The market, a creature of whims and anxieties, has turned its gaze upon Oracle (ORCL 2.33%). The share price, once a stout fellow, now appears… diminished, having lost a considerable portion of its heft since the commencement of the year. A question hangs in the air, thick as the dust motes dancing in a forgotten archive: is this a moment for hasty retreat, a frantic scramble to salvage what remains? Or might it be, perchance, an opportunity? A foolish notion, perhaps, but one that demands examination, lest we succumb to the paralysis of indecision.

Let us delve, then, into the labyrinthine affairs of this technological behemoth, guided by the faint glimmer of reason and a healthy dose of skepticism. Two observers, burdened with the task of deciphering Oracle’s current predicament, offer their insights – though whether these insights will illuminate or merely add to the confusion remains to be seen.

The Weight of Promises and the Murmur of Bonds

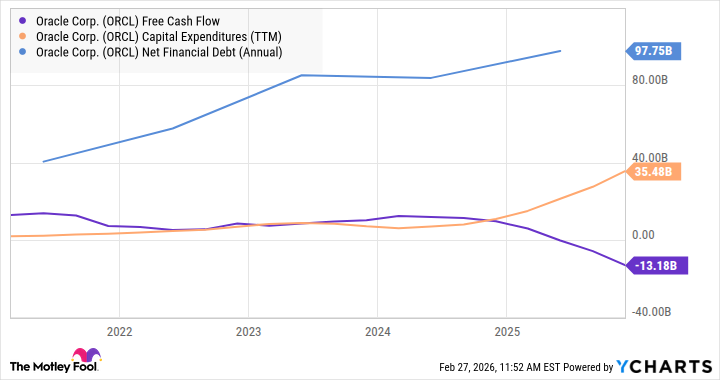

Lee Samaha, a man who appears to possess an unsettling familiarity with balance sheets, observes that Oracle’s stock has suffered a decline exceeding fifty percent since the announcement of its rather ambitious entanglement with OpenAI. A sum of three hundred billion, you understand! A figure so vast it threatens to swallow entire provinces. Equity investors, those nervous creatures, are growing increasingly concerned. Not merely about the cost of constructing these digital fortresses – these data centers, as they are politely called – but about the very possibility of OpenAI securing the funds necessary to fulfill its end of the bargain. A precarious arrangement, built upon a foundation of hope and, one suspects, a considerable amount of wishful thinking.

And the capital expenditure, ah, the capital expenditure! It swells, like a neglected wound, consuming cash at an alarming rate. A company already burdened with debt, now reaching deeper into its pockets. One might imagine a portly gentleman attempting to squeeze into a coat two sizes too small. It is not a pretty sight.

But the matter does not end there. The credit default swap spreads, those cryptic indicators of financial health, have begun to twitch and writhe. From a placid forty basis points to a decidedly agitated 125 to 145! Investors, those pragmatic souls, are purchasing protection against the possibility of default. A rather unseemly display of pessimism, wouldn’t you agree? Though, one must concede, it is a pessimism not entirely unwarranted. Should Oracle require further funding, the market will undoubtedly demand a higher price. A higher price for risk, of course. And that, my friends, is a burden that will fall squarely upon the shoulders of the shareholders.

The situation, you see, is a delicate dance. A decline in the share price makes it more difficult to raise capital through equity offerings. This, in turn, raises concerns among bondholders, who begin to question the company’s ability to repay its debts. A vicious cycle, indeed. Oracle, therefore, finds itself in the unenviable position of needing to convince the market that it and OpenAI can, in fact, fund their operations in accordance with their grand designs. A task that, one suspects, will require a miracle, or at least a very persuasive accountant.

The Fickle Nature of Investment and the Illusion of Returns

Scott Levine, a man who seems to view capital expenditure with a particular brand of suspicion, notes the growing skepticism surrounding the massive investments being made in artificial intelligence. A skepticism, he argues, that is entirely justified. Oracle, in its eagerness to embrace this technological marvel, has embarked upon a spending spree that is, to put it mildly, rather extravagant. Through the first six months of fiscal 2026, the company has expended a staggering sixteen point four billion dollars on capital expenditures! A figure that dwarfs the six point six billion reported for the same period last year. And there is no indication that this spending will abate anytime soon. Oracle anticipates requiring approximately fifty billion dollars in 2026 to support the construction of its data center infrastructure. A sum that could, one imagines, fund a small nation.

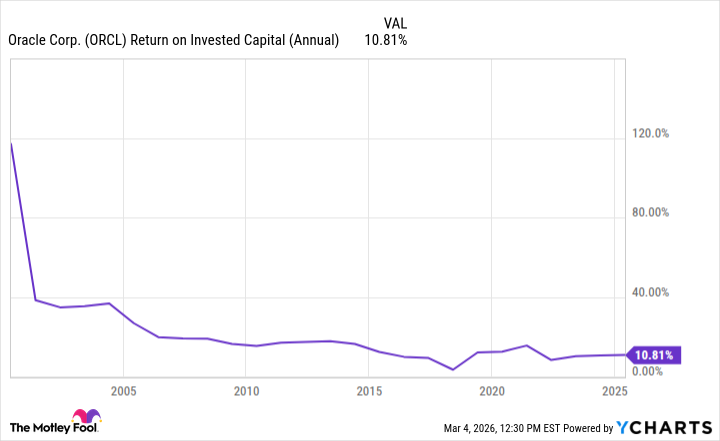

While the demand for AI infrastructure may indeed be growing, investors are understandably hesitant to embrace Oracle’s substantial investments, given the company’s history of declining returns on invested capital. Over the past twenty-five years, the company has consistently failed to generate adequate returns. A rather damning indictment, wouldn’t you agree? Ken Bond, Oracle’s senior vice president for investor relations, attempts to reassure shareholders, stating that the vast majority of these capital expenditures are for revenue-generating equipment. A comforting thought, perhaps, but one that requires careful scrutiny. If Oracle fails to generate stronger profits following the completion of its data center infrastructure, the company’s financial health will undoubtedly be compromised.

A Cloud of Uncertainty and the Prudence of Observation

So, what should Oracle investors do? The company remains a leader in the cloud computing space, and there is certainly a compelling argument to be made for holding onto Oracle stock. However, savvy investors know that owning shares of any company demands constant vigilance. It is not time to abandon ship, but it is certainly time to pay particularly close attention to the company’s upcoming financial reports. Observe, analyze, and, above all, remain skeptical. For in the world of finance, as in life, appearances can be deceiving, and the most promising ventures often harbor hidden dangers. And a little bit of caution, you’ll find, goes a long way.

Read More

- Building 3D Worlds from Words: Is Reinforcement Learning the Key?

- Gold Rate Forecast

- Securing the Agent Ecosystem: Detecting Malicious Workflow Patterns

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Wuthering Waves – Galbrena build and materials guide

- The Best Directors of 2025

- TV Shows Where Asian Representation Felt Like Stereotype Checklists

- Games That Faced Bans in Countries Over Political Themes

- 📢 New Prestige Skin – Hedonist Liberta

- SEGA Sonic and IDW Artist Gigi Dutreix Celebrates Charlie Kirk’s Death

2026-03-09 19:23