![]()

The current enthusiasm for Micron Technology (MU 3.19%)—a surge of 239% in the last year, a further 33% already accrued in this unfolding annum—presents a spectacle both gratifying and, to the discerning eye, faintly absurd. It’s as if the market, usually a creature of sluggish deliberation, has briefly mistaken memory chips for some sort of digital elixir of life. One wonders, naturally, how long this particular fever will hold. Let us, then, dissect the currents buoying Micron, and assess whether this momentum is merely a shimmering mirage, or a genuine upwelling from the tectonic plates of technological demand.

The insatiable appetite of giants—Microsoft, Amazon, Alphabet, Meta Platforms—for GPU clusters is, of course, the primary catalyst. They are, these behemoths, constructing digital cathedrals, and every cathedral requires not just stained glass, but a prodigious quantity of silicon. The projected $600 billion in AI capital expenditure this year is a sum so vast it threatens to warp the very fabric of economic reality. Micron, quite cleverly, finds itself positioned as a crucial purveyor of the high-bandwidth memory (HBM) essential to these glittering, power-hungry altars of artificial intelligence.

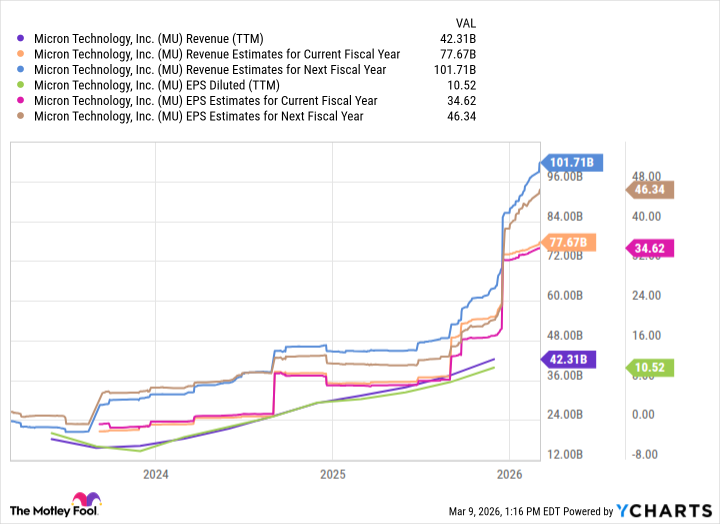

Historically, the memory market has been a capricious mistress, prone to dramatic swings dictated by the whims of consumer electronics upgrades. But AI, it appears, is attempting to impose a semblance of order, a new, insistent rhythm. Micron’s management confidently predicts a 40% annual growth rate for the HBM market through 2028, culminating in a rather baroque figure of $100 billion. A bold claim, certainly, and one that invites a raised eyebrow. Yet, consider this: Micron is, by its own account, already sold out of its HBM products. A delightful predicament for a manufacturer, wouldn’t you agree? The resultant surge in DRAM and NAND chip prices—60% and 38% respectively in the first few months of the year—is not merely impressive; it is, dare I say, a testament to Micron’s shrewd positioning and the burgeoning demand for its wares.

This is no longer a commodity market, my dear reader, but a landscape of specialized components, each integral to the larger AI ecosystem. Samsung and SK Hynix, naturally, loom as competitors, but Micron, with its current momentum, appears remarkably well-equipped to capitalize on this expanding market, enjoying both robust sales and, crucially, healthy profit margins. The subtle dance of supply and demand, orchestrated with a touch of silicon artistry.

How high can Micron climb? That, of course, is the perennial question. With AI adoption showing no signs of abating, and competitive pressures remaining relatively subdued, this “memory supercycle” – a rather ungainly term, but one that captures the essence of the situation – could well extend throughout the decade, perhaps even venturing into the 2030s. A tantalizing prospect, wouldn’t you agree? However, let us not succumb to excessive optimism. Capital expenditure budgets and infrastructure buildouts are, by their very nature, fluid and unpredictable. To attempt to forecast Micron’s precise trajectory with any degree of accuracy would be an exercise in amiable delusion.

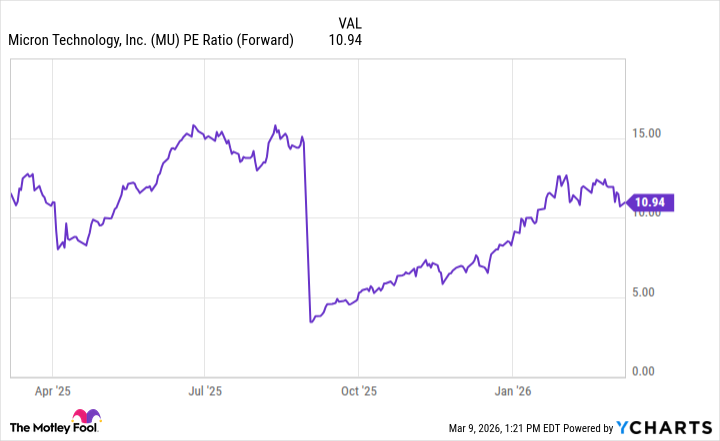

Nevertheless, a cursory glance at the company’s valuation profile offers a few clues. As of this writing (March 9), Micron boasts a forward price-to-earnings (P/E) ratio of 11—roughly half that of the Nasdaq-100. A rather striking discrepancy, wouldn’t you say? It suggests, perhaps, that the market has yet to fully appreciate Micron’s potential.

Even if Micron’s growth were to plateau, or show signs of maturing—a perfectly natural phenomenon, after all—I believe a significant upside remains. Over the next five years, a doubling of the current share price seems entirely feasible. And, under the most bullish of scenarios, Micron could conceivably reach $1,000 (or even more), joining the exclusive trillion-dollar club, provided it can secure a premium valuation and align itself with the broader tech sector. A rather ambitious projection, perhaps, but not entirely implausible. One might even say…memorable.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- The Best Directors of 2025

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- 20 Best TV Shows Featuring All-White Casts You Should See

- Umamusume: Gold Ship build guide

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Uncovering Hidden Signals in Finance with AI

- Gold Rate Forecast

- 39th Developer Notes: 2.5th Anniversary Update

- TV Shows That Race-Bent Villains and Confused Everyone

2026-03-13 14:42