It is a truth universally acknowledged, that a company in possession of a novel technology, must be in want of a sustainable profit. SoundHound AI, a purveyor of voice-activated assistance, has of late attracted a degree of notice, and not entirely to its advantage. The business, it is claimed, aids its clients in the efficient conduct of their daily affairs, and has expanded its reach through a series of acquisitions—a practice not uncommon amongst those seeking to present a more robust countenance.

One might be surprised, however, to learn that despite a doubling of its revenues in the past year, this particular stock has suffered a decline in esteem. Its current market capitalization, at approximately $3.4 billion, is but a shadow of its former self, and the share price has fallen considerably from its recent peak. It is a circumstance that invites a degree of scrutiny, and suggests that optimism, while plentiful, is not universally shared.

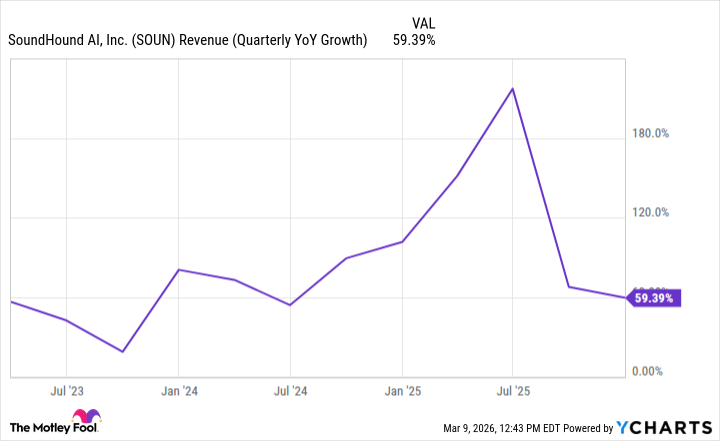

A Diminishing Rate of Advancement

Recent reports from SoundHound indicate a growth in revenue of 59% for the last quarter, amounting to just over $55 million. The full year’s revenue reached $168.9 million, a considerable increase from the previous year’s $84.7 million. A respectable showing, one might concede, yet a discerning observer cannot help but note a slowing of momentum. It is a pattern that raises questions as to the true source of this apparent prosperity.

The figures, when examined with a critical eye, reveal a temporary surge followed by a marked deceleration. While a growth rate of nearly 60% is not to be dismissed lightly, it is essential to understand the circumstances that have contributed to it. The expansion, it appears, has been largely achieved through acquisitions, a method which, while capable of inflating the top line, does not necessarily reflect underlying organic strength. Such a strategy, while providing a temporary lift, is often insufficient to ensure lasting prosperity.

The Perils of Unsustainable Growth

Impressive figures, however, cannot entirely conceal certain fundamental weaknesses. Last year, the company registered an operating loss of $23.3 million—a deficit mitigated only by a favorable adjustment in the fair value of contingent acquisition liabilities. Furthermore, the business consumed $98.2 million in operating activities. Such a state of affairs is, to say the least, precarious.

The lack of consistent profitability, the ongoing cash burn, and the reliance on acquisitions all contribute to a degree of risk that should not be underestimated. Investors may well find themselves subject to dilution in the future, as the company seeks to replenish its coffers. Indeed, the stock has already experienced a decline of 20% this year, and a further reduction in value would not be entirely unexpected. For while the rate of growth may appear promising, it is a narrative that does not, upon closer inspection, tell the whole story.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- Gold Rate Forecast

- Securing the Agent Ecosystem: Detecting Malicious Workflow Patterns

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- The Best Directors of 2025

- TV Shows Where Asian Representation Felt Like Stereotype Checklists

- Games That Faced Bans in Countries Over Political Themes

- 📢 New Prestige Skin – Hedonist Liberta

- Most Famous Richards in the World

- SEGA Sonic and IDW Artist Gigi Dutreix Celebrates Charlie Kirk’s Death

2026-03-09 23:02