So, the Middle East is doing its thing again, which, let’s be honest, is pretty much on brand for the last century. The Trump administration already injected a delightful amount of chaos into everything with tariffs and yelling at the Federal Reserve, but now we’ve got actual strikes on Iran. And everyone’s asking, “What does this mean for my 401k?” Which, honestly, is the most American question ever. Let’s unpack this, because history, like a really bad rom-com, tends to rhyme.

War & Stocks: A Complicated Relationship (Like Everything Else)

There’s been research done, a whole field of people staring at stock charts during wartime, and the results are… inconclusive. The CORP-DEPO folks have charts, graphs, the whole nine yards. But trying to predict market behavior based on conflict is like trying to predict what your boss is going to ask for on the way out the door – it’s a crapshoot. World War II is often cited as a boom time, but that was then. Now, we’ve got algorithms and high-frequency trading, which means the market reacts to things before anyone fully understands what’s happening. It’s like a really caffeinated squirrel.

The Russian invasion of Ukraine didn’t exactly tank global stocks, either. The STOXX Europe 600, bless its little index heart, is actually up since then. Which just proves that markets are weird, and sometimes logic takes a vacation.

I suspect we’ll see a similar pattern with Iran. The market, right now, is obsessed with AI and consumer spending. That’s where the money is, not geopolitical drama. Frankly, I’m more worried about the next earnings call than the Strait of Hormuz.

But Could Things Change? (Because They Always Do)

Look, right now, this doesn’t feel like a huge risk to the market. But let’s not pretend a full-blown ground operation wouldn’t be… problematic. Brown University crunched the numbers and found the “war on terror” cost us a cool $8 trillion. That’s a lot of avocado toast.

If this escalates, and U.S. debt keeps climbing, investors might start getting nervous about the dollar. That could send Treasury yields soaring, which would make everything more expensive for everyone, especially growth stocks that are already living on fumes. It’s like trying to run a marathon on a diet of optimism and venture capital.

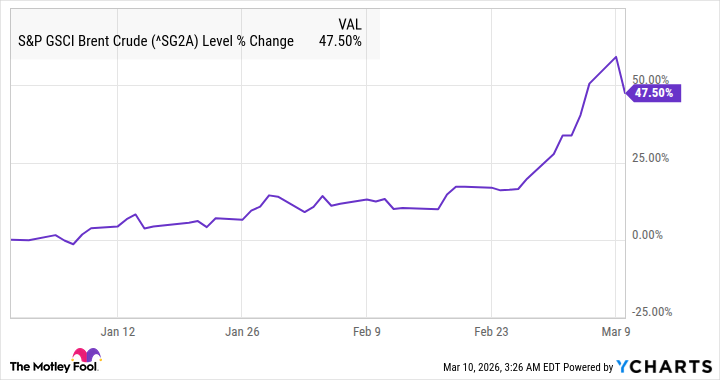

What About the Oil? (Now We’re Talking)

Okay, this is where things get interesting. Iran is a significant oil producer – number nine in the world, pumping out about 4% of the global supply. Any disruption there, and prices go up. And, yeah, they’ve already closed the Strait of Hormuz, which is basically the oil industry’s choke point.

Brent Crude is up about 48% since 2026, which, let’s be honest, is just rude.

But here’s the thing: the U.S. is the world’s biggest oil producer, by a long shot. That cushions the blow. Plus, everyone’s suddenly very interested in Guyana and Venezuela. And the White House, ever the pragmatist, is incentivized to get more oil flowing. So, a wait-and-see approach seems reasonable. It’s like watching a really slow-motion train wreck and hoping for the best.

Ultimately, the market will do what the market does: overreact, underreact, and generally make no sense. But hey, that’s what makes it fun. Or terrifying. It depends on your perspective, and your portfolio.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- The Best Directors of 2025

2026-03-13 19:52