projections; they are commitments. And these commitments, like the foundations of a great cathedral, will take years to fully realize. The computing units are the final stones to be laid, the last touches of artistry applied. Thus, Nvidia’s growth is not a fleeting phenomenon, but a sustained undertaking, a long-term investment in the future. Indeed, projections suggest that global capital expenditures on data centers will reach a staggering $3 to $4 trillion by 2030 – a figure that dwarfs the ambitions of empires past. McKinsey & Company, in their own assessment, estimate a cumulative spending of $7 trillion. Such sums are not merely numbers; they are a testament to the transformative power of technology.

We are, as yet, in the nascent stages of this infrastructure buildout. To believe that Nvidia’s growth will suddenly cease, to assume that it will revert to the average performance of other large-cap companies, is to misunderstand the nature of the forces at play. The market, in its shortsightedness, often fails to grasp the long-term implications of technological advancements. It is in these moments of misjudgment that opportunity presents itself.

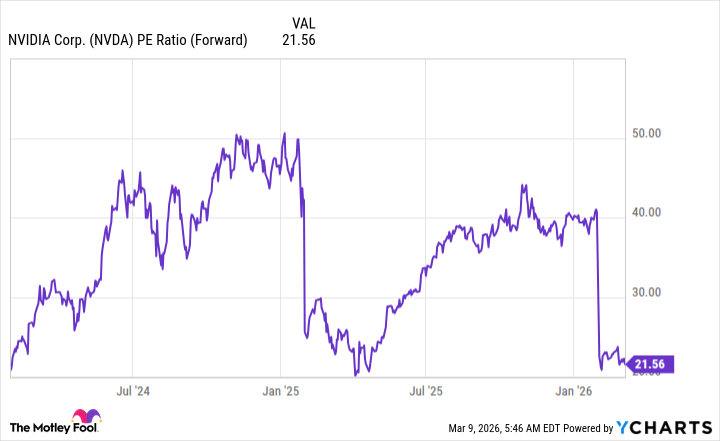

The Illusion of Valuation

Currently, Nvidia trades at a forward earnings multiple of 21.6 – a figure that, upon closer inspection, appears remarkably modest. To understand why, one must consider the context. The S&P 500, a broad measure of the American economy, trades at a similar multiple of 21.7. Thus, Nvidia is not merely keeping pace with the market; it is slightly undervalued. Of course, these figures are based on projected earnings, and projections are, by their very nature, speculative. But the implication is clear: the market is assuming that Nvidia will have a strong year in 2026, and then… revert to the mean. A most improbable outcome, given the circumstances.

The hyperscalers’ plans, Nvidia’s own projections, and independent analyses all suggest that growth will continue far beyond 2026. The market, blinded by its own short-term focus, fails to see the long-term potential. It is a folly akin to a man who sells his inheritance for a loaf of bread. To recognize this misjudgment, to capitalize on this shortsightedness, is the mark of a discerning investor.

Based on Wall Street’s price targets, Nvidia possesses more one-year upside potential than most large tech companies. Therefore, a prudent investor should consider adding to their position, or initiating a new one. AI spending shows no signs of slowing, and Nvidia remains at the forefront of this technological revolution. To buy now is not merely a financial decision; it is an affirmation of faith in the power of human ingenuity, and a bet on the future itself. And should one find themselves richly rewarded, as seems likely, they may reflect upon the wisdom of those who saw beyond the immediate horizon.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Celebs Who Narrowly Escaped The 9/11 Attacks

- How to Unlock Stellar Blade’s Secret Dev Room & Ocean String Outfit

- Global REIT ETFs: A Tale of Two Funds

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Persona 5: The Phantom X Relativity’s Labyrinth – All coin locations and puzzle solutions

- Honor of Kings: Must-Know Jungling Routes in 2025

- 20 Films Where Black Directors Subverted Hollywood’s White Savior Tropes

2026-03-14 02:32