The S&P 500, that curiously self-aware collection of publicly traded hopes and dreams, recently dipped a toe (or perhaps a substantial portion of its foot) into a bit of a wobble, closing Wednesday at 6,775.8 – a roughly 3.2% retreat from its peak in late January. Now, declines happen. They’re practically a defining characteristic of the entire endeavor. The question, of course, is whether this particular dip is merely a temporary gravitational adjustment, or the first shudder of something…more interesting. (Interesting, in the financial sense, rarely equates to ‘pleasant’. It’s a statistical anomaly, really.)

The current situation revolves, predictably, around oil. Specifically, the rather inconvenient fact that a significant portion of it – roughly 20%, give or take a tanker load – is currently refusing to flow through the Strait of Hormuz. This isn’t a matter of the oil being deliberately obstinate, of course. It’s merely that geopolitical events have, shall we say, discouraged its passage. Rapidan Energy, a firm whose job it is to worry about this sort of thing, has rather dramatically declared this the “biggest oil supply disruption in history.” One imagines their coffee breaks are… lively.

Brent crude, that globally-recognized benchmark of… well, crude, briefly flirted with $120 a barrel on Monday, a price not seen since the unpleasantness involving Russia and Ukraine in 2022. It’s since retreated somewhat, settling around $100, but remains stubbornly elevated – over 38% higher than before the aforementioned unpleasantness. (One begins to suspect that ‘unpleasantness’ is becoming a recurring theme in the modern economic narrative.) This, naturally, has implications. The market, being a remarkably sensitive organism, tends to react to such things.

What the Past Tells Us (and Why It Might Be Lying)

Looking back at previous oil-induced palpitations – the Gulf War in 1990, the 2008 financial crisis, and the 2022 Ukraine situation – reveals a pattern. A sort of financial dance, if you will: a sell-off, a period of anxious shuffling, and then, eventually, a recovery once the oil flow resumes and everyone remembers what they were worrying about in the first place.

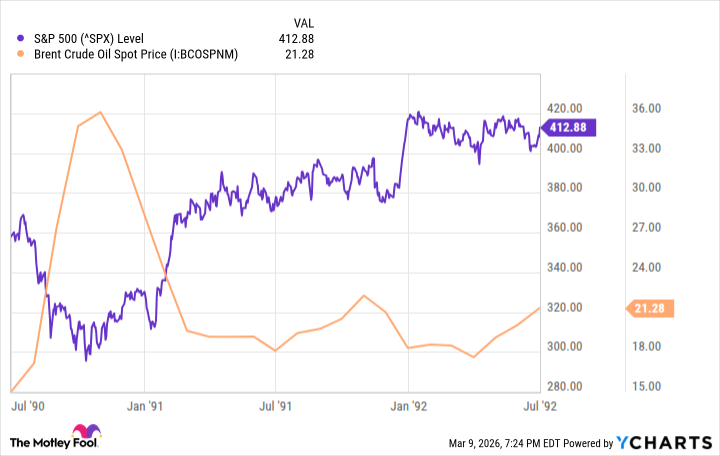

The 1990 Gulf War provides the cleanest example. Oil spiked, the S&P 500 dipped about 16% over three months, and then, rather efficiently, rebounded once the conflict resolved and Saudi Arabia decided to be helpful. It was, in a way, reassuringly predictable.

The 2022 situation, predictably, was more complicated. Russia’s actions, combined with existing supply chain issues, sent inflation soaring. The Federal Reserve responded with interest rate hikes at a pace that would make a cheetah blush. The S&P 500 dropped roughly 25% before bottoming out, but those who held on were eventually rewarded. (Though ‘rewarded’ is a relative term, of course. One might argue that simply avoiding total financial ruin constitutes a reward in the current climate.)

The 2008 crash is something of an outlier. Oil at $147 a barrel was part of the story, but the housing collapse and banking meltdown were the primary culprits. It was a bit like blaming the rain for a flood caused by a burst dam. (A perfectly valid analogy, if one is determined to be unhelpful.)

Why This Time Might Be Different (or Just Equally Confusing)

There are a few mitigating factors. The disruption could be short-lived if the Strait reopens or the U.S. releases strategic reserves. And, arguably, the U.S. is better positioned to handle a shock than it was in 1990 or 2022, thanks to increased domestic production and reduced reliance on foreign oil. (One should, however, remain cautiously optimistic. The universe has a peculiar fondness for proving optimists wrong.)

Still, volatility around a critical oil chokepoint is likely to persist, regardless of any de-escalation. Traders will remain on edge, anticipating further disruptions. (It’s a bit like expecting a rogue asteroid to appear at any moment. Statistically improbable, but not entirely outside the realm of possibility.)

Lessons from History (and Why We Never Learn)

This situation feels more akin to 1990 or 2022 than 2008. History suggests a relatively short-lived market correction. However, the economy is more fragile now than it was in 1990, and inflation remains a concern. The softening labor market further complicates matters, limiting the Federal Reserve’s options. (It’s a bit like trying to navigate a labyrinth blindfolded while juggling flaming torches. Technically possible, but not advisable.)

And then there’s the looming question of artificial intelligence. Is the current capital expenditure cycle sustainable growth, or a bubble waiting to burst? Companies are taking on enormous debt to fund this build-out, and that debt won’t respond well to sudden rate hikes. (Echoes of 2008, perhaps? One should at least acknowledge the possibility.)

A repeat of 2008 seems unlikely, but panic selling during previous oil shocks proved costly. For long-term investors, the most important thing isn’t predicting oil prices; it’s examining your portfolio. Are you invested in companies you believe in? (A surprisingly difficult question to answer, given the inherent absurdity of the entire endeavor.)

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- The Best Directors of 2025

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- 20 Best TV Shows Featuring All-White Casts You Should See

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Umamusume: Gold Ship build guide

- Top 20 Educational Video Games

- Celebs Who Married for Green Cards and Divorced Fast

- Most Famous Richards in the World

2026-03-12 19:44