For six decades, the name Warren Buffett was, shall we say, sutured to Berkshire Hathaway. A paternal figure presiding over a kingdom of capital. Now, with the baton passed to Greg Abel, a curious thing has occurred. A slight tremor in the carefully constructed equilibrium. Abel, a creature of operational finesse rather than the Buffettian alchemy of investment whims, has dared to… repurchase shares. A gesture both predictable and, in its very predictability, subtly audacious. It’s as if a meticulous watchmaker, inheriting a grandfather clock, decided to polish the pendulum. A necessary act, perhaps, but one that acknowledges a change in tempo.

The final years of the Buffett reign saw a curious shedding of equity, a strategic divestiture that swelled the cash reserves to proportions bordering on the baroque. Share buybacks, a quarterly ritual for twenty-four consecutive seasons, ceased abruptly in June of 2024. Twenty-one months of abstinence. A prolonged pause that invited speculation, a silence that now, with Abel’s intervention, has been elegantly broken. One suspects a certain impatience, a quiet assertion of autonomy. Or perhaps, simply, a favorable valuation. The market, after all, is a capricious mistress, and even the most discerning eye can occasionally detect a fleeting moment of lucidity.

Abel, it appears, perceives such a moment. The resumption of buybacks isn’t merely a financial transaction; it’s a declaration. A signal sent flickering across the ticker tape: Berkshire Hathaway, while evolving, remains a creature of value. And, intriguingly, Abel has dipped into his own coffers, investing a not insignificant $15 million. A gesture that transcends mere corporate procedure. It’s a personal endorsement, a wager placed on the future. A rather delightful detail, wouldn’t you agree?

A Fleeting Opportunity, Observed

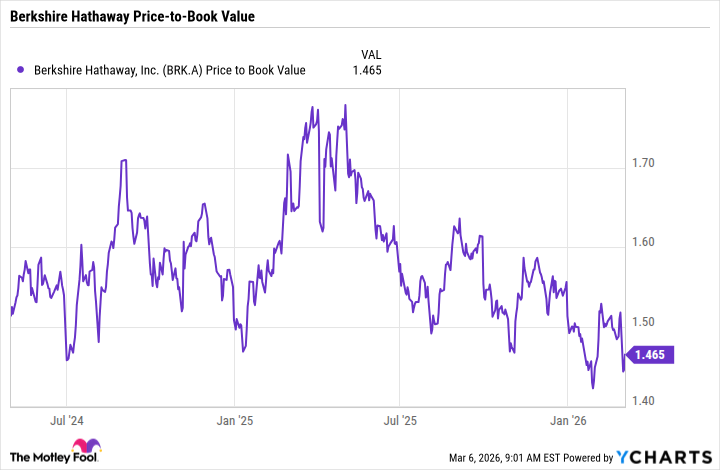

The announcement of Buffett’s impending departure cast a shadow, a momentary dip in Berkshire’s valuation. A predictable reaction, of course. The market dislikes uncertainty, even when that uncertainty is merely the changing of a guard. The price-to-book ratio, that most reliable of metrics, descended to a rather fetching 1.5. A level rarely seen since the last buyback spree. Yet, Buffett remained unmoved. A curious reticence. One wonders if he was waiting for a more… dramatic capitulation. Or perhaps, simply enjoying the spectacle.

The new year brought a further decline, pushing the ratio down to 1.42. A tempting figure. But valuations, like butterflies, are fleeting. The data, compiled in the 2025 annual report, may have lacked the immediacy required for decisive action. The present, as always, is a slippery thing.

The full-year results revealed a cash pile of $373 billion, a sum that borders on the fantastical. The equity portfolio, valued at just under $300 billion, adds further weight to the equation. A formidable combination. Abel, with a pragmatism that is distinctly his own, seized the opportunity. The buybacks commenced on March 4th, coinciding with a minor dip in share price, triggered by disappointing quarterly results and the distant rumble of geopolitical unrest. A coincidence, perhaps? Or a shrewd calculation? The market, after all, is often driven by irrationality. A well-timed purchase, however, can be exquisitely rewarding.

On March 4th, Berkshire traded at a price-to-book ratio of 1.46. A seemingly modest figure. But valuations are rarely straightforward. Adjustments for the real-time value of the portfolio and the ever-increasing cash pile reveal a more compelling picture. The current valuation, therefore, presents a rather seductive opportunity. A chance to acquire a piece of a remarkably well-managed enterprise at a price that is, shall we say, agreeable.

Is the Allure Genuine?

A favorable valuation, however, does not automatically guarantee a sound investment. Berkshire’s book value, while substantial, is largely composed of liquid assets. A deeper analysis of the company’s operating results is therefore essential. Is Berkshire deserving of a higher multiple than in the recent past? The answer, as always, is nuanced.

The insurance business, typically a bastion of stability, experienced a curious interplay of fortune and misfortune. The California wildfires, a perennial threat, were offset by a remarkably quiet hurricane season. A stroke of luck, perhaps? Or a testament to Berkshire’s superior risk management? GEICO, the insurance subsidiary, continued to climb, while losses remained consistent with the previous year. A steady performance, if not a spectacular one.

Burlington Northern Santa Fe (BNSF), the railroad behemoth, showed improvements in operating margin, thanks to a reduction in idle time. Yet, it still lags behind its primary competitor, Union Pacific, which boasts a significantly higher margin. A minor imperfection in an otherwise impressive portfolio. A reminder that even the most well-managed enterprises are not immune to the vagaries of competition.

The energy business delivered results in line with expectations. However, recent legislative changes pose a potential threat. The “big, beautiful bill,” as it is known, may negatively impact future earnings. A cautionary note. A reminder that the regulatory landscape is ever-shifting.

The manufacturing, service, and retailing segment saw a slight increase in revenue and improved operating margin. A modest gain. A subtle indication of underlying strength.

The results, therefore, are mixed. But investors should consider the potential for future improvement. Berkshire’s insurance business benefits from its unparalleled ability to underwrite risk. The railroad business is showing signs of recovery. The energy business, despite regulatory challenges, remains a valuable asset. As a result, now may be an opportune moment to acquire shares.

Abel, it seems, shares this view. He not only deployed Berkshire’s cash but also invested $15 million of his own funds. A bold move. A clear signal of confidence. Berkshire Hathaway, while evolving, remains a company of exceptional quality. And it is currently trading at a fair price. A rather delightful confluence of circumstances, wouldn’t you agree?

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- The Best Directors of 2025

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- 20 Best TV Shows Featuring All-White Casts You Should See

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- Umamusume: Gold Ship build guide

- Top 20 Educational Video Games

- Most Famous Richards in the World

- Celebs Who Married for Green Cards and Divorced Fast

2026-03-12 05:03