The American market, as any astute observer knows, is a stage crowded with pretenders to lasting value. Currently, ten companies bask, however briefly, in the golden light of a trillion-dollar valuation. Among them, Nvidia, Apple, Alphabet, Microsoft, Amazon, Meta, Broadcom, Berkshire Hathaway, and Walmart. And, of course, Tesla. It is a curious club, and one suspects that membership, like reputation, is often more fragile than it appears.

Tesla, you see, is priced as if it possesses not merely a future, but a monopoly on it. A rather bold claim, even for a company whose CEO traffics in the spectacular. The market, it seems, has a fondness for narratives, and Tesla’s—of robotaxis and humanoid robots—is particularly captivating. One might say it is a triumph of imagination over, shall we say, current performance.

The truth, as is so often the case, is considerably less romantic. Despite the grand visions, a rather pedestrian reality persists: 73% of Tesla’s revenue still derives from selling automobiles—automobiles whose demand, I observe with a certain detached amusement, is demonstrably waning. To build a kingdom on the shifting sands of consumer preference is, at best, a risky undertaking.

I predict, with a confidence born not of certainty, but of observation, that Tesla will relinquish its trillion-dollar status before the close of 2026. It is not a matter of if, but when the market finally demands a reckoning.

The Inexorable Decline of the Electric Dream

In 2024, Tesla delivered a respectable, if unremarkable, 1.79 million electric vehicles. A mere 1% decline, one might argue. But 2025 brought a sharper awakening: 1.63 million deliveries—a 9% contraction. This, in turn, dragged automotive revenue down by 10%, culminating in a rather alarming 47% plunge in earnings per share. Earnings, naturally, are the currency of reality, and reality, as I’ve found, has a habit of intruding upon even the most elaborate fantasies.

The impending withdrawal of the Model X and Model S—premium vehicles, admittedly—is presented as a strategic realignment. A focusing of efforts on the more accessible Model Y and Model 3. A sensible move, perhaps, but one that will pit Tesla directly against the increasingly formidable—and significantly cheaper—Chinese manufacturers, most notably BYD. BYD, it should be noted, offers an electric vehicle for under $27,000 in Europe, while Tesla’s Model 3 begins at over $40,000. A rather substantial difference, wouldn’t you agree? The market, after all, is rarely swayed by poetry.

BYD, in fact, outsold Tesla globally in 2025 for the first time. A statistic that speaks volumes, and not necessarily in Tesla’s favour.

The Future is Always Further Away Than It Seems

Mr. Musk, a man not unfamiliar with hyperbole, is understandably reluctant to engage in a price war. His solution? To pivot towards autonomous vehicles and robotics. The Cybercab, a robotaxi promising a revolution in urban transportation, and Optimus, a humanoid robot poised to conquer the factory floor. Lofty ambitions, to be sure. But ambition, without execution, is merely a pleasant distraction.

The Cybercab, alas, remains tethered to the limitations of regulation and technology. Full self-driving approval is currently restricted to Austin, Texas. A charmingly provincial state of affairs. Mass production is anticipated, but contingent upon regulatory approval. A rather crucial detail, wouldn’t you say?

The market for humanoid robots is, as yet, unproven. Mr. Musk confidently predicts that robots will outnumber humans by 2040. A bold claim, though one suspects it is more aspirational than analytical. Optimus is slated for production in Fremont, California, utilizing spare capacity. A convenient solution, though one wonders if the factory will be filled with robots building robots, a rather unsettling thought.

The Illusion of Value

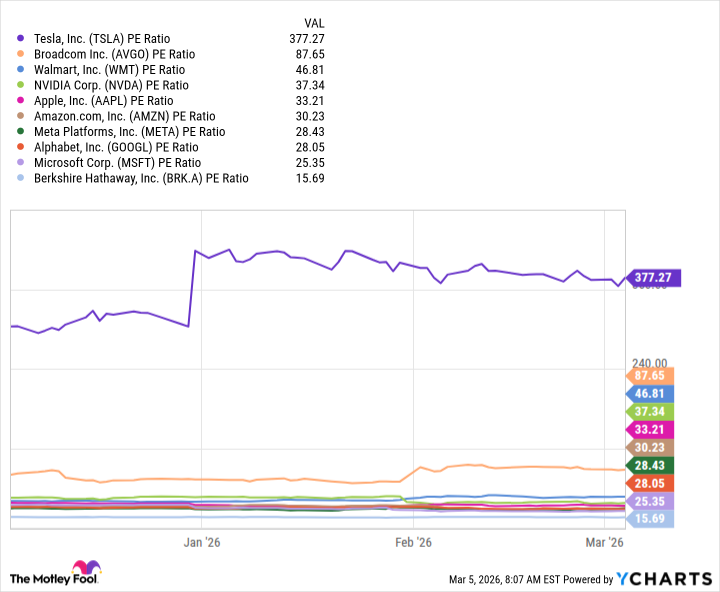

In 2025, Tesla’s earnings plummeted by 47% to $1.08 per share. A rather substantial decline. One might expect the stock to reflect this reality. It has not. Tesla currently trades at a price-to-earnings ratio of 377. An extraordinary figure. It is, quite simply, more than eleven times as expensive as the Nasdaq-100 index. To be so richly valued, despite such a precipitous decline in earnings, is…untenable.

A 77% decline would be required to bring Tesla in line with Broadcom, the next most expensive stock in this dubious club. I do not suggest that such a dramatic fall is inevitable. However, a mere 34% decline would suffice to eject Tesla from the trillion-dollar echelon. If electric vehicle sales continue to falter, or if investors perceive delays in the Cybercab and Optimus rollouts, such a decline is entirely plausible in 2026. And, as any discerning investor knows, the higher one climbs, the further one has to fall. It is, alas, the immutable law of gravity.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- Securing the Agent Ecosystem: Detecting Malicious Workflow Patterns

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Mel Gibson, 69, and Rosalind Ross, 35, Call It Quits After Nearly a Decade: “It’s Sad To End This Chapter in our Lives”

- TV Shows Where Asian Representation Felt Like Stereotype Checklists

- The Best Directors of 2025

- Games That Faced Bans in Countries Over Political Themes

- 📢 New Prestige Skin – Hedonist Liberta

- Most Famous Richards in the World

2026-03-10 11:43